Quick Answer

No - country-by-country reporting usually does not apply if you operate as a solo freelancer or consultant without a multinational group structure. It is an OECD/G20 BEPS Action 13 regime built for large enterprise reporting, with jurisdiction-specific consolidated revenue tests. First check whether your setup is actually part of a cross-border group, then confirm the local filing-year threshold. If those checks fail, focus on residency evidence, foreign-account duties, and invoice records.

Does Country-by-Country Reporting Apply to You? The 30-Second Answer#

For many freelancers, consultants, and business-of-one operators, the answer is usually no. You are generally outside scope unless you are part of a multinational enterprise group, not just working with clients in multiple countries. Use this quick scope check:

| Scope factor | Article detail | Effect on scope |

|---|---|---|

| Group structure | Part of a group with at least two enterprises that are tax-resident in different jurisdictions | If your setup is just you, or one small company delivering services across borders, you will usually fail the first test. |

| Revenue threshold | Country-by-country reporting revenue threshold in the filing jurisdiction for the preceding fiscal year | Many OECD-aligned regimes use a EUR 750 million preceding-year consolidated revenue threshold, while U.S. rules for qualifying parent entities filing Form 8975 use $850 million; thresholds are jurisdiction-specific. |

| Cross-border activity alone | Foreign clients, travel, and international invoices | Alone do not make you an in-scope multinational group. |

- Group test: Are you part of a group with at least two enterprises that are tax-resident in different jurisdictions?

- Threshold test: If yes, does your group meet the country-by-country reporting revenue threshold in the filing jurisdiction for the preceding fiscal year?

If your setup is just you, or one small company delivering services across borders, you will usually fail the first test. Foreign clients, travel, and international invoices alone do not make you an in-scope multinational group.

This regime sits under OECD/G20 BEPS Action 13. It is designed for large multinational groups and used by tax administrations for transfer-pricing and BEPS risk assessment. It is not a personal filing for independent professionals.

Practical checkpoint: verify both your group structure and your jurisdiction-specific threshold before you spend time here. Many OECD-aligned regimes use a EUR 750 million preceding-year consolidated revenue threshold, while U.S. rules for qualifying parent entities filing Form 8975 use $850 million. Thresholds are jurisdiction-specific, so confirm the in-force rule for your filing jurisdiction and preceding fiscal year. If you have a parent entity, subsidiary, or multiple tax-resident entities across jurisdictions, pause and confirm scope under local rules.

If that is not your fact pattern, your real compliance risks are elsewhere. The next section focuses on the filings and records that usually matter more. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

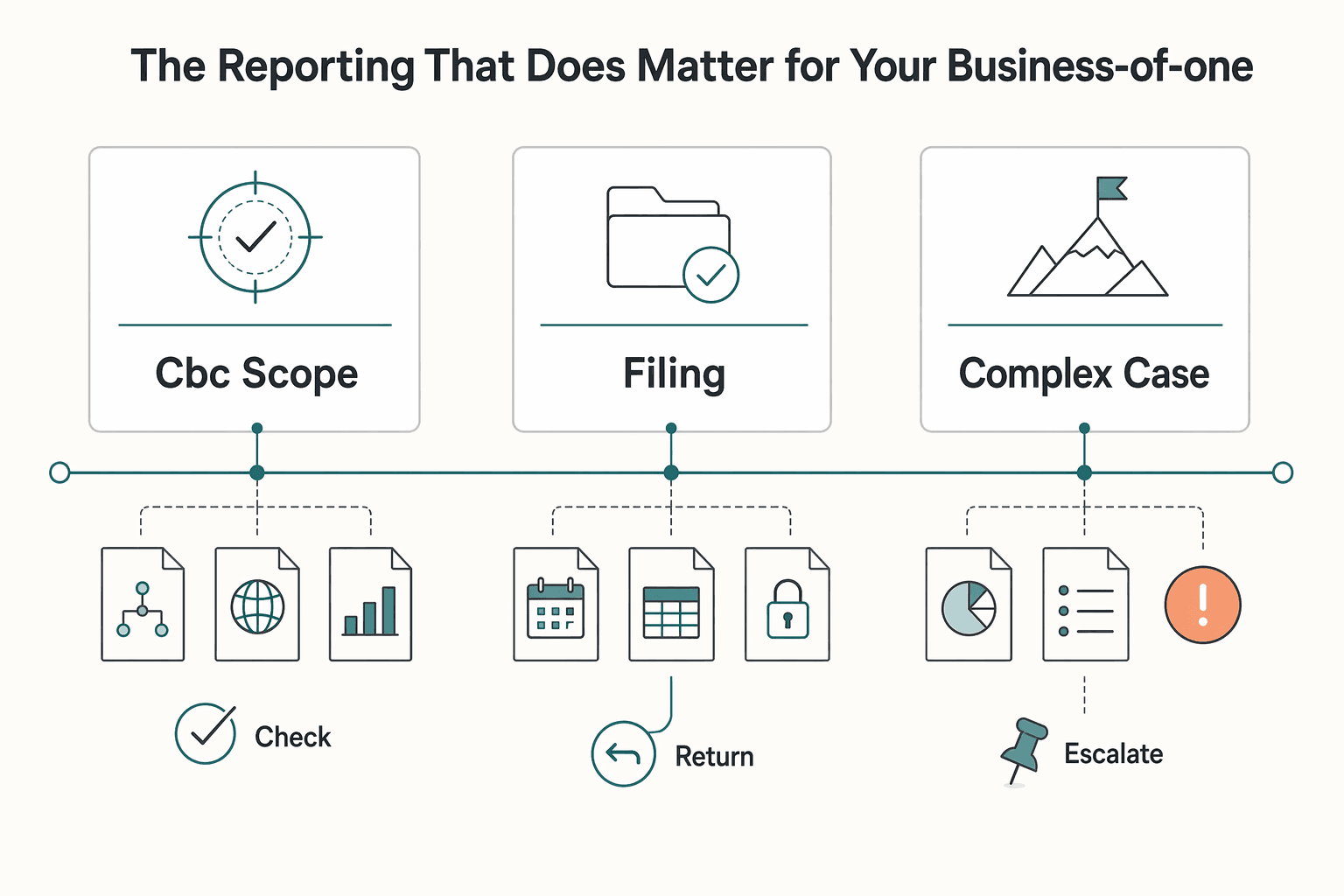

The Reporting That Does Matter for Your Business-of-One#

For a solo operator, first check whether CbC is in scope at all. It is designed for large multinational groups, with filing and exchange mechanics such as Form 8975 and competent authority arrangements. If your setup does not resemble a large-group reporting package, make CbC a scope check first and focus on the filings that apply to your situation.

| Focus | Why it matters | What to do now |

|---|---|---|

| CbC scope confirmation | OECD CbC guidance is aimed at large MNE groups, so scope is the first decision point. | Confirm whether your structure is in scope in your filing jurisdiction and tax year before investing effort in CbC workflows. |

| Filing mechanics (if in scope) | IRS guidance includes practical checkpoints for Form 8975 timing, filing method, and XML schema requirements. | Verify timing, submission method, and required technical format before preparing a filing. |

| Exchange and preparation complexity | CbC operations can involve automatic exchange arrangements and multiple sharing paths, and OECD guidance notes common preparation errors by MNE groups. | Map your reporting path early and run a pre-submission error check so data handoffs stay consistent. |

If you do need to check CbC scope, verify the threshold by jurisdiction and filing year before relying on any number. Do not assume one number applies everywhere. Use this working checklist:

- CbC scope confirmation: Confirm whether your structure is in scope in your filing jurisdiction and tax year before you invest time in CbC workflows.

- Filing mechanics (if in scope): Verify timing, submission method, and required technical format before you prepare a filing.

- Exchange and preparation complexity: Map your reporting path early and run a pre-submission error check so data handoffs stay consistent.

That is the practical shift. CbC is a large-group regime. For a business-of-one, compliance work is usually about clean execution and record discipline in the filings that actually apply to you. The next section turns that into a workable way to track, review, and escalate issues.

Related: A Guide to Transfer Pricing for Small International Businesses.

The Global Professional's 3-Tier Compliance Shield#

Use this as a simple triage rule: where you are, what you own, how you earn. If a new move, account, or client setup does not change one of those three, it is usually not your first-priority risk.

Tier 1#

Risk trigger. Residency risk starts when your movement pattern can be read in more than one way across countries. Tests are not uniform. Some are calendar-year based, some are tax-year based, and some use single-year or multi-year formulas. For example, the U.S. substantial presence framework uses the current calendar year plus a 3-year formula. The UK uses the Statutory Residence Test for a tax year. If two countries can both claim residence, treaty tie-breaker logic can turn on where your personal and economic relations are closer and, if needed, habitual abode.

Keep. Keep one defensible day log with entry and exit dates, overnight location, purpose of stay, and matching support such as travel records, accommodation evidence, calendar entries, invoices, and work-location notes. Consistency across records matters more than perfect formatting.

Do this week. Clean one residency file for the current and prior year. If you spend material time in more than one country, add a "dual-residence evidence" tab for home base, family location, banking center, and where work is managed.

Tier 2#

Risk trigger. Foreign account reporting risk begins when you hold foreign financial accounts or specified foreign financial assets. In the U.S. context, FBAR (FinCEN Form 114) is triggered when aggregate foreign account value exceeds $10,000 at any point in the calendar year. It has an annual April 15 due date and automatic extension language to October 15. FATCA/Form 8938 is separate and can apply alongside FBAR; for certain U.S. taxpayers, reporting starts at $50,000, with higher thresholds for joint filers and taxpayers who reside abroad. Outside U.S.-specific filing, CRS increases visibility through annual cross-jurisdiction account-data exchange.

| Item | Trigger or role | Timing or note |

|---|---|---|

| FBAR (FinCEN Form 114) | Aggregate foreign account value exceeds $10,000 at any point in the calendar year | Annual April 15 due date with automatic extension language to October 15. |

| FATCA/Form 8938 | For certain U.S. taxpayers, reporting starts at $50,000 | Separate and can apply alongside FBAR; higher thresholds for joint filers and taxpayers who reside abroad. |

| CRS | Annual cross-jurisdiction account-data exchange | Increases visibility through annual cross-jurisdiction account-data exchange; do not assume bank reporting or CRS replaces your own filing duties. |

Keep. Maintain one account register with institution, country, owner, authority type, open and close dates, statement location, and highest approximate annual value in your reporting currency.

Do this week. Reconcile every non-domestic account into that register, then set a quarterly value review and pre-filing check. Do not assume bank reporting or CRS replaces your own filing duties.

Tier 3#

Risk trigger. Cross-border income risk usually splits into two tracks: invoicing compliance and permanent-establishment exposure. Good invoicing discipline supports payment and reporting consistency. PE is a treaty concept tied to a fixed place of business and is not solved by invoice format alone.

Keep. For each client, keep a compact file with the signed contract, SOW or onboarding details for the paying legal entity, invoices, payment proof, and work-location notes. Resolve any mismatch between the contracting entity, invoiced entity, and payer before you issue the next invoice.

| Area | Risk trigger | Likely consequence | Preventive control | Escalate when |

|---|---|---|---|---|

| Invoicing compliance | Contract entity, invoice addressee, and payer do not match | Payment delays, rework, inconsistent records | Verify legal entity details and tax identifiers before the first invoice | Client asks you to bill a different entity midstream |

| Tax treatment execution | Unclear place of taxation or missing invoice support | Incorrect treatment and amendment risk | Keep service scope, location notes, and client tax profile with invoice records | You cannot explain why the chosen treatment is correct |

| Permanent establishment | Work starts looking like a fixed business base in one country | Local business tax and registration questions | Track where work is performed and review setup changes early | You are operating from a stable base abroad |

Do this week. Audit your last three international invoices against contract files and travel or work-location records. If you cannot show who hired you, who paid you, and where the work was done, fix that before the next invoice.

Before the FAQ and closing section, run this handoff checklist:

- Which country or countries could plausibly treat you as resident this year?

- Is your foreign-account register complete, with FBAR and Form 8938 reviewed separately where relevant?

- For each active client, can you produce one file with the contract, invoice trail, payment proof, and work-location notes?

- Which one issue needs tax-professional input before your next filing or billing date?

Work through those questions one by one. That is how you replace compliance anxiety with control, one risk, one file, and one decision at a time.

You might also find this useful: How to Use a 'Cost-Plus' Model for Transfer Pricing.

Turn this framework into a repeatable weekly workflow by logging your travel days and residency evidence in the Tax Residency Tracker.

From Compliance Anxiety to Confident Control#

If you are not operating inside a multinational group near CbC thresholds (for example, EUR 750 million or U.S. $850 million parent-entity rules), country-by-country reporting is usually not your day-to-day focus. Your real compliance system is simpler: track where you are, what accounts you hold, and how your income is documented.

Turn the shield into three working files#

Run the 3-tier shield as three files you actively maintain.

Your movement file supports residency decisions. Track dates, locations, and supporting records in one place, and make sure your log and documents tell one consistent story. If U.S. tax residency is relevant, review the Substantial Presence Test thresholds of 31 days in the current year and 183 days across the 3-year formula. Escalate when more than one country could reasonably claim taxing rights.

Your account file supports foreign-account reporting. Keep a ledger with the bank name, country, account owner, maximum balance, and year-end balance, plus statements. If you are a U.S. person, compare aggregate foreign account value against the $10,000 FBAR trigger for FinCEN Form 114, due April 15 with an automatic extension to October 15. If you are not a U.S. person, verify the applicable local threshold before treating it as a filing trigger. Escalate when ownership or control is unclear, or balances cross reporting thresholds.

Your client file supports income and invoice positions. Store contracts, invoices, receipts, deposit records, and tax documents together. Confirm that the contract party, invoice addressee, payer, and booked income stay aligned for each engagement. In the EU, invoices are generally required for most B2B supplies, so missing or inconsistent invoice support is a clear risk signal.

| Worry Pattern | Control Action | Proof You Keep |

|---|---|---|

| "I may have created residency risk without noticing." | Maintain a day log and review it monthly against the rules that apply to you. | Day log |

| "I have foreign accounts but no trigger view." | Keep an account ledger and compare it against your verified filing threshold. | Account ledger |

| "My client income trail is messy." | Reconcile contract, invoice, payment, and tax records for each engagement. | Invoice and tax docs |

Escalate before complexity compounds#

Talk to a pro when any of these show up:

- your residency facts plausibly support tax claims in more than one country

- your foreign account or foreign income profile now requires threshold analysis, not assumptions

- you add an entity, operate through multiple entities, or your client, payer, and invoice structure stops matching cleanly

That is the point of this system: less noise, tighter records, and earlier escalation when the facts change.

For a step-by-step walkthrough, see Can I Claim the Foreign Tax Credit for Taxes Paid to a 'Blacklisted' Country?.

If your cross-border setup still feels unclear after this guide, request a practical next-step review through Contact Gruv.

Frequently Asked Questions

Does country-by-country reporting apply to your business-of-one?

CbCR rules are aimed at multinational enterprise groups with consolidated revenue above EUR 750 million, with annual filing typically in the headquarter jurisdiction. If you operate through multiple entities or inside a larger consolidating group, get a professional scope check before assuming CbCR is out of scope.

How is CbCR different from the filings that matter to you personally?

CbCR is a group-level corporate transparency framework. Personal residency, account, and individual income filing rules are jurisdiction-specific. Use this quick split to decide which lane you are in: | Item | Scope | Filing owner | Trigger condition | Consequence of miss | Your action | |---|---|---|---|---|---| | CbCR | Large multinational groups | Parent or other in-scope group filer | Consolidated group revenue above EUR 750 million | Group-level compliance follow-up by tax authorities | Usually not relevant unless you are in a consolidating group. If yes, verify local mechanics and whether Form 8975 applies | | Foreign-account reporting | Confirm with the relevant authority | Confirm with the relevant authority | Jurisdiction-specific | Jurisdiction-specific | Confirm the exact local rule before relying on any threshold | | Residency and income filings | Confirm with the relevant authority | Confirm with the relevant authority | Jurisdiction-specific | Jurisdiction-specific | Treat these as local-law questions and get country-specific advice |

What should you track while moving between countries?

Track your movement facts and keep supporting records that match your filings. A practical minimum is dates, locations, and the documents that back your timeline. If your records do not tell one consistent story, fix that before filing season.

If banks or tax authorities already exchange data, can you relax your own filing process?

No. CbC reports are exchanged between governments under competent authority arrangements, and that process is for authority use. Treat data exchange as visibility for regulators, not a substitute for your own filing and recordkeeping controls.

What actually gets filed when a group is in scope for CbCR?

CbCR includes jurisdiction-level aggregate tax and activity information for places where the group operates. In U.S. mechanics, Form 8975 and related Schedule A questions are concrete filing checkpoints. If those terms appear in your real workflow, move from DIY to specialist support.

Is CbCR public?

Not at taxpayer level. OECD guidance states reports are submitted to governments and are not publicly available due to confidentiality. Jurisdictions may publish anonymized, aggregated statistics, but that is not the same as publishing a taxpayer’s filing.

What if you suspect exchanged CbC information was disclosed or used improperly?

Treat it as a real escalation path, not a theoretical issue. IRS guidance includes reporting routes for suspected unauthorized disclosure or misuse of exchanged information. Preserve notices, correspondence, and filing context, then escalate with professional support.

When does cross-border client work create extra tax risk for you?

Trigger rules for when cross-border client work creates extra tax risk are jurisdiction-specific. Treat that as a jurisdiction-specific issue and escalate for local advice before relying on assumptions.

When should you stop DIY-ing and talk to a pro?

Do it when your setup spans multiple jurisdictions or entities, or when CbCR markers like EUR 750 million, Form 8975, Schedule A, or competent authority exchanges show up in your real facts. Keep your movement file, account file, and client file current. Review them whenever a new move, account, or client setup changes your fact pattern.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalregister.gov/documents/2024/10/29/2024-24582/provisions-p...trusted

- irs.gov/businesses/international-businesses/frequent...trusted

- irs.gov/businesses/international-businesses/us-multi...trusted

- oecd.org/content/dam/oecd/en/topics/policy-sub-issues...trusted

- oecd.org/content/dam/oecd/en/topics/policy-sub-issues...trusted

- state.gov/wp-content/uploads/2019/03/97-1219-Switzerla...trusted

- state.gov/wp-content/uploads/2019/02/10-1123-Malta-Tax...trusted

- uscc.gov/sites/default/files/2025-11/2025_Annual_Repo...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Transfer Pricing for Small International Businesses with Related Entities

For a business of one operating across related entities, transfer pricing is mostly about execution. Document each related-party charge when it happens, choose the most reliable method you can actually support, and have the file ready before you file your return. If you wait until year-end, the evidence can be harder to rebuild and your method support can be easier to challenge.

How to Use a 'Cost-Plus' Model for Transfer Pricing

Before you use this playbook, note the evidence limit for this section: the grounding available here does not establish technical rules for cost-base construction, arm’s-length legal tests, comparables screening, defensible markup ranges, or jurisdiction-specific thresholds. Treat the steps below as an internal execution checklist, and escalate technical transfer-pricing positions to a qualified advisor.