Quick Answer

Start by selecting one provable route, then confirm that route’s exact requirements inside the authority channel you will use. For a dubai retirement visa application, align your file to the processing path and rely on in-channel wording when outside guides disagree. Keep the first submission tight: identity records, retirement or age proof, and only the financial evidence tied to your chosen route. That approach reduces avoidable delays from mixed thresholds and document rework.

Dubai retirement visa in plain English#

This is a retirement residence route. Your main job is to choose one eligibility path you can prove clearly, then file through the official channel that handles that path.

At the UAE level, the route is the Residence visa for the retired. The baseline is at least 55 years old at retirement and at least 15 years of work inside or outside the UAE. After that, you need to meet one listed financial condition.

What is officially confirmed#

The UAE government page, updated 19 Feb 2026 in the excerpt provided, describes a 5-year long-term visa for retired foreigners. Use that as your baseline before you rely on third-party summaries.

The same page also identifies the filing checkpoints:

- ICP for a retired foreigner entry permit

- GDRFA Dubai for issuing a retired foreigner residence permit

If a guide conflicts with the channel you will actually use, follow the channel wording.

Where confusion starts#

Most confusion starts with the financial thresholds. The official page includes AED 180,000 annual income and separately states that for Dubai, annual fixed income must not be less than AED 240,000. Non-official guides then convert those into monthly figures, but they do not agree. You will see AED 15,000 versus AED 20,000, and some also state AED 15,000 for Dubai.

The safer move is not to plan around one universal monthly number. For Dubai filings, use the Dubai-specific official wording as your planning baseline unless the filing channel says otherwise.

Pick your route first. Before you start collecting documents, decide which path you can prove most clearly. From the official excerpt, that means either:

- an income-led route

- a combined asset route with property/properties of at least AED 1 million and financial savings of at least AED 1 million

That combined wording matters. If your income is easier to document consistently, start there. If your case depends on property, confirm the evidence requirements in the filing channel before you spend money on prep.

Verify before you spend. Do this two-step check before you pay for fees, translations, or attestations:

- Copy the exact requirement text from the official UAE page for your route.

- Confirm the matching service wording in ICP Smart Services or GDRFA Dubai.

Then build a focused first file: identity details, proof of age and retirement history, and only the financial evidence for the route you chose. Avoid mixing documents from conflicting summaries, because that can force a file rebuild later.

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

What this visa is and what it is not#

At the official UAE level, it is described as a 5-year long-term residence option for retired foreigners.

One non-official guide says it grants residency but not employment. Treat that as useful caution, not final legal wording, because the government excerpt provided does not present this route as a work authorization tool.

Use non-official overview pages for orientation only. For decisions, rely on the named application channels: ICP Smart Services for the retired-foreigner entry permit and GDRFA Dubai for the retired-foreigner residence permit. If sources conflict, copy and follow the exact service wording in the channel where you will file.

For thresholds, stick to the official annual wording: AED 180,000 as the broader baseline and AED 240,000 fixed income for Dubai applications. A secondary guide reports monthly versions of these numbers, so verify directly in ICP or GDRFA if your case is close to the line.

If your goal is a non-retirement route, review UAE Golden Visa Program separately before you file. Also, do not assume the process is fully online from start to finish. At least one secondary report notes that first-time applicants may still need a biometric centre visit.

For another visa walkthrough format, see A Guide to Colombia's Digital Nomad Visa and Tax Implications.

Which eligibility rules to trust first#

Trust the wording in the application path you will actually use, and keep secondary summaries separate until they match it. Orientation pages can help you understand the route, but they are not enough on their own for prep decisions.

Start with a simple rule hierarchy#

- The live requirements shown in the filing channel you will use

- Checkpoints that are stated consistently across the provided material

- Media, developer, and consultancy summaries

If a rule appears only in secondary summaries, treat it as unconfirmed.

Verify these checkpoints before collecting documents#

For property-route cases, the provided material points to checks that can directly affect cost and eligibility:

- minimum applicant age: 55 years

- passport validity: more than 6 months

- medical insurance: stated as compulsory for residence permit applications

- title-deed value: at least 1 million AED

- property-route evidence: an official evaluation certificate is stated as mandatory

- document consistency: the title-deed name must match the passport name

Check ownership structure early too. One provided page states that if joint shares are unequal, only the highest shareholder may apply as the primary visa holder.

Keep "confirmed" and "reported" in separate columns. That will save you time later, especially if you need to defend a document choice during review.

| Officially confirmed in your filing path | Reported in secondary summaries |

|---|---|

| Exact service labels and document names | General "who qualifies" summaries |

| In-channel mandatory fields and checkpoints | Simplified threshold conversions |

| Route-specific evidence requirements | Broad claims about renewal or work rights |

Do not merge these columns. In the material provided, renewal language differs between sources, so plan on continued eligibility being required unless your filing channel states otherwise.

This pairs well with our guide on A Guide to Getting a Golden Visa in Portugal.

Reconciling the income, savings, and property mismatch#

If income, savings, and property figures do not line up across sources, treat them as unsettled until an official filing authority confirms them. Plan conservatively before paying fees or ordering documents.

| Route area | What is confirmed from approved material in this section | What unverified summaries may add | What to confirm through the official filing channel before paying |

|---|---|---|---|

| Income | Confirm with the relevant authority | Specific income or pension thresholds presented as settled. | Exact minimum, accepted income types, and required proof format. |

| Savings | Confirm with the relevant authority | Specific balance thresholds, account conditions, or holding-period claims. | Exact amount, acceptable account types, and required bank evidence. |

| Property | Confirm with the relevant authority | Specific value cutoffs and document rules, including Title deed and Official valuation certificate language. | Whether Title deed is required, whether an Official valuation certificate is required, and what ownership pattern is accepted for your path. |

What stays unresolved until verified. Until the official filing channel confirms the live wording for your path, keep these points open:

- exact income minimum

- exact savings minimum

- exact property value threshold

- whether income, savings, and property can be combined or must stand alone

- whether Title deed alone is sufficient evidence

- whether an Official valuation certificate is mandatory

Keep each route in its own column until the filing channel merges them for you. That keeps your prep clean and lowers the risk of paying twice for the wrong documentation.

Related reading: A Guide to Greece's Digital Nomad Visa and its 50% Tax Break.

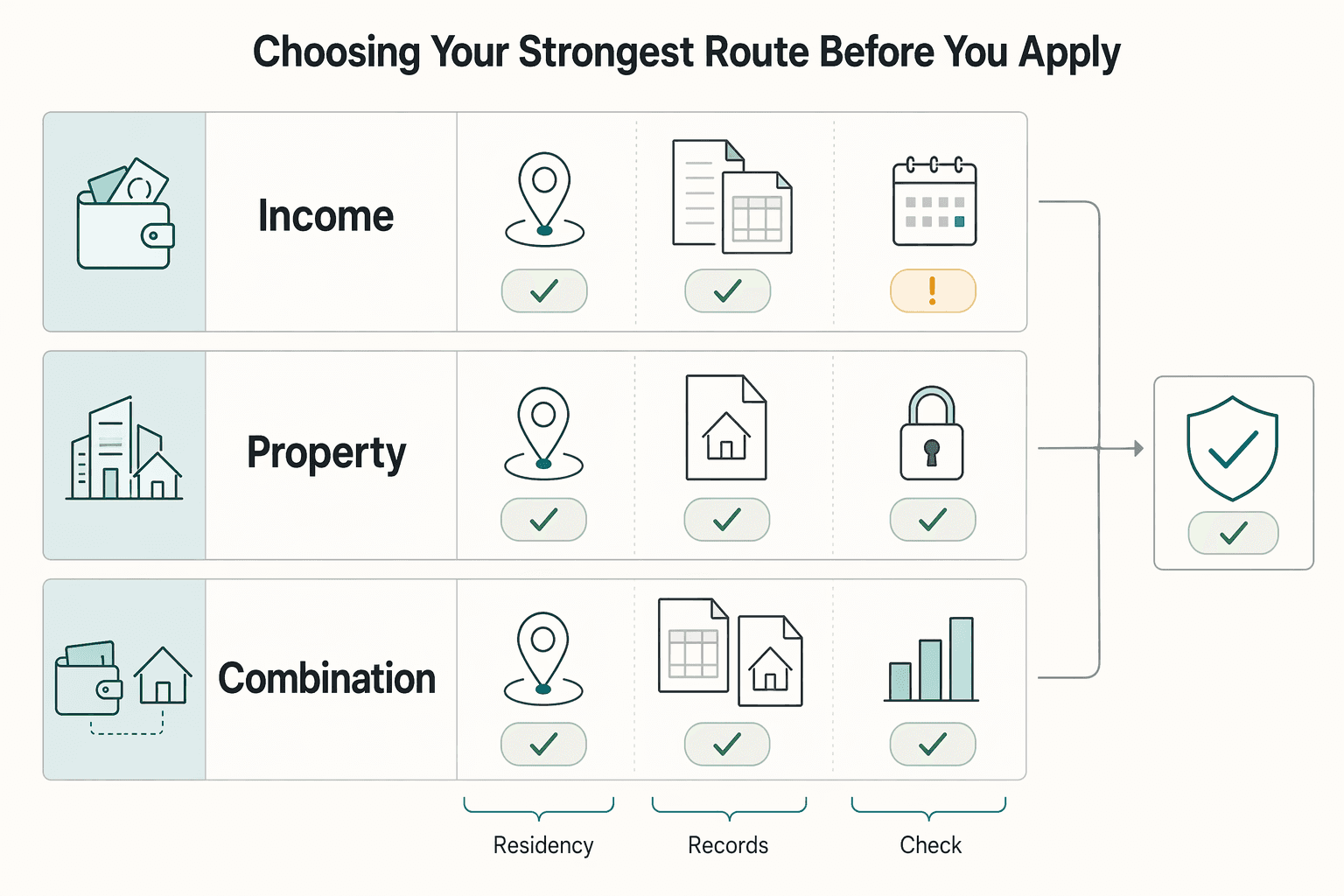

Choosing your strongest route before you apply#

Choose the route you can prove most cleanly with documents you already have, not the route that looks most flexible on paper.

| Route | Best fit | Evidence noted | Key caution |

|---|---|---|---|

| Income | Salary or pension continuity is your best evidence | Bank statements for the last 6 months that clearly match the income source | Do not build the plan around a borderline interpretation of reported monthly figures |

| Property | Property records are complete and clear | Title deed, valuation, registration, and proof of no liens or seizure | Do not assume gross value is enough if the property is encumbered |

| Combination | Neither standalone route is clearly stronger | Use mixed evidence only after you have confirmed how it is handled | Confirm how combined evidence is treated before you rely on it |

For the Residence Visa for the Retired, eligibility is framed as age plus financial evidence. The financial side may be one route or a combination, but that flexibility only helps if your proof is strong and consistent.

- Choose the income route first when salary or pension continuity is your best evidence.

- Choose the property route first when your property records are complete and clear.

- Choose a combination route only when neither standalone route is clearly stronger and you have confirmed how mixed evidence is handled.

For an income-led file, continuity is the key checkpoint. You want last 6 months of bank statements that clearly match the income source you are relying on. Non-official guides often cite AED 180,000/year (AED 15,000/month) for Dubai and note that figures can vary by emirate, so do not build your plan around a borderline interpretation.

For a property-led file, validate the document chain before you pay for anything extra. The key evidence set is title deed, valuation, registration, and proof of no liens or seizure. If the property is encumbered, do not assume gross value is enough. The guidance says the property should be unencumbered, or the equity portion must meet the requirement. Also confirm what form of valuation evidence your route expects.

If your documents are spread across countries, prefer the route with fewer cross-border dependencies and the clearest evidence set.

For a separate residency-planning example, see A Guide to Getting a Golden Visa in Greece.

Building your document pack without rework#

Build one document pack for one filing path, then validate it in the exact channel you will use. For retiree cases, anchor your checklist to the ICP Smart Services flow under Resident - Retiree. ICP directs applicants to use the correct category for terms, fees, and required documents.

If you expect an initial Residence entry permit for retired foreigner step, handle it carefully. The page referenced here is a renewal page, not a full initial-entry checklist. It is still useful as a control list because ICP states that renewal must maintain residence-issuance requirements.

| Checklist folder | What to prepare now | What to verify before upload |

|---|---|---|

| Identity | Passport valid for no less than 6 months; retirement or age proof such as a work certificate proving retirement and service period, or birth certificate | Core identity details are consistent across documents |

| Financial proof | Income route: bank certificate confirming fixed annual income plus bank statements for the last 6 months | Statements show the same account holder and a clear income pattern for your chosen route |

| Insurance proof | Evidence of valid health insurance | Policy is active and document details are complete and readable |

| Route-specific evidence | Property route: municipality certificate confirming property ownership plus a certificate from the competent authority assessing property value(s), or a mortgaged title deed showing AED 1 million paid to release the mortgage | Issuer is the correct authority, ownership details are clear, and mortgage status is explicit |

Property files need an extra validation pass. Property files can fail on document quality, not just headline value. Validate ownership details early and resolve obvious mismatches before submission. Then confirm that your valuation document is issued by the competent authority. If the property is mortgaged, make sure your evidence clearly supports the AED 1 million paid-to-release condition you are relying on.

Insurance and a final consistency check. Set the insurance evidence before final upload, since valid health insurance is part of the required documentation. Then do one final consistency pass. Keep core identity details consistent across the full pack and the application profile tied to Emirates ID processing. Keep one dated master folder after submission as well. That helps if you need a renewal follow-up later, especially because ICP notes an overstay fine of AED 50 per day after visa expiry or cancellation.

Need the full breakdown? Read A Guide to Getting a Golden Visa in Spain.

Before you submit, keep one tracker for document details, expiries, and residency timing so your file stays consistent across channels. Use the tax residency tracker to organize that timeline.

The 30-60-90 day timeline from prep to Emirates ID#

Use this 30-60-90 plan as a conservative buffer, not as an official ICP or GDRFA processing timeline. One practical delay risk is file drift, where route logic or identity details change after the process starts.

| Stage | Main goal | Checks and risks |

|---|---|---|

| First 30 days | Lock one eligibility route and build one matching file set | Check passport validity at 6+ months, keep name formatting consistent, and validate route evidence early |

| By 60 days | Submit a complete file and respond quickly to questions | Avoid switching routes after submission and avoid name or detail mismatches across key documents |

| By 90 days | Handle post-approval formalities without rebuilding eligibility | Exact order can vary; leave slack for appointments and follow-ups, and keep the same route and core identity details |

First 30 days#

Your first-month goal is to lock one eligibility route and build one matching file set. Treat the route as a single-path choice, property, savings, or income, then align every document to that choice before filing.

Check the basics early: passport validity at 6+ months, consistent name formatting across records, and clear route evidence such as bank statements or title-deed-based property evidence. Validate your pack in your chosen filing flow early instead of adapting a generic checklist later.

By 60 days#

By day 60, the priority is a clean submission and a fast response to any questions. File only when the documentation is complete and payments are cleared, then answer follow-up requests with a tight, consistent evidence set.

Two avoidable failure modes in this plan are:

- switching routes after submission

- name or detail mismatches across key documents

Do not try to patch weak eligibility with altered paperwork. Questionable documents can trigger strict action.

By 90 days#

By day 90, the goal in this planning scaffold is post-approval formalities, not rebuilding eligibility. The exact order of steps can vary, so do not assume one universal sequence.

Plan insurance as part of that sequence. One retirement-visa summary says it is required before visa stamping and must stay valid through the visa term. Keep room in your budget for that stage. Published estimates in non-official sources, AED 3,000-10,000/year, are not official fee schedules, but they are still useful for rough planning.

Leave schedule slack for medical-related steps and Emirates ID completion, as timing for appointments and follow-ups can vary. Your day-90 checkpoint is simple: same route, same core identity details, and stable evidence from start to finish.

Picking the right application channel the first time#

Choose the channel based on who will actually process your file, not on whichever portal is easiest to open first. For a Dubai case, that usually means ICP (icp.gov.ae) for federal online submission paths, GDRFA for savings- or income-based residency processing, and DLD for property-led Dubai routes, with Amer as an in-person support channel.

Match the channel to your route before you submit#

Start with the handling authority, then build the file to match it.

| Channel | Use when | Notes |

|---|---|---|

| ICP | You are following a federal online workflow | Confirm the exact service path in the same channel before you pay |

| GDRFA | Your Dubai residency processing is tied to savings or income | Document checks are reviewed against GDRFA requirements before submission |

| DLD | Your file is a Dubai property route | Published guidance commonly points here, but confirm the exact handling path in-channel before you file |

| Amer | You need in-person support | In-person support channel |

- Use ICP when you are following a federal online workflow.

- Use GDRFA when your Dubai residency processing is tied to savings or income.

- For Dubai property routes, published guidance commonly points to DLD, but confirm the exact handling path in-channel before you file.

Treat orientation pages as guidance, not final routing logic. Before you pay, confirm the exact service path in the same channel you will use to submit: service name, handling authority, and route logic. That matters because document checks are reviewed against GDRFA or DLD requirements before submission.

Property files need an extra verification step. If your file includes Dubai property, confirm whether the relevant retiree residence service is being handled through DLD steps and whether any additional authority step applies. Then build your documents to that path. Property-route packs may include title deed, valuation, registration, and proof of no liens or seizure. Also remember that requirements may vary slightly by emirate, so do not assume one checklist transfers cleanly across all routes.

Cost planning when fee numbers conflict#

When fee numbers conflict, treat only channel-confirmed amounts as planning inputs. Everything else belongs in the estimate column until you verify it in writing.

For this route in Dubai, do not chase one all-in total too early. Build a simple cost sheet by bucket, then mark each line as either officially published in channel or reported estimate. That keeps your budget tied to the authority actually handling your file and stops unclear numbers from driving your move date.

| Cost bucket | What to capture | What counts as channel confirmed | If still unconfirmed |

|---|---|---|---|

| Filing fees | Application or residence-processing charges from the handling authority | A current amount shown in the actual submission or payment flow, or written confirmation from that channel | Keep as estimate and do not use it to lock your move date |

| Medical-related steps | Any medical step listed in your route, and its payable amount | The step appears in your route and the amount is shown in portal flow or writing | Keep as estimate until both step and amount are confirmed |

| Emirates ID | ID-related charges if they appear separately in your flow | Amount shown in the same channel sequence for your case | Do not assume it is included elsewhere |

| Insurance | Your policy quote and any plan options you are evaluating | A dated quote in your name plus confirmation it is acceptable for your route | Keep as estimate until acceptability and cost are confirmed |

Use one rule for every line item: if you cannot show the source screen, email, or quote, it is not confirmed. That matters because the route is framed around financial self-sufficiency, and private health insurance is part of the broader financial-evidence picture.

Do not lock dates too early. Do not lock nonrefundable travel, shipment bookings, or lease deadlines until the channel-confirmed costs are in writing. If a required item is still sitting in the estimate column, your timeline is still provisional.

Keep a still-unconfirmed list. Before you pay, make sure you can answer these in writing:

- Which exact filing fee applies in the channel handling your route

- Whether medical-related steps are paid separately, and when

- Whether Emirates ID charges are billed separately

- Which insurance evidence is acceptable for your profile, and whether your selected policy quote meets that requirement

Property route pitfalls that cause preventable delays#

An avoidable source of delay in a property-led application is treating unverified document assumptions as settled requirements. In this section's evidence set, there is no official retirement-visa rule source confirming Title deed requirements, Official valuation certificate requirements, or joint-ownership treatment. One excerpt is a State.gov cookie banner, and the other is a general UAE expat money article, so neither should be used as a property-route rulebook.

What to do before you submit. Keep the property route provisional until the handling channel confirms the rules in writing.

- Treat your property route as provisional until the handling channel confirms requirements in writing.

- Do not rely on forum summaries or third-party checklists as proof that your property pack is submission-ready.

- If ownership structure or document acceptability is still unclear, resolve that before filing instead of trying to reinterpret the route during review.

Renewal and continuity checks before year five#

Treat this as a renewable route, not a permanent one. The current materials describe the retirement visa as a 5-year residence permission that may be renewed after the first 5-year period if the retiree still meets the criteria.

Keep continuity evidence organized now#

Use a simple yearly tracker so renewal prep stays incremental instead of becoming a last-minute rebuild. This is practical housekeeping, not an official ICP or GDRFA checklist.

- Insurance continuity: medical insurance is described as compulsory for residence permit applications. Keep policy records and renewal proof together, including whether you use DHA Basic Insurance or Comprehensive Insurance.

- Identity records: keep your identity documents consistent across files, especially passport details.

- Route documents: retain the documents tied to the path you used to qualify.

If you qualified through property, keep this especially tight. One source states that an official evaluation certificate is mandatory and that the title deed name must match the passport name.

Recheck fit before renewal pressure starts. If your long-term plan changes, compare options before renewal becomes urgent. One supported comparison is that the retirement route is age-specific and 5-year, while the UAE Golden Visa Program is described as 10-year.

That comparison alone does not confirm your Golden Visa eligibility, but it is enough to justify a side-by-side review if your residency horizon has changed. Start that review early with the UAE Golden Visa Program. You might also find this useful: Dubai Virtual Working Program for Nomads Who Need Certainty.

Your next step to avoid delays#

Choose one financial qualification route now, and build your file only for that route. Avoidable delays usually come from mixing route evidence, changing direction mid-process, or relying on summaries instead of the rules shown in your actual filing channel.

Pick one route and keep the evidence focused. Treat this as an evidence decision. Build around the route you can prove most clearly: income, property, or savings. If your documents start telling multiple stories at once, you may face follow-up questions or delays.

Use one final pre-submission check: your document pack should support one route, and the core identity details should stay consistent across the file.

Verify rules in the channel you will use before paying. Different sources can describe the eligibility routes differently, including whether meeting one criterion is enough. Do not try to merge those versions yourself. Confirm the wording directly in your filing channel, for example, GDRFA Dubai, before you pay.

Also treat fast marketing timelines like "3 days" as promotional, not guaranteed service timing. Plan around document readiness and review risk instead.

Use a short execution checklist.

- Eligibility confirmed: your chosen route matches the live channel wording.

- Document pack validated: required documents are complete and consistent.

- Channel chosen: you know the authority path you will submit through.

- Timeline planned: you have buffer for review questions or resubmission.

- Cost buffer set: you separate confirmed charges from unclear costs.

If your plans may still include working, make that call before you submit. This route is for legal residency, not employment authorization. If needed, compare it with A Deep Dive into the UAE's Golden Visa Program for Freelancers before final submission.

Related: How to Manage Your Time Effectively as a Freelancer.

If you are deciding between retirement residency and other long-stay paths, plan the paperwork and timing side by side before filing. Explore Gruv planning tools.

Frequently Asked Questions

Who is eligible for a Dubai retirement visa right now?

The baseline official criteria are age 55+ at retirement and at least 15 years of work inside or outside the UAE. You also need to qualify through one of the listed financial routes. If your age or work-history proof is unclear, resolve that first before you build the rest of the file.

Is the financial route based on property and savings together, or can one route qualify on its own?

In the official wording provided here, the property path is combined: property/properties of at least AED 1 million and financial savings of at least AED 1 million. There is also a separate income-based path. For planning, do not assume property alone qualifies under this specific official summary.

What is the Dubai-specific income wording versus broader UAE wording?

The same official page shows two figures: AED 180,000 annual income in broader wording and AED 240,000 annual fixed income in Dubai-specific wording. If you are filing through a Dubai channel, plan against AED 240,000 unless the live submission path states otherwise. Confirm the exact wording in the channel you will actually use.

Which documents are mandatory before I start the application?

The concrete items shown here include a passport valid for at least 6 months, a valid UAE health insurance policy, and retirement proof, such as a certificate confirming retirement after at least 15 years of service. If you are applying through the property route, ICP also lists a certificate proving property ownership. Keep identity details consistent across all submitted documents.

Should I apply through ICP, ICP Smart Services, or GDRFA Dubai?

Apply through the authority channel that processes permits. The official materials point to ICP / ICP Smart Services and GDRFA Dubai for retired-foreigner residence services. Use informational pages only for orientation. Final checks on terms, fees, and required documents should happen inside your actual submission channel.

What costs are confirmed versus still uncertain?

What is confirmed from the ICP service page is limited: you must select the right category to see the applicable terms, fees, and required documents, and the page shows an Application Fees - 100 AED line. What is not confirmed here is a complete retirement-specific fee schedule from that excerpt alone. The 500 AED line shown there is labeled for a 5-year multiple-entry tourist visa, not clearly for the retirement residence route.

How does renewal work, and what should I track before the first term ends?

The retirement visa term is 5 years. Renewal process details and a full renewal checklist should be confirmed with your submission channel. Treat renewal as conditional until requirements are confirmed. Track continuity each year for insurance, identity records, and whichever qualification route you used, whether that is income evidence or property and savings evidence.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- 2009-2017.state.gov/documents/organization/200506.pdftrusted

- 2009-2017.state.gov/j/ct/rls/crt/2014/239407.htmtrusted

- brandeis.edu/crown/publications/middle-east-briefs/meb163...trusted

- congress.gov/114/chrg/CHRG-114shrg47421/CHRG-114shrg47421...trusted

- govinfo.gov/content/pkg/FR-2015-06-22/xml/FR-2015-06-22.xmltrusted

- govinfo.gov/content/pkg/CHRG-109hhrg31363/pdf/CHRG-109hh...trusted

- state.gov/report/custom/4f29b1ed7atrusted

- state.gov/report/custom/18900bd23ctrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

How to Manage Your Time Effectively as a Freelancer

Most freelancers struggle not because they work too few hours, but because they misallocate the hours they have—treating time as an infinite resource rather than a finite business asset with a real cost per unit. The solution is a three-layer operating system: a Time Budget Framework that commits hours to four categories before any client work is booked, a Weekly Operating Template that assigns those categories to specific calendar windows, and a monthly Admin Audit Checklist that reconciles invoicing, bookkeeping, and compliance records. Multi-client orchestration requires a WIP limit, dedicated client windows, and a capacity decision rule run before accepting new engagements. Together, these systems replace reactive decision-making with a repeatable structure that keeps delivery quality consistent, records audit-ready, and the freelance practice operationally durable.

UAE Golden Visa for Freelancers and the Green Visa Decision Guide

Choose the route your documents can support now, not the visa label with the most search volume. If you searched for `uae golden visa for freelancers`, use that as a starting query, then choose between Golden Residency and the Green route based on the evidence you can actually file.