Quick Answer

Yes - deducting business meals in 2026 is usually limited to 50% when the expense has a clear business purpose, you or an employee is present, and records are complete. Keep the receipt, list attendees when relevant, and write the objective while details are fresh. In entertainment settings, only food and beverage amounts listed separately from admission charges are typically supportable.

Deducting business meals in 2026 without creating audit anxiety#

Start with the current baseline: in 2026, qualifying unreimbursed non-entertainment business meals are generally limited to 50%, and the temporary full restaurant meal write-off applied only to 2021 and 2022.

That reset clears up most of the noise. The full deduction was temporary, and it applied only to restaurant meals paid or billed after December 31, 2020, and before January 1, 2023. It should not be your starting point now.

This guide is for a self-employed taxpayer dealing with mixed real-world charges without a finance team. Think client meals, travel-day food, and expenses that look business-related but may not be. The goal is not to find more write-offs. It is to separate defensible meal expenses from personal spending before they reach Schedule C (Form 1040) and your U.S. federal income tax return.

The scope here is intentionally narrow. It focuses on IRS guidance, regulations, and Publication 463. It does not assume state treatment is identical, and it does not generalize beyond U.S. federal rules.

Use these baseline tests repeatedly:

- The meal must have a clear business purpose.

- The expense cannot be lavish or extravagant under the circumstances.

- You, or an employee, must be present when food or beverages are provided.

- Meal cost can include taxes and tips.

- Transportation to and from the meal is not part of meal cost.

The common mistake is overclassifying by vibe. A meal near a meeting is not automatically deductible, and a travel-day dinner is not automatically personal or business. If you cannot explain the business reason later, treat it as unresolved until you can support it.

A practical checkpoint helps at the time the charge posts. Can you tie it to a real client, project, trip, or business discussion while details are still fresh? If yes, save the receipt and context immediately. If not, keep it out of the deduction bucket for now.

By the end of this guide, you should be able to classify each meal, keep the proof you need, and know when to escalate before filing.

You might also find this useful: A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

Start with the current rule and define the terms that matter#

For 2026 planning, the safest starting point is current IRS guidance: unreimbursed non-entertainment business meals are generally limited to a 50% deduction, not 100%. The temporary full deduction for qualifying restaurant meals applied only to 2021 and 2022 for amounts paid or incurred after December 31, 2020, and before January 1, 2023.

Use the current baseline, not old blog posts#

Use current IRS guidance as your default. The IRS states that unreimbursed non-entertainment business meals are generally subject to the 50% limit, and Publication 463 reflects that the temporary 100% treatment expired. If you see claims about a broad 2026 reset, treat them as unverified unless they match IRS or Code-level language.

The terms that actually control the outcome#

- Ordinary and necessary expense: To be deductible, a business expense must be both ordinary and necessary.

- Active conduct of your trade or business: Regulatory language uses this phrase to require a direct business connection, not merely personal consumption.

- Lavish or extravagant expense: Publication 463 does not set a fixed dollar cap. The test is whether the cost is reasonable under the facts and circumstances.

A practical rule before you classify anything#

If you cannot state the business purpose in one sentence, do not classify it as a business meal yet. A receipt helps, but a canceled check alone does not establish business purpose. Your records still need to show the business purpose and how the meal tied to your business.

For a step-by-step walkthrough, see Can Digital Nomads Claim the Home Office Deduction?.

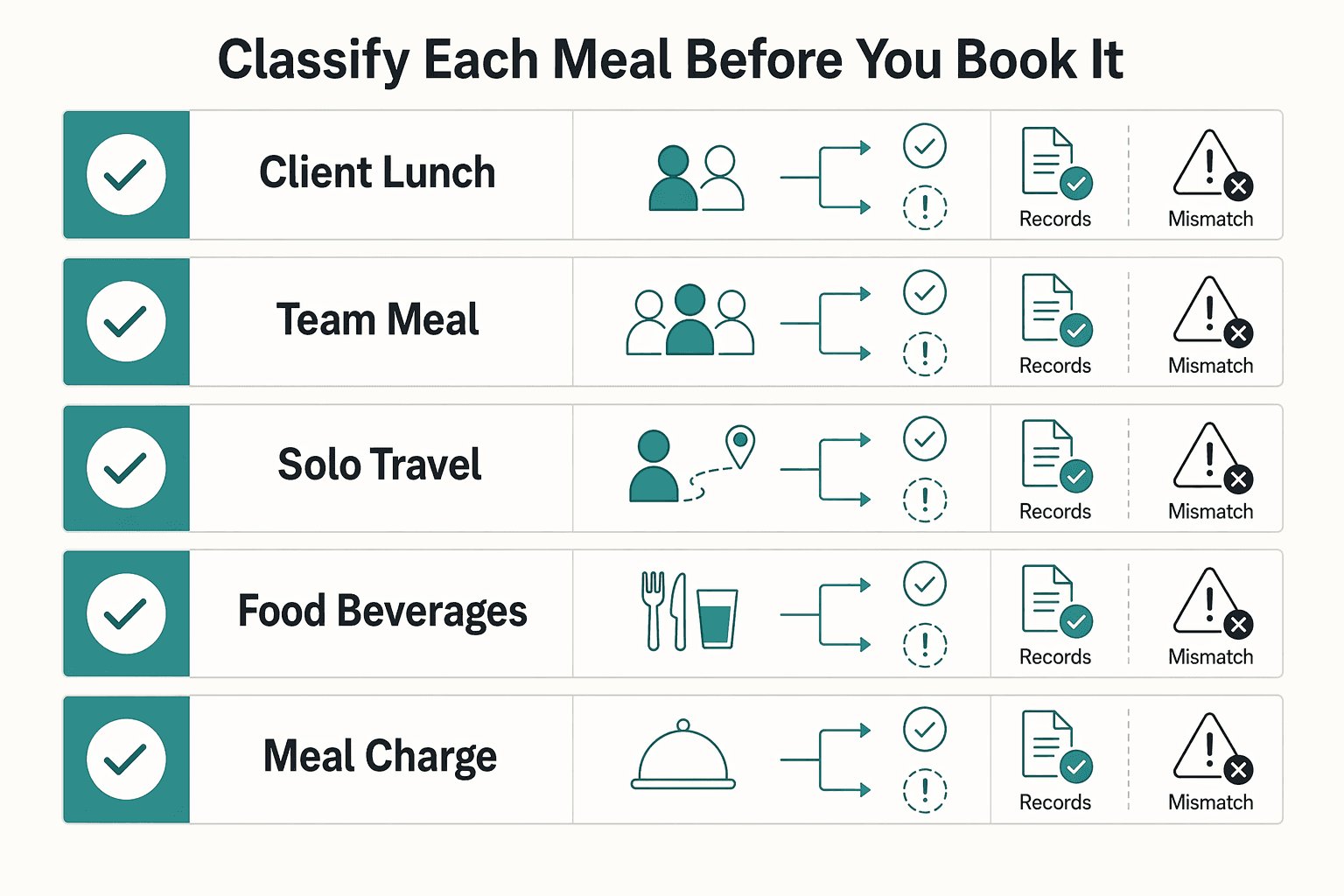

Classify each meal before you book it#

The biggest control point is classification at the time of booking, not at tax time. Deductibility turns on the scenario, who was present, and how well the charge is documented. A qualifying non-entertainment business meal is generally 50% deductible, not fully deductible.

| Scenario | Deductible status | Required proof | Common failure mode |

|---|---|---|---|

| Client lunch with a client or other business associate, and you or your employee are present | Likely deductible (generally 50%) | Receipt or paid bill with restaurant name/location, date, amount, and number of people served, plus a record of attendees and business purpose | Receipt exists, but no clear record of attendees or business purpose |

| Team meal with an employee tied to business activity | Likely deductible (generally 50%) | Receipt or invoice, date, amount, attendees, and business purpose; enough detail to show it was for you or an employee and not lavish or extravagant | Logged as a general “staff meal” with no business context |

| Solo travel meal on a business trip | Likely deductible (generally 50%) only if travel is overnight or long enough to require substantial sleep or rest | Receipt plus travel date/location/amount and a record linking it to business travel | Claimed as travel meal even though the trip did not require sleep or rest |

| Food and beverages at an entertainment event | Partially deductible only if food/beverage cost is separately purchased or separately stated; entertainment is usually non-deductible | Bill/invoice/receipt that separately states food and beverages from entertainment, plus business purpose and attendee note | Bundled ticket or package with no separate food line |

| Meal charge missing a receipt, invoice, or itemized bill | Often disallowed or difficult to substantiate until records are rebuilt | Documentary evidence where required, plus your own record of time, place, amount, and business purpose | Only a card statement or bank line, with no substantiation of business purpose |

The highest-impact check is straightforward: you, or your employee, must be present, and the food or beverages must be provided to you or a business associate. The biggest overclaim risk is entertainment. If food is not separated from the entertainment charge, treat it as a non-deductible entertainment expense.

Before you post the expense, verify two things. First, make sure your documentation is complete. For $75 or more, documentary evidence is required; below that, you still need strong records of time, place, amount, and business purpose. Second, make sure your business note is specific. If you cannot write a one-sentence purpose, do not classify it as a business meal yet.

Book conservatively:

- Client meals, employee meals, and qualifying travel meals:

50% meals - Entertainment with a separate food line:

meals tied to entertainment - review - Missing documentation:

unclassified - records missing

Include taxes and tips in meal cost, but keep transportation to and from the meal out of the meal line. The IRS discussion in Publication 463 is the best primary reference when you are checking what belongs in the meal amount.

Use a three-step yes or no test before claiming any meal#

A simple gate can help you triage unclear charges. If any step fails, book the charge as personal or unresolved for now and revisit it only if you can improve the record.

Step 1. Test the business purpose#

Start with a specific commercial objective you can write in one sentence. Tie it to something concrete in your records, like a client, project, proposal, trip, or calendar event. If your note is vague, for example just "networking," treat it as a no for now.

Step 2. Confirm context#

Next, check whether the setting and activity clearly support the business objective you wrote in Step 1. Record the business context connected to the meal. If the context is mostly social, or you cannot clearly explain why the meal happened, keep it out of the claim pile until you can.

Step 3. Verify your records#

Then review the file before you claim anything. Keep documentation that explains what the charge was and how it connects to the business purpose you recorded.

Before finalizing treatment, make sure you are using current IRS guidance. Publication 463 is Travel, Gift, and Car Expenses, and this excerpt is marked for preparing 2025 returns. The IRS also says to check IRS.gov/Pub463 for Future Developments, including changes enacted after publication. The Schedule C instructions include a Business meals deduction topic, so use that as a pointer and confirm current rule text before you file. This excerpt alone does not provide step-level meal-deduction rules.

Separate meals from entertainment so you do not overclaim#

This is where a lot of otherwise reasonable deductions fall apart. Do not claim entertainment as a meal expense unless the food and beverage cost is separately purchased or clearly separated on your documents. Under Section 274, entertainment is generally nondeductible, so your meal position is strongest when the meal amount is carved out on the paperwork.

This often comes up at games, concerts, suites, and similar events. Entertainment is defined broadly as amusement or recreation. Food and beverages are not automatically treated as entertainment, but if they are provided at or during an entertainment activity and not separately identified, your deduction position weakens fast.

Use the separate billing test#

Use a simple rule: check the bill, invoice, or receipt first. Food and beverage costs should be separately purchased or separately stated from the entertainment charge. Publication 463 reflects the same logic in its game-ticket example: separately stated food and beverage charges are not treated as entertainment expense. For meal deductions, that separation usually determines whether you have a supportable partial deduction or an overclaim risk.

| Situation | Treatment | What to verify |

|---|---|---|

| Event ticket plus separate receipt for food and drinks | Meal cost may be treated as a meal expense if normal meal rules are met | Keep both records so the meal amount is clearly separate |

| Event or suite invoice with tickets on one line and catering on another | Catering line may be treated separately from entertainment | Confirm distinct dollar amounts, not a package-only description |

| One bundled charge for admission, parking, and food | High-risk position; allocation is generally not allowed | Do not create a meal split after the fact |

Where people get into trouble#

The most common failure mode is a bundled charge with no food breakout. Final Section 274 regulations say that when food or beverage is not separately purchased or separately stated from entertainment, you generally cannot allocate part of that bundled amount to meals.

In practice, bundled invoices often combine seats, parking, and catering into one total. Without clear, separate meal charges, the full amount may be treated as nondeductible.

What to keep in your file#

Your file should let someone else identify the meal amount from documents alone. Keep:

- Itemized invoice or receipt showing separate food and beverage charges

- Ticket or admission record, when relevant

- Any related record that helps show the meal amount was separately charged

If the meal amount is properly separated and the meal otherwise qualifies, the usual limit is generally 50% of cost. The temporary full deduction for restaurant meals applied to 2021 and 2022 only.

Looking for the current rule summary instead? Review the IRS FAQ on deducting business expenses before you classify edge cases.

Handle client meals and travel meals with stricter documentation#

Client meals and travel meals can both qualify, but travel meals usually need a deeper proof trail because you need support for both the meal and the trip.

| Scenario | What you need to prove | Documentation focus |

|---|---|---|

| Local client meal | You, or your employee, were present, and the meal had a business context with a client or other business contact | Receipt plus a short note on the business contact and purpose |

| Travel-day meal | The meal and that the trip qualifies as business travel away from your tax home | Travel context plus meal support: temporary assignment (more than 1 year is treated as indefinite), and travel that is overnight or long enough to require sleep or rest |

What counts as the meal cost#

Keep the meal amount tight: food, beverages, taxes, and tips. That is the amount you generally test against the 50% limit.

Do not blend in non-meal charges. If a meal happens during entertainment, only separately purchased or separately stated food and beverage amounts belong in the meal file. The entertainment charge stays out.

Documentation depth changes by scenario#

For local client meals, you are mostly proving business purpose and attendance. For travel meals, you are proving both the meal and the trip.

If you use actual costs, keep records of actual amounts. If you use the standard meal allowance, you still need records for time, place, and business purpose of the travel.

Use this order every time#

A consistent order helps avoid year-end reconstruction:

- Capture the receipt as soon as practical.

- Add a short purpose note while context is still clear.

- Tie the transaction to the client, trip, or project in your books.

If you already keep a trip packet for airfare, lodging, and dates, store meal support in that same packet. This keeps travel-meal review clean and aligns with the IRS explanation of what kind of records you should keep.

Build an evidence pack you can defend in minutes#

Low-stress meal deductions come from records that are easy to review. The Internal Revenue Service (IRS) puts the burden of proof on you, and organized files make both filing and examination support easier.

Capture the same fields every time#

For each meal, keep one complete record with the core details and documentary proof.

| Field | What to record | Why it matters |

|---|---|---|

| Date | Transaction date and, for travel meals, trip date range | Supports when the expense was incurred and helps match books |

| Location | Restaurant or venue name and city | Supports where the expense happened |

| Attendees (if applicable) | Names of clients, prospects, employees, or other business contacts present | Adds business context to the record |

| Business purpose | One specific sentence with the commercial objective | Distinguishes business purpose from personal spending |

| Amount | Food, beverages, taxes, and tips | Keeps the meal amount tight; excludes transportation and entertainment charges |

| Proof type | Underlying receipt, invoice, or bill | Provides the documentary evidence expected for expense support |

Keep purpose notes specific. “Discussed contract renewal terms with Client X” is stronger than “business meeting.”

Use a folder structure that is easy to review#

The IRS does not require a monthly structure, but it does expect records to be orderly and organized by year and type. A monthly meal folder setup is a practical way to do that.

2026 TaxesBooks exportMeals/01 JanuaryMeals/02 FebruaryMeals/03 MarchTravelIncomeBank and card statementsFiled return

Inside each monthly meal folder, keep the receipt file, purpose note, attendee context (if applicable), and bookkeeping reference. Use sortable file names like 2026-03-14_ClientX_lunch_84-60_receipt.pdf.

Build in a quarterly check before errors pile up#

Do not wait until year-end to find support gaps. Use a quarterly spot-check of a small sample of entries as an internal control, not an IRS rule. Check for missing business-context notes, vague purpose notes, and missing underlying proof.

For meals tied to entertainment, verify that food and beverage costs are separately stated on the bill, invoice, or receipt. If they are bundled into a single entertainment charge, that meal cost may not qualify.

Keep records on a retention schedule you can actually follow#

Use retention rules, not memory. Default retention is 3 years when special exceptions do not apply. Keep records for 6 years if omitted income is more than 25% of gross income shown on the return, 7 years for certain bad debt or worthless securities claims, and indefinitely if no return was filed or a fraudulent return was filed.

A practical habit is to lock the full-year folder with the filed return copy after filing. Keep it at least 3 years, then check whether a longer period applies before deleting anything. If you are self-employed, keep the same type of travel records an employee would keep.

If you want a cleaner monthly audit trail, use the Tax Residency Tracker to keep dates, locations, and filing-jurisdiction notes in one place.

Tie meal deductions to bookkeeping and filing steps#

Treat this as a control step. Keep meal records clean from bookkeeping through U.S. federal income tax return prep, and keep uncertain items clearly flagged until they are resolved.

Map records into internal categories before return prep#

Do not wait until filing season to sort meal activity. For internal bookkeeping, use one consistent category for entries you tentatively include in meal totals. Use a separate review bucket for items that are incomplete or unclear.

That review bucket helps limit last-minute judgment calls. Book clearer items to your normal meals category, park weaker items in a temporary review account, and move them only after supporting details are complete.

Run a regular reconciliation: compare meal ledger totals and entry counts against your supporting records, then follow up on gaps before finalizing year-end totals.

Build a preparer-ready handoff#

When you hand this off, separate settled numbers from open questions.

| Handoff item | What to include | Why it helps |

|---|---|---|

| Meals totals | Year total and monthly subtotals from your books export | Lets the preparer trace totals back to your ledger |

| Exceptions log | Entries excluded or pending due to unclear support | Shows what you screened out instead of passing through |

| Unresolved judgment list | Brief notes on borderline items needing a preparer call | Keeps tax judgment questions separate from bookkeeping cleanup |

For each unresolved item, include date, amount, payee, and one clear sentence on the issue.

Keep meal files separate from other tax threads#

If you have multiple compliance threads, keep meal support in your expense records and keep foreign-asset reporting files separate. Form 8938 is used to report specified foreign financial assets, is attached to your annual return, and is filed by that return’s due date, including extensions. Filing Form 8938 does not replace FinCEN Form 114 (FBAR), which may still be required.

Keep separate workstreams, such as Meals, Books export, Form 8938, and FBAR, so totals and documents do not get cross-wired. For Form 8938, thresholds are not one-size-fits-all. A $50,000 trigger applies in some cases, and higher thresholds can apply for joint filers or taxpayers residing abroad.

This pairs well with our guide on How to Deduct Startup Costs for Your Freelance Business.

Address cross-border and state-level traps early#

Bookkeeping alone is not enough when more than one jurisdiction is in play. If your year includes time abroad, a state move, or services performed in multiple places, treat U.S. federal meal analysis as the starting point, not the full answer.

Federal first, not federal only#

Start with U.S. federal rules, then test local treatment. The IRS baseline is that U.S. citizens and resident aliens are taxed on worldwide income, and filing and payment rules are generally the same whether you are in the United States or abroad.

Do not assume that result carries everywhere else. Treaty treatment varies by country and income type, and treaty residency can differ from Internal Revenue Code residency in dual-status situations. A meal position that is supportable on your U.S. federal return may not be treated the same way in another country.

For meals during foreign travel or while living abroad, keep one extra note with the receipt. Record where you were tax resident at the time, if changing, and where the related services were performed. That makes later jurisdiction and sourcing decisions easier to defend.

Where California raises the stakes#

California is a practical example of why documentation posture matters early. The FTB generally follows federal law on many common business expenses, but it still expects documentary proof and calls out extra proof for travel, entertainment, gifts, and auto expenses.

Residency and sourcing also require facts, not a checkbox. California looks at temporary or transitory purpose and domicile. It taxes nonresidents on California-source taxable income, and for part-year residents applies worldwide-income and California-source concepts based on period. Services physically performed in California are one stated sourcing example.

So tie each meal to the surrounding work facts, not just the receipt. If you claim nonresident status but had a client meal in California, keep the calendar context, client or project tie, and support for where services were performed.

When to stop and get advice#

If residency or sourcing is unclear across jurisdictions, pause and get professional advice before claiming aggressively.

Use a stop rule when any of these apply:

- You changed countries or states midyear and are unsure when residency changed.

- You plan to rely on a treaty position and have not confirmed state treatment.

- Meals relate to work across multiple jurisdictions and your records do not show where services were performed.

For California exposure, keep records longer than your normal habit. The FTB says the usual period to examine a return and issue a notice is 4 years, so do not purge receipts and supporting notes right after filing.

If you want a deeper dive, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

When should you bring in a tax professional#

Consider bringing in a tax professional before you file when your meal records are incomplete or your facts cross multiple rule sets. At that point, the risk can shift from cleanup to denied deductions, entertainment misclassification, or missed parallel filings.

Use these escalation triggers:

- Substantiation gaps: Publication 463 and Section 274 substantiation rules require records that support amount, time, place, business purpose, and business relationship. If entries are missing receipts or key details, deductions may be denied.

- Meal vs. entertainment ambiguity: Entertainment is broadly disallowed, and food tied to entertainment generally needs to be separately stated on the invoice to be treated as a meal expense.

- Multi-layer compliance in one year: Escalate faster when meal claims overlap with travel, cross-border activity, or state documentation expectations, including California guidance that calls for additional proof in travel and entertainment categories.

- Form 8938/FBAR overlap: Form 8938 does not replace FBAR, and both may be required with separate penalties for failure to file each form.

A prepared packet can keep the meeting focused on decisions instead of reconstruction:

- categorized meal, travel, and entertainment ledger

- receipts and invoices, including separately stated food charges

- notes on missing documentation or mixed personal and business facts

- a short list of open filing questions

Good preparers will ask for records and receipts, and you remain responsible for filing a complete and correct return.

Related reading: the IRS Tax Topic on Business use of your home is a useful companion when you are separating meal records from other Schedule C expense buckets.

The takeaway for a low-stress filing season#

Use a conservative, repeatable process: claim only meal entries you can clearly explain and substantiate. For your U.S. federal return, a defensible file is usually better than pushing for every possible deduction.

The reason is simple. The burden of proof is on you. IRS guidance expects adequate records or other supporting evidence, and stronger substantiation comes from records made at or near the time of the expense.

Use one repeatable sequence#

Keep the process consistent every time:

- Classify the meal before it lands in a generic category.

- Save complete proof: bill, invoice, or receipt, plus context.

- Review entries on a regular cadence and remove weak items.

- File only claims that still hold up.

Publication 463 is a practical anchor because it explains deductible expenses, reporting, and required records. Use a quick yes or no check for each meal:

- Was there a real business purpose, not personal or social?

- Were you or your employee present?

- Do your records clearly support the amount and context?

If any answer is no, pause the deduction. This is especially important for meals connected to entertainment, where food and beverages may be deductible only when charged separately or separately stated.

What a defensible record looks like#

A defensible entry is simple and complete: receipt plus a short note with date, place, and business purpose (and who attended, when relevant). If you use a standard meal allowance for travel, you still need records supporting time, place, and business purpose.

| Checkpoint | What to verify | Common failure mode |

|---|---|---|

| Receipt quality | Bill, invoice, or receipt is saved and readable | Card statement only |

| Business context | Note explains why it was business-related | Vague or missing memo |

| Cost boundaries | Taxes and tips included; transportation kept separate | Transport costs mixed into meal total |

| Deduction boundary | Meal charges separated from entertainment charges | One bundled charge |

Be conservative with exceptions#

Most unreimbursed non-entertainment business meals are generally subject to the 50% limit, and the expense should not be lavish or extravagant under the circumstances. Personal, living, and family expenses are generally nondeductible unless a specific rule allows otherwise.

If an item is ambiguous or thinly documented, leave it out until you can support it. Before filing, clean up recent meal records, rerun your yes or no check on exceptions, and consider reviewing unresolved high-impact items with a qualified tax professional.

We covered related classification issues in How the IRS Classifies Your Side Hustle as a Hobby or Business.

Before you file, run a final consistency check with your tools and escalate any meal entries you still cannot defend.

Frequently Asked Questions

Can I still deduct business meals in 2026?

Yes. Qualifying business meals can still be deducted in 2026. The temporary full deduction ended, and the usual limit is generally 50% of meal cost rather than a full write-off.

Is the deduction usually partial or full, and why do older articles still mention the enhanced rule?

Usually partial. The IRS states the enhanced full deduction applied for 2021 and 2022 only, and otherwise the limit is usually 50% of the meal cost. Older articles still mention 100% because that temporary rule applied during a limited billing and payment window.

What proof does the IRS expect if my meal deduction is reviewed?

The IRS says businesses should follow the special recordkeeping rules for business meals. Keep clear records of the expense, and make sure they support that a business owner or employee was present when food or beverages were provided.

Are meals during an entertainment event deductible if the food is itemized separately?

Potentially, yes. Meal costs may be deductible when food and beverages are bought separately from entertainment, or separately stated on bills, invoices, or receipts. A single bundled entertainment charge with no food breakout is much harder to support as a meal deduction.

Do tips and taxes count as part of a business-related meal expense?

Yes. The IRS states meal cost can include taxes and tips. Apply the usual deduction limit to that qualifying meal total.

Is transportation to and from a meal part of the meal deduction?

No. The IRS is explicit that transportation to and from the meal is not part of business meal cost. Keep those transportation costs separate from the meal line item.

What should I do if I am unsure whether a meal was personal or business-related?

If you are unsure, do not assume deductibility. Only claim meals you can clearly support as business-related under the applicable rules and records.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

A Guide to Deducting Business Travel Expenses

**For deducting business travel expenses, use a repeatable compliance system so you only claim costs you can prove.**