Quick Answer

Treat essentialism for solopreneurs as a compliance-first operating method: focus on the few decisions that can damage your business, then standardize how you handle them. Keep residency tracking current, validate invoice requirements before submission, and monitor foreign-account reporting exposure like FBAR on a set cadence. The goal is not doing fewer tasks for its own sake, but reducing uncertainty so cash flow, records, and decisions stay reliable.

The Essentialist OS: A Risk-Mitigation Framework for Your Business-of-One#

If you run a business-of-one, the useful version of essentialism is not mainly about getting more done. It is about lowering the odds that one preventable mistake in tax residency, invoicing, or reporting turns into a costly mess. The Essentialist OS is a practical lens: identify the few risks that can actually hurt the business, standardize how you respond to them, and review those controls on a regular schedule.

That shift matters because many solo operators are not mainly struggling with too many apps or meetings. They are exposed where the work touches money, records, and accountability. A missed reporting obligation, an invoice that does not meet the relevant rules, or unclear tax residency data can create friction with payments, advisors, and potentially regulators. That friction often shows up long before it appears in your calendar.

What the Essentialist OS means in practice#

Start with a narrower definition of essential. For a solo business, essential work is the work that keeps the business valid, paid, and defensible. In practice, that usually comes down to three things: knowing where your tax position could change, making sure invoices can stand up to scrutiny, and keeping reporting duties visible instead of treating them as background admin.

One checkpoint matters more than it sounds. Track your physical presence against statutory tax residency rules. Not roughly. Not from memory. If your business depends on cross-border work or travel, your location data stops being a personal detail and becomes compliance input.

The same logic applies to invoicing. If a client, platform, or jurisdiction requires particular fields or treatment, mark those requirements clearly and verify them before you send anything.

Standardizing your response does not require a heavy process. It means deciding in advance what happens when a recurring risk appears. If travel patterns change, review residency exposure. If a new client is in a different jurisdiction, verify what the invoice must include before you send it. If a reporting area like FBAR could apply, do not rely on vague reminders. Keep it on a reviewed list with ownership attached.

Why generic advice breaks for solo operators#

The first problem is severity mismatch. General productivity advice treats distractions and task volume as the main issue. Your real exposure may be higher stakes altogether. Even older FBAR penalty examples are severe enough to make the point. They include over $16,000 per violation for some non-willful failures, and the greater of $165,353 or 50% of account balance for willful violations. Current amounts still require verification before use. That is not the same class of problem as an overfull inbox.

The second problem is scope. Generic advice may help you prioritize projects, but it rarely reaches finance and compliance. It may not tell you how to keep invoicing compliant, how to spot reporting obligations, or how to reduce drag from fragmented tools. For a solo business, those are not back-office details. They can affect cash collection, record quality, and whether you can defend what you did later.

The third problem is ownership. An accountant, bookkeeper, or assistant can support parts of the work, but final authority should stay with you for tax residency data, core client relationships, and business structure. If nobody owns the last review, errors sit in the gaps between people. In practice, that is a common failure mode for solo operators who do have help but never defined what cannot be delegated.

The execution path from here#

The next three sections put that lens to work.

- First, cut non-essential risk by focusing on the small set of compliance exposures that matter most, including residency, invoicing, and reporting visibility.

- Next, remove operational drag that quietly burns revenue, especially from high-friction clients and fragmented financial tools.

- Then, lock in execution with clear ownership, repeatable response rules, and regular reviews so control does not depend on memory.

If you keep one rule from this section, keep this one. When a task affects legal status, payment validity, or reporting exposure, treat it as a business control, not a productivity preference. That reframe is what makes this approach useful. For related reading, see The Best Personal Productivity Systems for Freelancers (GTD).

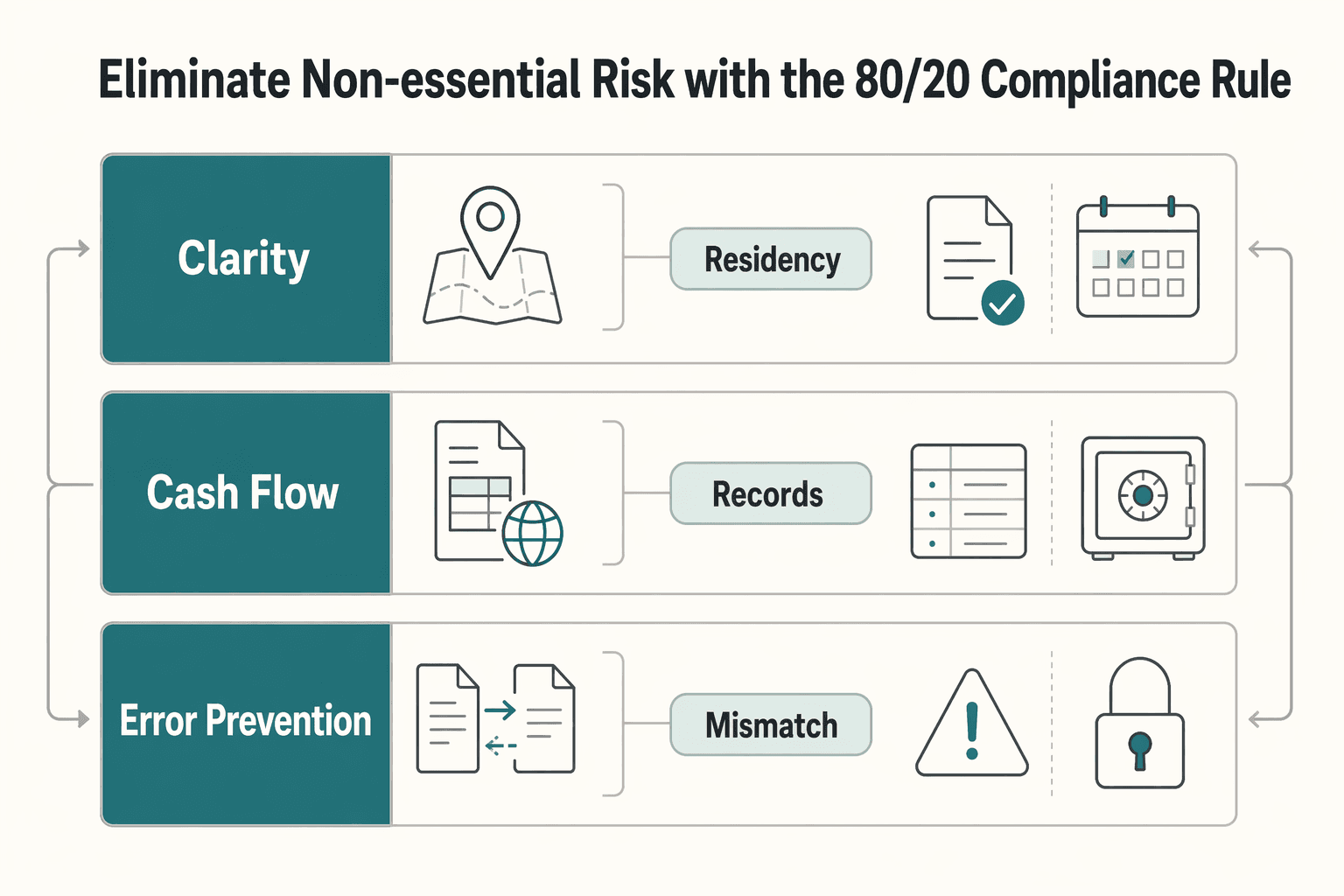

Step 1: Eliminate Non-Essential Risk with the 80/20 Compliance Rule#

Use this step to build a lightweight compliance control system around the few risks that can actually hurt your business: tax residency, cross-border invoicing, and FBAR exposure. You do not need to become a specialist. You need clear records, clear review points, and clear ownership.

| Focus | Ad hoc compliance behavior | Essentialist compliance workflow |

|---|---|---|

| Clarity | You rely on memory, old emails, and rough assumptions. | You keep one current log for dates, client billing requirements, and reporting watchpoints. |

| Cash-flow protection | You send invoices, then fix issues after a client or advisor flags them. | You verify required treatment before sending, so invoices are easier to approve and pay. |

| Error prevention | You review only when something feels off or a deadline is near. | You review on a set cadence and when travel, client location, or account balances change. |

Tax residency: track facts, not memory#

- Track: your physical presence by date and location.

- Log: one place you will maintain consistently, for example one spreadsheet or note.

- Review: monthly, and again when travel patterns change or before advisor conversations.

Final accountability for this data stays with you, even if someone else helps interpret it.

Cross-border invoicing: protect payment before send#

- Track: which clients fall outside your usual setup, plus client-provided billing details.

- Log: client record plus master invoice-template notes.

- Review: before invoicing a new jurisdiction, and whenever contract terms, client entity, or billing contact changes.

Treat invoicing as a control point, not background admin, so you do not discover issues only after a five-figure payment is delayed.

FBAR exposure: run a watchlist, not a year-end scramble#

- Track: aggregate balance across relevant foreign accounts, if foreign-account reporting could apply.

- Log: monthly snapshots in the same compliance sheet; current threshold pending source-record verification.

- Review: monthly, and any time balances jump due to payment, transfer, or account changes.

For FBAR (Report of Foreign Bank and Financial Accounts), this routine keeps reporting exposure visible instead of leaving it to a reactive scramble.

If you want a deeper dive, read GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

Step 2: Recapture Lost Revenue by Eliminating Operational Drag#

Once compliance basics are in place, the next revenue leak is operational friction you have normalized. The job here is to keep cash collection, records, and owner attention aligned so avoidable admin drag does not eat paid work.

Use a client friction scorecard before signing or renewing#

Because final authority over core client relationships stays with you, apply the same screen to every new engagement and renewal:

- Payment behavior: Will they follow your standard invoicing flow and pay inside your target payment window? (Target payment window pending source-record verification.)

- Process maturity: Can they onboard, approve, and pay without custom detours each cycle?

- Communication load: Do you have one accountable contact with decision authority?

- Scope-change reliability: When scope shifts, do they confirm changes in writing before delivery and honor the updated invoice?

Do not rely on headline fee alone. If friction keeps showing up, treat it as a terms, pricing, or renewal decision before work expands.

Before delivery starts, keep one client evidence file with legal entity name, billing contact, payment instructions, procurement requirements, and required invoice wording. This protects collection and helps prevent invoice mistakes that can put a five-figure payment at risk.

| Operating area | Fragmented operations | Integrated operations |

|---|---|---|

| Billing speed | Invoice details are pulled from emails, notes, and separate apps before each send. | Client, invoice, and payment details sit in one current record, so billing moves with fewer delays. |

| Error risk | Manual re-entry across tools increases mismatches and missing context. | Fewer handoffs reduce re-entry mistakes and record gaps. |

| Reconciliation effort | You reconcile status across multiple systems after the fact. | Invoice and payment status are traceable in one operating record. |

| Owner attention cost | You spend billable attention reconstructing what happened. | Less context switching keeps attention on delivery and growth. |

Consolidate tools and payment rails on purpose#

Aim for a single integrated financial system: one source of truth, fewer handoffs, and audit-friendly records you can explain later.

Use a short migration sequence:

- Map where client, invoice, payment, and accounting data are duplicated today.

- Choose one primary operating record for active clients and payment status.

- Migrate active clients first, keep old systems read-only for history, and verify opening balances/status before fully switching.

Run banking and payments with a simple policy: one preferred collection rail, one backup rail for true exceptions, a fee/FX review cadence verified from your finance records, and written exception terms when clients request nonstandard rails. Keep a current leakage note in the same finance record, including who absorbs fees, required remittance details, proof-of-payment records, and any leakage benchmark that still needs source-record verification.

You might also find this useful: A Guide to 'Deep Work' for Freelancers.

Step 3: Execute Flawlessly with an Essentialist Operating System#

Once client friction and tool sprawl are under control, the next risk is unclear ownership. Keep final authority over a few high-stakes decisions, use simple if-then protocols for recurring triggers, and run a review cadence you can sustain.

Keep decision rights clear#

You do not need to do everything yourself, but you should keep final authority where risk can materially change: your tax position data, core client relationships, and business structure.

| Decision area | You own (final approval) | Advisors/support can do | Delegate with approval gate |

|---|---|---|---|

| Tax position and residency facts | Confirm the facts and filing position before finalization | Prepare analysis, draft records, flag issues | Data collection and draft tracking, then return to you for sign-off |

| Core client relationships | Approve renewal, scope, pricing, or exit calls | Prepare options and implications | Admin follow-ups after your decision |

| Business structure | Approve any structure change | Model tradeoffs and implementation steps | Execution tasks only after your approval |

Use one rule: if a task can change business facts, filing position, or a core client outcome, it comes back to you before final action.

Use a repeatable if-then protocol#

Use one template for predictable events so decisions do not rely on memory.

- Trigger: event that starts review

- Required check: what must be validated first

- Owner: who prepares, who approves

- Documentation: what to save, where

- Fallback: what to do if unclear or failed

You can copy this format directly:

| Trigger | Required check | Owner | Documentation | Fallback |

|---|---|---|---|---|

| Travel or living-pattern change | Reconcile physical-presence records against current rules verified from official source records | Support prepares; you approve | Calendar export, travel records, tracker snapshot | Pause final action and escalate for review |

| New foreign bank/financial account or reporting-risk change | Confirm whether reporting obligations may apply under the current verified rule | Advisor prepares; you approve | Account inventory, statements, filing/analysis record | Hold submission or account-change workflow until resolved |

| Material client change (renewal/scope/pricing) | Confirm risk, payment process, and relationship impact | Team prepares; you approve | Decision note, updated terms, client file update | Keep current terms temporarily or defer commitment |

Reactive execution vs Essentialist OS#

| Dimension | Reactive execution | Essentialist system |

|---|---|---|

| Decision speed | Re-decisions happen under pressure | Owners and approval gates are predefined |

| Compliance consistency | Checks vary by memory and context | Same trigger runs the same check each time |

| Handoff clarity | Ownership is implied | Ownership and approval points are explicit |

| Error recovery | You reconstruct from scattered messages | You trace decisions through saved records |

Run a practical review ritual#

Pick a fixed cadence you can maintain, for example monthly or quarterly based on how quickly your facts change. Keep the same agenda each time:

- Compliance signals: residency tracking, invoicing exceptions, foreign-account/reporting changes, pending follow-ups.

- Decision-right drift: where someone else started making calls that should return to you.

- Operational friction: one recurring source of cleanup to remove next.

- Next-period changes: travel, key renewals, pricing decisions, structure questions.

End each review with clear outputs:

- Decisions made

- Risks flagged

- Next-period priorities

- Evidence updates required

- Owner and due date for each follow-up

This is how the Essentialist OS stays practical: your attention stays on the few decisions that protect the business, and your records stay clear enough to explain later. For a step-by-step walkthrough, see A Guide to Calendly for Freelance Scheduling.

Conclusion: The Ultimate Freedom is Freedom from Anxiety#

If you want the practical payoff of essentialism as a solopreneur, aim for less uncertainty, not just fewer tasks. Build a business-of-one you can actually trust: a compliant foundation, cleaner operations, and day-to-day decisions that do not depend on memory, guesswork, or crossed fingers.

That looks ordinary on purpose. You track your physical presence against the residency rules that apply to you. You keep final approval over your tax residency data, core client relationships, and business structure. You issue invoices that match the rules you have verified, cut high-friction clients that create admin drag, and consolidate tools where duplicate work keeps creating mistakes. Less ambiguity gives you better control. Less friction gives you better focus.

The risk is often not one dramatic failure. It can be assumption drift: an unverified residency period, a client exception that becomes the norm, or an account/reporting obligation you meant to check later. That is where anxiety builds. You know something important may be off, but you do not know exactly where. A resilient solo business reduces that feeling by keeping key facts current and the evidence behind them easy to find when needed.

So keep the method simple and repeatable. Use your quarterly review to check the few things that can materially change your position. That includes residency tracking, invoicing compliance, foreign account exposure such as FBAR relevance, client friction, and any rule that still needs verification. Then make the next small correction. Not a reinvention. Just consistent application of the same discipline until your business feels controlled because it is.

Frequently Asked Questions

How should you simplify your tech stack?

Start with a braindump of every app, login, and manual handoff in your business, then keep the tools that reduce duplicate entry and review friction. Some automation helps, but convenience alone is not a good reason to add another app if it creates one more place to reconcile information. Next step: map your sales, delivery, billing, and record-keeping tools on one page, then cut the ones that create repeated copy-paste or unclear ownership.

What compliance work deserves your attention first?

Start with the few obligations that could create the biggest cleanup if missed, but treat every rule as jurisdiction-dependent until you verify it. A useful filter is to ask what one check you can do now that would make other tasks easier or unnecessary, such as confirming which residency rule, invoice requirement, or reporting trigger applies to you. Next step: make a short register of obligations by country and add “current rule,” “deadline,” and “verified by” fields, marking any threshold or deadline as pending until it is verified from official source records.

What should you keep final approval over, even if you delegate?

You can delegate preparation, research, and routine follow-up, but keep final approval over the few decisions that materially change your priorities or obligations. A common failure mode is letting priorities drift to someone else by assumption. Next step: label recurring tasks as prepare, approve, or archive, and keep your name only on the few approvals that can materially change the business.

How do you choose clients the Essentialist way?

Choose clients who fit your delivery style and payment habits, not just your revenue target. If a prospect requires constant exceptions, slow approvals, or vague scope, you may be trading focus for avoidable admin drag. Next step: add a short screening checklist to discovery calls and walk away when a client fails your baseline on scope clarity, payment process, or responsiveness.

What should your contracts cover first?

Keep the agreement clear on scope, payment timing, change requests, and who can approve extra work. You do not need a long contract to reduce friction, but you do need language that matches how you actually work, with local legal specifics verified separately by jurisdiction. Next step: review your last project dispute or near-miss, then revise the contract section that would have prevented it.

What financial habit matters most?

Keep a standing appointment with yourself to review your business finances. That can give you a cleaner read on cash movement, unpaid invoices, and odd transactions without relying on memory. Next step: block a recurring review on your calendar and save the same notes and records each time.

How often should you review your Essentialist OS?

Use a review rhythm you can actually keep, because a habit you drop after a short burst is less useful than a lighter one you sustain. A 30-day push may not be long enough for a sticky habit for everyone. Next step: schedule your next three review sessions now and use the same agenda until it becomes automatic.

How do you adapt this if you operate across multiple countries?

Treat each country as its own verification task, not as a place to reuse assumptions from somewhere else. Your setup can stay simple, but your checks should be country-specific for residency, invoicing, banking, and record retention, and you should verify local rules before you act. Next step: build a country-by-country register and mark each item as verified, needs advice, or not applicable.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- github.com/ever-works/awesome-time-trackingexternal

- gruv.ai/blog/a-guide-to-essentialism-for-solopreneursexternal

- katuva.com/top-business-books-solopreneurs-2025external

- sekarlangit.substack.com/p/essentialism-your-mindset-to-embodyexternal

- sidehustlenation.com/essentialism-the-one-thingexternal

- tim.blog/2019/01/09/greg-mckeown-essentialismexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

The Best Productivity Systems for Freelancers: GTD, PARA, and Second Brain

**Treat productivity as a system you can run under load, not a vibe you summon on demand.** Client work is messy by default: requests scattered across Gmail and Slack, scope shifting midstream, and the annoying truth that "done" does not always mean "paid."

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.