Quick Answer

Start with a documented readiness review before you convert llc to s-corp: confirm owner eligibility, one-class-of-stock alignment, and current federal classification. Then file based on your actual path, using Form 8832 only when classification facts require it and submitting Form 2553 with all required signatures. Keep IRS acceptance records, payroll setup, and bookkeeping controls in scope from day one so the election is supported in practice, not just on paper.

Separate the S Election From the LLC#

Converting an LLC to S-corp status is a tax and operations decision, not a one-form upgrade. If the entity is eligible and you handle the filing sequence correctly, the election can work cleanly. If not, you can end up with an invalid election and corrective work.

This guide is built around one practical outcome: decide go or no-go, file in the right order, and operate correctly after the effective date. Before filing, run these checks:

- Confirm eligibility for S status, including no more than 100 shareholders, eligible shareholder types, and the one class of stock requirement.

- Confirm filing mechanics: the election is made on Form 2553, and it must be signed by all shareholders.

- Confirm your entity-classification path: a qualifying entity that timely files Form 2553 may not need Form 8832, but sequencing can still matter in some fact patterns.

Treat eligibility issues as blocking issues, not cleanup items. An ineligible shareholder at conversion can invalidate the election.

Keep expectations realistic, too. S-corp income is generally taxed to shareholders rather than the corporation, but entity-level tax can still apply in certain built-in gains and passive-income situations. After election, operations can include payroll and employment-tax obligations, including Social Security, Medicare, and income-tax withholding.

Before you file, review the main risk points. For some LLCs, negative tax capital account balances can trigger income recognition at conversion. This guide flags where federal rules are clear and where you should confirm jurisdiction-specific details before moving forward.

Related reading: A Guide to Board Resolutions for a Delaware C-Corp.

What conversion actually means in practice#

In most cases, "convert LLC to S-corp" means a federal tax election, not replacing your company under state LLC law.

| LLC situation | Tax treatment | Form / filing note |

|---|---|---|

| Single-member LLC | Generally treated as a disregarded entity unless it elects otherwise | No election unless it elects otherwise |

| Domestic multi-member LLC | Generally treated as a partnership unless it elects corporation treatment | Corporation treatment is typically elected via Form 8832 |

| S corporation treatment | Elected for federal tax purposes | Form 2553; must be signed by all shareholders |

Your Limited liability company (LLC) remains the same state-created legal entity, but the Internal Revenue Service (IRS) can tax it differently. In practical terms:

- A single-member LLC is generally treated as a disregarded entity unless it elects otherwise.

- A domestic multi-member LLC is generally treated as a partnership unless it elects corporation treatment, typically via Form 8832.

- S corporation treatment is elected on Form 2553, and it must be signed by all shareholders.

The key point is that legal identity and tax status run on separate tracks. Your LLC can remain the same legal entity even after S-corp tax treatment begins, which is why you should review core records and keep entity name and tax classification consistent.

The common mistake is treating a tax election and a legal conversion as the same event. If separate state-law conversion steps apply, handle those as a separate legal process and confirm whether you need them before filing tax elections.

Once you understand that split, the next job is deciding whether your facts support filing at all. After filing, use the IRS acknowledgment as your checkpoint for acceptance and effective timing. If Form 2553 is missing required signatures, it may not be considered timely. Need the full breakdown? Read Calculating Reasonable Salary for an S-Corp Under IRS Rules.

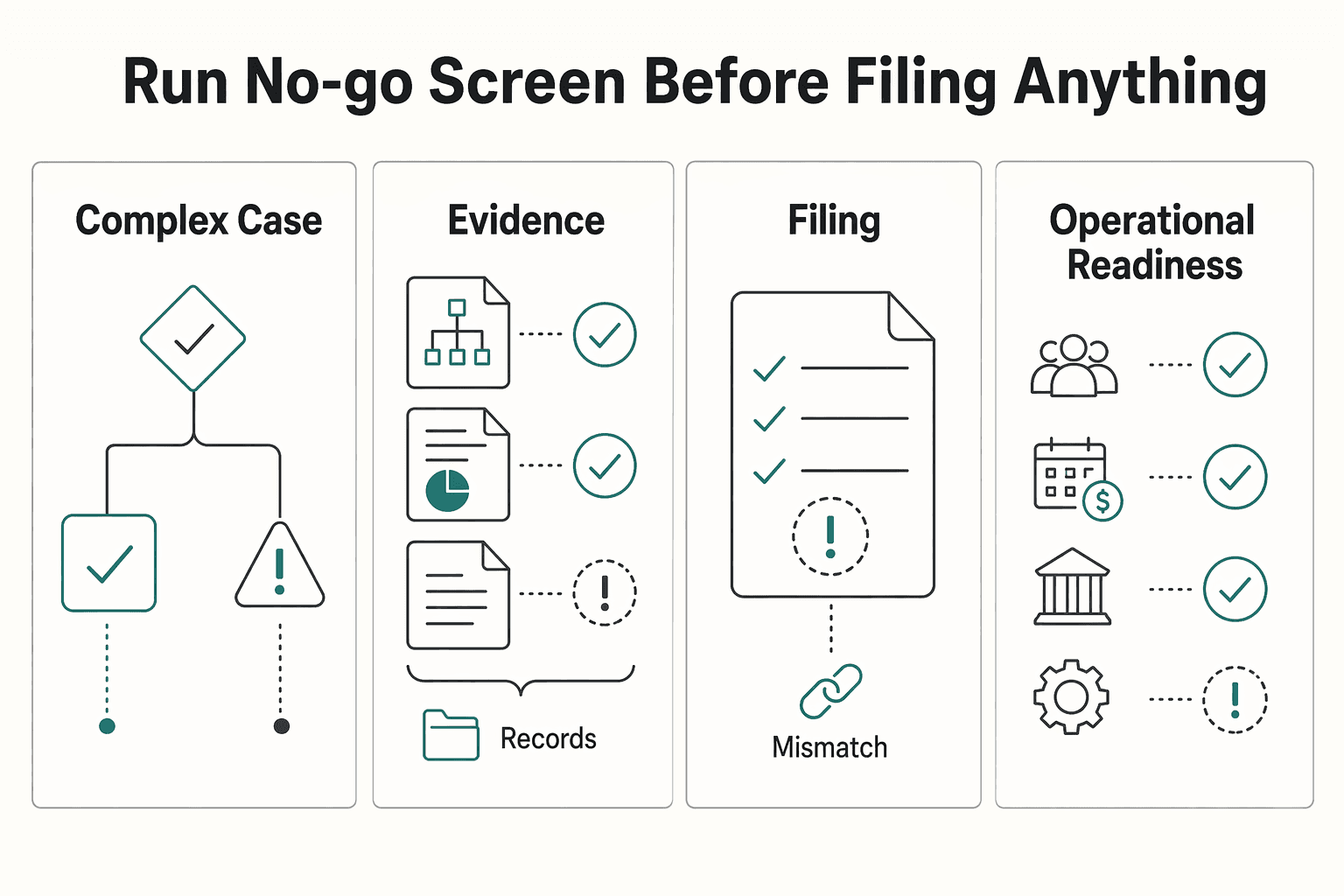

Run the go or no-go screen before filing anything#

Do not file yet. First run a one-page go or no-go screen. If any check is unverified, treat the election as not ready.

Use a decision table you can hand to your accountant, attorney, payroll provider, or co-owner. That way, status, support, and open items sit in one place.

| Check | What you are confirming | What should be in your file | Go or no-go rule |

|---|---|---|---|

| Current tax classification | How the LLC is currently classified for federal tax purposes | Last filed federal return position, any prior Form 8832, internal notes on entity status | If classification is unclear, stop before filing |

| Eligibility assumptions | Which S-corp eligibility assumptions are verified versus still unknown | Current ownership roster, governing documents, and advisor review notes | If any eligibility item is unverified, do not file Form 2553 yet |

| Governing-document review | Whether legal/tax review of governing documents is complete | Operating agreement, amendments, side letters, special allocation terms (if any) | If document review is not complete, treat as not ready |

| Tax posture review | Whether current tax posture needs pre-filing analysis | Prior returns, current books, and any schedules needed for advisor review | If tax posture has not been analyzed, do not assume the election is harmless |

| Operational readiness | Whether execution responsibilities and timing are defined | Provider status, responsibility owner, and first-run timing plan | If execution is not clearly defined, wait |

Start with the classification you have, not the one you want#

This is the first gate because it can change what you file next. The IRS says an eligible entity uses Form 8832 to elect federal tax classification, with options that include corporation, partnership, and an entity disregarded as separate from its owner.

If your records do not clearly show the current federal classification, stop there. If a classification change may be needed before filing Form 2553, confirm the sequence with your advisor first. The IRS Form 8832 page references Form 2553, which is a useful reminder that the forms are connected.

Unverified eligibility items are hard stops, not cleanup items#

If any eligibility item is still an assumption, pause and resolve it first. Do not submit Form 2553 on assumptions.

Keep this document-driven. Your current ownership roster, legal names, percentages, and governing documents should all match. If owner status is uncertain, do not guess. As a general reminder, residency labels can be fact-specific. California's FTB describes residency as facts and circumstances and does not issue written opinions for a specific period.

The quiet risks are usually in the documents and books#

Most preventable problems show up in the agreement or the tax records, not in the form itself. Review governing documents and current tax posture before filing, not after.

For entity terms, gather the operating agreement, amendments, and side arrangements in one place. For tax posture, gather prior returns, current books, and any schedules needed for review.

Operational readiness is an execution test#

Operational readiness is a real go or no-go item, not an afterthought. If the provider, setup, ownership, and first-run timing are not defined, you are not operationally ready.

Use a strict rule: if you cannot produce documentary support for each of the five checks, mark the election not ready rather than "probably fine." Related: Delaware C-Corp vs Wyoming LLC for Your Next Growth Stage. Before you file Form 2553, pressure-test your operational plan, including payments, records, and compliance checkpoints, with the Gruv docs.

Confirm ownership and equity structure eligibility#

This is a hard gate. If ownership or equity terms are unclear, the election is not ready. Start with a current ownership roster and verify it against your governing and tax records.

Test the owners you actually have#

For an LLC electing S-corp status, confirm the company is domestic, has fewer than 100 owners, and has no nonresident alien members. Under Eligible shareholder rules, explicitly confirm that no owner is a corporation or partnership.

Give the Non-resident alien shareholder restriction its own check. If an owner's status is unclear, mark it unverified and resolve it before filing.

Review economics against the one-class rule#

Owner eligibility alone is not enough. Your Operating agreement and related terms need to align with the One class of stock requirement.

This is a common failure point. Unrevised operating-agreement language can inadvertently terminate an S election. Review the current agreement, amendments, and any side arrangements before filing, especially if they create different economic rights across owners. Weigh the tradeoff early, too. The one-class rule can make new investment rounds harder.

Treat unresolved eligibility items as a filing gate#

Handle open eligibility questions before submission, not at the last minute. If owner status, agreement language, or equity terms are still unclear, pause and resolve them first.

Document your eligibility review#

Keep an internal file that captures how you validated eligibility at filing time. Include:

- current ownership roster with legal names and percentages

- notes supporting each owner's eligibility status, including any nonresident alien review

- current Operating agreement, amendments, and the excerpts reviewed for one-class risk

Catch the hidden tax traps competitors gloss over#

The trap to catch early is structural, not cosmetic. If your documents or tax posture are unclear, pause before filing.

Treat unusual tax posture as a stop sign, not a note to revisit#

If your LLC has unusual capital history or other atypical tax facts, do not assume the move to an S corporation election is mechanically clean. The grounding here does not establish one universal tax outcome for those situations, so treat them as review items tied to your actual records.

Before filing, have your advisor test election readiness using current returns, governing documents, and contribution and distribution history. If that explanation is still vague, the election is not ready.

Boilerplate agreements are where S elections quietly fail#

For LLCs electing S status, agreement review is a hard gate. Under the One class of stock requirement, all outstanding equity must grant identical rights to distribution and liquidation proceeds.

A generic operating agreement can still create a prohibited second class of stock, and a filed election does not cure that defect. Review the current operating agreement and all amendments first, then check for any side documents or payout terms that change the economics in practice:

- the current operating agreement and all amendments

- side letters, resolutions, or written distribution arrangements

- liquidation and distribution terms that give different economic rights

- template language copied from multi-class or investor-style LLC docs

If ownership percentages look uniform but distribution or liquidation rights are not identical, treat that as a potential second-class-of-stock issue.

The failure can reach back earlier than expected#

A defective provision can matter earlier than people expect. If an LLC has a prohibited second class of stock, a purported S corporation election is invalid. The problem can trace back to when the offending provision was adopted, including formation-era language in some cases.

If you discover a foot fault later, there may be a repair path. Revenue Procedure 2022-19 (issued in October 2022) provides a mechanism for certain invalidating S-election foot faults without a private letter ruling. That can reduce burden in some cases, but it is not a reason to file first and inspect later.

Build one trap-review file before you submit#

Before you submit anything, keep a single file with the governing documents, amendments, side arrangements, and tax records you used to evaluate election readiness. Add a short written conclusion from your advisor on one-class compliance and shareholder-eligibility posture. If that file is incomplete, treat the election as not ready.

For a step-by-step walkthrough, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Choose the right IRS filing path and sequence#

The right sequence starts with your current IRS tax classification, not your state-law LLC label. Confirm that first, then decide whether you need only Form 2553 or a Form 8832 step before it.

Start with your current IRS classification#

For federal income tax, a single-member LLC is generally in disregarded entity classification unless it elects corporate treatment. A domestic multi-member LLC generally defaults to partnership tax classification unless it files Form 8832 to be treated as a corporation.

Do not guess from memory or state paperwork. Verify your current federal filing posture and any prior classification election on file. If that status is unclear, treat it as an open item and resolve it before preparing the election packet.

Evaluate Form 8832 first, then file Form 2553 when required#

Form 8832 is the entity-classification election to be treated as a corporation. Form 2553 is the S corporation election for an entity eligible to be treated as a corporation.

Use this sequence as a decision rule: evaluate Form 8832 first, then file Form 2553 if your fact pattern requires that order. Do not apply a blanket rule that every LLC must file 8832 before 2553. If timing or status is unclear, pause and verify before filing. Use current final IRS forms and instructions as well. Draft IRS materials are marked "DRAFT, NOT FOR FILING."

Keep submission and acceptance records together#

Treat filing proof as part of the election record. Keep one folder with:

- the signed Form 2553 including signatures from all shareholders

- any Form 8832 used in the classification step

- submission proof, for example, mail or fax confirmation

- the IRS acknowledgment showing acceptance and effective date

If Form 2553 is missing proper signatures, IRS guidance says it is not considered timely. Also confirm the current filing address or fax instructions before sending. The IRS notes an address change for some Form 2553 filers effective June 18, 2019. If you do not receive acceptance or nonacceptance notice, follow up with the IRS at 800-829-4933.

Set up owner pay the way S-corp rules expect#

Once your election is accepted, owner pay should be handled as an operating discipline, not a draw habit. For practical planning, use consistent records and a documented approach to owner-employee pay.

Start with the pre-election baseline#

Start with what you filed before the election, then compare from there. For this self-employment tax context, the IRS includes a disregarded single-member LLC owner in sole proprietor treatment and includes a member of a multi-member LLC taxed as a partnership in partnership treatment. In both cases, Schedule SE (Form 1040) is the concrete record of your pre-election owner-pay tax profile.

Use the baseline as math, not memory. Self-employment tax is 15.3% total, made up of 12.4% Social Security and 2.9% Medicare. You usually must pay it at $400 or more in net self-employment earnings, and generally 92.35% of net earnings is subject to that tax. For 2024, the first $168,600 of combined wages, tips, and net earnings is subject to the Social Security-side combination rule.

Keep the filed Schedule SE, supporting workpapers, and your net-earnings notes. That record matters because Schedule SE information is used to figure Social Security benefits, and this tax can still apply even if you already receive Social Security or Medicare benefits.

Separate wages from distributions on purpose#

For post-election operations, it is usually easier to defend your records when wages and distributions are tracked as separate flows. If they blur together in practice, your records become harder to defend.

A practical owner-pay evidence pack can include:

- a short compensation memo describing role, duties, time spent, and how pay was determined

- payroll records for wage payments

- separate bookkeeping accounts for wages and owner distributions

- distribution approvals or owner records that tie to amounts actually paid

A common risk pattern is irregular owner draws all year, little or no payroll, then relabeling cash later. If you expect to operate that way, do not assume the election alone will produce clean tax savings.

Test whether the change is actually worth it#

The real comparison is pre-election self-employment tax versus a post-election owner-pay process you can document clearly. That is the tradeoff to evaluate.

A practical read is straightforward. If prior filings show meaningful Schedule SE exposure and your records are consistent, the case for changing structure may get stronger. If income is uneven, role valuation is unclear, or bookkeeping will likely blur wages and distributions, the case may be weaker.

Keep the scope tight when modeling. IRS self-employment tax guidance here covers Social Security and Medicare taxes only, not every other tax obligation. When you evaluate the shift to S-corp treatment, use current IRS instructions, anchor on your prior Schedule SE baseline, and choose a pay process you can defend at year end.

Build a first-year compliance rhythm you can sustain#

First-year S-corp compliance is mostly an execution problem: consistent payroll, clean books, and complete records. The risk is rarely one missed task. It is a backlog of weak payroll and bookkeeping that makes your S corporation election harder to support.

A practical approach is to use a recurring review cadence, even though the IRS excerpts here do not require a monthly checklist. A steady cadence works because payroll records, employer tax deposits, bookkeeping close, and filing records need to stay aligned.

Use one recurring checklist#

Keep the checklist short enough to run every cycle:

- Run payroll for any owner-employee and keep the payroll records.

- Confirm employer tax deposits tied to that payroll.

- Close the books with wages and shareholder distributions separated.

- Store records together so quarterly and year-end filings can be reconciled without cleanup work.

Your records should tell one consistent story across payroll, bookkeeping, deposits, quarterly Form 941 filings, year-end W-2/W-3 reconciliation, and Form 1120-S preparation.

A common failure mode is weak payroll and bookkeeping while owner cash is treated as distributions. Weak payroll and bookkeeping can lead to distributions being reclassified as wages, which is why steady first-year controls matter more than theoretical tax savings.

Keep the election file together#

Keep the election file intact from day one. Use one digital or physical file for your filed Form 2553, any Form 8832 you submitted, and the payroll and tax records tied to that election.

This file is your evidence pack if questions come up later. S-corp status is a tax election applied to an existing entity, not a new entity by itself. This documentation is what connects your elected treatment to how the entity actually operates.

Keep payroll and bookkeeping aligned with payouts#

When pay patterns shift, review payroll and bookkeeping before moving cash. The goal is to avoid contradictions between how money moves and how wages versus distributions are reported.

That is the first-year tradeoff in practice: complexity goes up, and the potential benefit depends on whether you can run the process cleanly. If you cannot maintain this rhythm, treat that as a warning sign before you make the election.

Handle state and cross-border caveats without overreacting#

Treat this as three separate compliance tracks: federal entity-tax election, state compliance, and international reporting. A federal election decision does not, by itself, determine whether Form 8938 or FBAR filing is required.

| Track | What it covers | File to keep |

|---|---|---|

| Federal election | Federal entity-tax election | Federal election documents and related acceptance records |

| State | State compliance | Your jurisdiction's entity and tax requirements |

| International | International reporting | FBAR review, Form 8938 review, and your filing or no-filing rationale |

At the state level, requirements vary by jurisdiction. Use state examples as illustrations, then verify your own state filings, tax registrations, and entity-status implications separately.

For cross-border reporting, do a separate review based on your actual foreign accounts and assets. Form 8938 is used to report specified foreign financial assets when they are above the applicable reporting threshold, and it is attached to your annual return by that return's due date, including extensions. A simple checkpoint is to confirm the form states the correct calendar year or tax year.

Key guardrails:

- Filing Form 8938 does not replace FinCEN Form 114 (FBAR) when FBAR is otherwise required.

- Changing entity tax treatment does not, by itself, remove Form 8938 review.

- For certain specified domestic entities, the Form 8938 instructions reference thresholds that exceed $50,000 at year-end or $75,000 at any point during the year.

- Higher Form 8938 thresholds can apply in some cases, including some joint filers and taxpayers residing abroad.

- If you are not required to file an income tax return for the year, Form 8938 is not required for that year.

Keep one file per track:

- Federal election file: your federal election documents and related acceptance records.

- State file: your jurisdiction's entity and tax requirements.

- International file: FBAR review, Form 8938 review, and your filing or no-filing rationale.

For globally mobile owners, document each track separately. That helps you avoid both overreaction and missed filings.

Decide when to convert now and when to wait#

Convert now only if your eligibility and records are already solid in practice. Wait if structure or compliance discipline is still moving. The real question is not just whether you can file Form 2553, but whether you can file and stay compliant after filing.

Convert now when your setup is already audit-ready#

A strong "go" case is usually straightforward. Ownership is stable, owners are eligible shareholders, your Operating agreement does not conflict with the One class of stock requirement, and all shareholders can provide written consent for Form 2553.

Your day-one file should be ready before you elect:

- current ownership roster

- signed shareholder consents

- reviewed Operating agreement

- filed Form 2553 and submission proof

If timing is flexible, January 1st is often the cleanest switch point for bookkeeping. Mid-year changes can require parallel recordkeeping, which increases complexity.

Wait when structure or cleanup is unresolved#

Delay if ownership is changing, agreement terms could create second-class economics, or compliance discipline is not yet reliable. An ineligible shareholder at conversion can invalidate the election, and S status can terminate later if eligibility rules stop being met.

Pause for tax cleanup when needed, too. If the LLC was taxed as a partnership and members have significant negative tax capital account balances, conversion can trigger unexpected taxable income. One cited example shows a negative $100,000 tax capital account leading to $100,000 of recognized taxable income.

If several go or no-go checks are still unresolved, take that as a delay signal. Fix the structure first, then elect.

Compare this path with financing plans#

If your ownership structure may change, do not assume an S election is the default long-term fit. Compare the ownership rules and tax tradeoffs before you commit. A side-by-side review like The S-Corp Election vs. C-Corp: A Tax Comparison for US-Based Agencies can help you pressure-test that choice early.

Use this execution checklist before you press submit#

Before you file, confirm four packets in order: entity baseline, eligibility, filing, and operations. A complete Form 2553 alone may not be enough if these records do not align.

| Packet | What to confirm | Pause if... |

|---|---|---|

| Entity baseline | Current tax classification, owner count, ownership roster, state status | You cannot confirm whether the LLC is in Disregarded entity classification or Partnership tax classification |

| Eligibility | Ownership roster and related entity records used to confirm the election can be made | Any ownership or eligibility question is unresolved |

| Filing | Completed Form 2553, possible Form 8832, submission copy, response-tracking log | You are assuming Form 8832 is or is not required without checking the classification path |

| Operations | Recordkeeping and bookkeeping processes needed to support the election | Your records process is not ready to support the election consistently |

Confirm the baseline before you pick the filing path#

Start with current federal tax classification. If you cannot confirm whether the entity is currently treated as disregarded or partnership, you do not yet have a reliable filing path.

Use Form 8832 as a checkpoint when classification is unclear. The form asks whether the entity has more than one owner, and owner count affects available classification choices. For multi-owner entities, it lists partnership or association taxable as a corporation. It also asks whether a prior election had an effective date within the last 60 months and signals a general ineligibility stop in some cases.

State status is a separate check. Federal election status does not replace state tax treatment. For example, California taxes nonresidents on California-source income.

Treat eligibility as a document test, not a memory test#

Confirm eligibility with records, not assumptions. Your ownership roster and related entity records should describe the same ownership picture before filing. If those documents do not line up, pause and fix the mismatch first.

File like you expect to defend it later#

Assume you may need to prove the sequence later. Keep a complete filing packet: Form 2553, any required Form 8832, what you submitted, and a dated IRS response-tracking log. If status is delayed or unclear, verify directly instead of assuming the election is in effect.

Also verify current submission instructions at filing time. The IRS notes Form 2553 filing-address changes for certain states effective June 18, 2019.

Make sure operations are ready to support the election#

Do not file before operations can support the election. Bookkeeping and recordkeeping should be ready to reflect the election consistently.

Retain election records as ongoing operational records, not one-time paperwork. Keep accepted election documents, submission copies, and bookkeeping records together. We covered related payroll context in What is 'Reasonable Salary' for an S-Corp? A Guide to IRS Compliance.

Conclusion#

If you're weighing whether to convert llc to s-corp, the priority is not speed. It is proving, in your records, that the election is valid before you file.

This is not just an administrative checkbox. Your tax and ownership facts must support the election. A single ineligible shareholder can invalidate it. The one-class-of-stock requirement can get complicated once your operating agreement and state LLC law are involved. If your LLC has significant negative tax capital accounts, conversion may not be worth it because member tax exposure can be substantial. One cited example shows a member with a $100,000 negative tax capital account balance being deemed to have $100,000 of taxable income at conversion.

Use this decision rule: not "Can I file now?" but "Can I support each go or no-go check with records I would hand to the IRS or an advisor?" If not, pause and fix the fact pattern first.

Your file should be boring and complete. At minimum, confirm your ownership roster, shareholder eligibility, one-class-of-stock alignment in governing documents, and required election signatures. If your current federal tax classification is unclear, resolve that first and confirm whether an additional classification election is relevant to your path. Filing is not the same as confirmed treatment. IRS internal guidance includes a scenario where an S-corp filing is processed as a C corporation.

Next step:

- Complete the checklist from records, not memory.

- Flag unknowns tied to jurisdiction, operating agreement terms, or current classification.

- Pause on major stop signs, especially an ineligible owner or meaningful negative tax capital account exposure.

- Confirm unresolved points before filing, then keep one packet with signed filings, submission proof, and IRS response records.

If your LLC clears the eligibility and capital-account checks and your records support the filing, the election can work well. If not, waiting is usually the lower-risk choice.

If you want to confirm your post-election money workflow is audit-ready before you commit, talk with Gruv.

Frequently Asked Questions

Can an LLC elect S-corp taxation without changing its legal entity under state law?

Often, yes. A practitioner source indicates an LLC can elect S-corp tax treatment without changing its state-law entity form. Still, do not treat that as a universal state-law rule.

What are the minimum eligibility checks before filing Form 2553?

Start with IRS eligibility: the entity must meet S-corp requirements, including being a domestic corporation, having no more than 100 shareholders, having only allowable shareholders, and having only one class of stock. It also cannot have a non-resident alien shareholder. Before filing Form 2553, confirm required information in the form instructions and make sure all shareholders sign the form.

When is Form 8832 needed before an S corporation election?

Form 8832 is the federal entity-classification election form. Whether it is needed before Form 2553 depends on the entity’s current federal tax classification. The provided grounding does not establish a universal sequencing rule, so confirm classification first if status is unclear.

What usually invalidates an S-corp election after filing?

Common risk points are unmet IRS eligibility requirements, ineligible shareholders, not meeting the one-class-of-stock requirement, or missing shareholder signatures on Form 2553. Filing alone does not fix an ineligible fact pattern.

How does the one class of stock rule affect an LLC operating agreement?

At minimum, your governing documents should not conflict with the IRS one-class-of-stock requirement for S status. If documents and ownership records are not aligned with that requirement, resolve that before filing.

Why can a negative tax capital account create taxable income during conversion?

The provided grounding does not establish a universal conversion rule for negative tax capital accounts. Do not assume it always creates taxable income, and do not assume it is always neutral. Treat it as a case-specific tax analysis to resolve before filing.

What should a solo professional verify before deciding to switch?

Verify the fundamentals first: current federal tax classification, S-corp eligibility, and complete shareholder signatures for Form 2553. Confirm whether Form 8832 is needed based on your current classification. If any of those items are unresolved, pause and fix them before electing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

The S-Corp Election vs. C-Corp: A Tax Comparison for US-Based Agencies

**Start with this rule: choose the structure you can qualify for, operate cleanly, and defend under review.**

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.