Quick Answer

Start by treating a commission-only sales structure as documented B2B work, not a verbal percentage deal. Put scope and non-revenue deliverables in an SOW, then confirm your sourced accounts are separately identifiable in CRM before you negotiate rate details. Define the earned event, who runs payout calculations, and which report controls disputes. Add post-termination handling for in-flight opportunities, and keep authority limits, invoice records, and data-use responsibilities clear so payment reviews rely on evidence.

Stop Thinking Like a Sales Rep, Start Acting Like a Strategic Partner#

Change your positioning before you discuss rates. If you walk into a startup conversation like a candidate for a job, you may make it easier for the client to control your day-to-day work, blur what you were hired to produce, and create more room for payment disputes when results take time. If you position yourself as a business delivering a defined sales service, you create clearer proof of value and a cleaner basis for getting paid.

That shift can matter in a commission-only sales structure because you are often funding early work with your own time. Your first protection is not a higher percentage. It is a clearer engagement shape.

A useful model comes from independent consulting work. Start with a defined scope, document it, refine it after discovery, and tie reporting back to that scope. In one example, an outside consultant was hired through an RFP, then worked under a three-party contract with a final report tied to 8 scope elements. You do not need that level of formality for an early-stage sales engagement, but the pattern is worth copying.

Position the engagement like a service, not a seat on the team#

Treat the relationship as B2B work from the start. Talk about scope, deliverables, checkpoints, and reporting instead of territory, quota, and a manager. The practical distinction can look like this:

| Area | Employee-style engagement | Partner-style engagement |

|---|---|---|

| Control | Client directs schedule, tools, messaging, and daily activity | Client sets goals and boundaries; you own how you execute |

| Deliverables | Activity expectations and general sales duties | Defined outputs such as pipeline reports, feedback summaries, and sourced opportunities |

| Risk ownership | Enablement and process design are often treated as internal responsibilities | You carry more execution risk, so scope and proof of contribution matter more |

| Payment implications | Payment is often tied to time or role expectations | Payment depends on documented outcomes, attribution, and contract clarity |

If the company wants daily standups, fixed hours, mandatory tool use, and approval on every outreach step, treat that as a signal to clarify expectations early. It may still become a workable deal, but that setup can increase payment friction. Your role may look like internal labor while your upside is still pushed into variable compensation.

Use an SOW and KPI split to keep the work measurable#

Do not overcomplicate this. Put the service in writing. Use a short Statement of Work for what you will do, and keep KPIs as performance signals rather than the whole agreement. A solid early draft should spell out:

| SOW item | What to define |

|---|---|

| Coverage | Scope of accounts, segments, or channels you are covering |

| Other deliverables | What you will deliver besides closed deals |

| Opportunity logging | How sourced opportunities will be logged and reviewed |

| Attribution data | What data the client must provide for attribution and payout review |

| Scope review timing | When the scope will be revisited after an initial discovery period |

That last point matters because early assumptions may be wrong. In that example, the scope was refined into a more detailed work plan after document review and initial interviews. You can use the same move. Start with a narrow first phase, then revise once you have seen the market, product gaps, and sales cycle reality.

Show value before revenue lands#

If you want partner treatment, deliver partner-grade outputs early. Closed revenue can lag. Useful signal does not have to.

| Early output | Evidence trait | Useful later for |

|---|---|---|

| Weekly pipeline insight notes | Observable, date-stamped | Invoices, commission reviews, or disputes later |

| Objection patterns from prospect calls | Observable, date-stamped | Invoices, commission reviews, or disputes later |

| Process feedback on handoff gaps | Observable, date-stamped | Invoices, commission reviews, or disputes later |

| Competitor mentions | Observable, date-stamped | Invoices, commission reviews, or disputes later |

| Market signal reporting on pricing resistance or feature requests | Observable, date-stamped | Invoices, commission reviews, or disputes later |

Those outputs are easy to date-stamp and later attach to invoices, commission reviews, or disputes.

Build one checkpoint into the first month. In the same example, orientation meetings ran for 3 days before the work moved forward. Your version can be simpler, but the lesson holds. Front-load alignment, then document what changed. A kickoff summary, a first pipeline review, and a written scope update create a paper trail that can help protect cash-flow conversations.

Another failure mode in that example is lost attribution inside the client's own reporting. In that case, reporting was limited because the company did not distinguish Niagara Mohawk data within line-of-business reporting. Your version of that problem can be easier to spot: your leads, accounts, or opportunities get mixed into the house pipeline and stop being traceable. Once that happens, commission arguments can follow.

Before you negotiate comp, ask one blunt question: how will my sourced work be separately identified in your CRM and reporting? If there is no clean answer, fix that first. Then move to the next pillar: How to Structure a Commission-Based Independent Contractor Agreement.

Related: How to Create a Sales Playbook for Your SaaS Team. If you want a quick next step, try the free invoice generator.

Pillar 1: Architecting Your Compensation#

Choose the model your client can report cleanly and you can enforce consistently. In this setup, compensation design affects cash-flow stability, behavior, and payout disputes, not just upside.

A sales compensation plan is the written blueprint for what gets rewarded and when. Treat it as a risk-control document. Before you agree to any model, confirm the startup can reliably show your sourced accounts, deal value, discounts, and closed status in CRM without manual reconstruction.

| Model | Plain definition | Use it when | Cash-flow stability | Incentive alignment | Admin complexity | Downside risk to you | First term to lock |

|---|---|---|---|---|---|---|---|

| Revenue share | You are paid on attributed revenue | You can influence top-line outcomes directly, deal cycles are shorter, and pricing is relatively consistent | Low | Strong for revenue growth | Low to medium | High if attribution or timing is disputed | Exact commission trigger logic |

| Gross margin | You are paid based on deal profitability, not just revenue | Profit protection matters, discounting varies, or delivery cost swings by deal | Low | Strong for profitable growth | Medium to high | High if margin inputs are unclear | Which margin data is authoritative for payout |

| Retainer plus performance | Fixed retainer plus variable performance pay | Deal cycles are long, the offer is still maturing, or your work includes strategy and pipeline build | Medium to high | Balanced between early work and outcomes | Medium | Lower than pure variable structures | What the retainer covers in scope |

| Draw against commission | Advance paid now and offset against future commissions | You need near-term cash support and trust pipeline quality and reporting discipline | Medium | Can align if targets and reporting are credible | Medium | Can be severe if draw terms are vague | Whether the draw is recoverable |

If the startup wants to reward more than one goal, it may propose a matrix-rate structure (rate changes by achievement plus another filter). That can work, but only when it can calculate metric intersections cleanly; otherwise payout review turns into math disputes.

Use this quick fit check:

| Startup condition | Best-fit starting model |

|---|---|

| Short deal cycle, stable pricing, strong reporting quality | Revenue share |

| Long deal cycle, lower product maturity, heavy discovery work | Retainer plus performance |

| Lower pricing control, frequent discounting, margin-sensitive business | Gross margin |

| Strong reporting quality, immediate cash-flow pressure for you | Draw against commission |

Before work starts, lock these items in the compensation schedule and contract:

- Scope baseline tied to your SOW

- Commission trigger logic (the status or event that counts)

- Treatment of discounts, refunds, and reversals

- Draw recoverability status, if a draw applies

- Documentation required for payout review (CRM fields, report exports, invoice backup)

In practice, the safest plan is usually the simplest one the startup can report accurately. For a step-by-step walkthrough, see A Guide to Sales Tax Nexus for Remote Businesses.

Pillar 2: Fortifying Your Contract#

After you set compensation, lock the deal in writing with the same precision. Your contract is the system for scope, commission entitlement, and enforcement when the client process breaks.

This is payment protection, not legal theater. One contract-review source attributes 67% of B2B legal disputes to unclear wording or overlooked clauses. Use a structured review approach: define the event, define the evidence, define the exit, and define what you are not agreeing to absorb.

The five clauses that actually protect your pay#

- Define when commission is earned.

State the exact earned event in plain language and tie it to a verifiable record. Also state how reversals, credits, cancellations, or non-payment affect amounts already earned, so that rule is not invented later.

- Define payout mechanics separately.

The earned event and payout process are different. Name who calculates payout, which report controls the math, what review path applies, and what happens when records conflict.

- Define termination and tail handling.

Say which documented in-flight opportunities remain commissionable after termination and how post-termination review works after legal verification in the relevant jurisdiction. This is what protects pipeline value when timing and exit do not align.

- Define liability-cap logic for your actual role.

Set the cap structure with legal review and make clear your responsibility tracks your contracted services. Do not leave room to shift broad downstream business losses onto you by default wording.

- Define IP and data-use boundaries.

Separate ownership of your pre-existing materials from client-use rights, and limit client-data use to the agreed service purpose and instructions. This avoids ownership creep and data-related blame shifting.

How the clauses compare#

| Clause | Primary risk covered | Common ambiguity to eliminate | Minimum wording intent |

|---|---|---|---|

| Commission earned | Nonpayment for sourced deals | "Closed" or "won" not defined | Name the verified earned event and the system or document that records it. |

| Payout mechanics | Delayed or disputed payout | Review/approval path unstated | Name the payout report, reviewer role, and verified trigger for payment. |

| Termination and tail | Loss of pipeline value after exit | No rule for in-flight deals | Define the documented pre-termination status that keeps a deal eligible and the verified post-termination rule. |

| Liability cap | Disproportionate financial exposure | Broad indemnity or uncapped damages | Set cap logic after legal review and list only verified carve-outs. |

| IP and data use | Ownership and misuse disputes | Pre-existing materials and client data blurred together | Limit client data use to the documented service purpose and agreed instructions. |

What to review before you sign#

Before you sign, run a short, structured check. A 15-point checklist model is useful because it groups risk/liability, protection of sensitive assets, and termination/conflict controls instead of treating them as fine print.

| Review point | What to check |

|---|---|

| SOW vs. compensation | The SOW matches the compensation schedule line by line, including exclusions |

| Earned-commission proof | You can point to the exact record that proves commission was earned |

| Payout calculation path | There is a named report, owner, and review path for payout calculations |

| Post-termination commissions | They are tied to documented status, not verbal assurances |

| Liability wording | Jurisdiction-sensitive limits and carve-outs are identified for legal review instead of filled in from memory |

| IP and data terms | They match what you deliver and what data you actually handle |

| Vague words | If wording says "reasonable," "material," or "promptly," replace it with measurable language |

If a payment clause does not map to a real record, a real owner, and a real dispute-prevention purpose, it is not ready to sign.

For a related pricing workflow, see How to Calculate Your Billable Rate as a Freelancer.

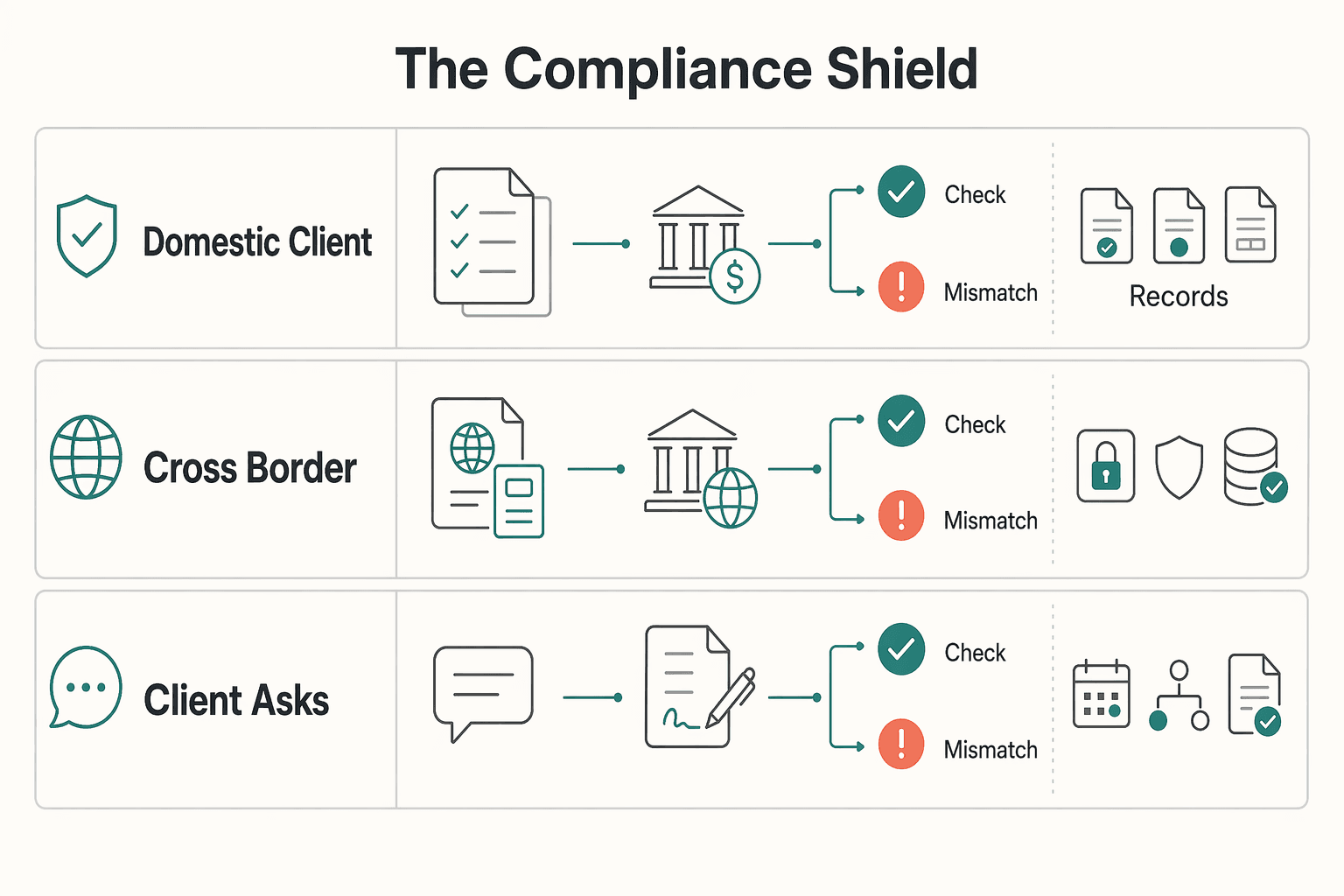

Pillar 3: The Compliance Shield#

Good contract language helps, but your operating habits are what keep payment moving. Here, the compliance target is simple: do not create tax, invoicing, or privacy issues that can delay or block payout.

For PE risk, keep your authority narrow on paper and in practice. State clearly that you do not have authority to sign or conclude contracts for the client, then work the same way in emails, proposals, and calls. Keep a record of who at the startup approved pricing, approved terms, and executed the final agreement. If your behavior suggests decision authority you do not have, risk rises even if the contract wording is clean.

| Scenario | What you must confirm before invoicing | What to include on the invoice | What to document for audit trail |

|---|---|---|---|

| Domestic client | Your registration, filing, tax-treatment, and threshold questions that still need verification | Legal names, service period, contract/SOW reference, amount due | SOW copy, payout report, procedure/policy version used, last update date |

| Cross-border B2B client | Client tax status/ID, whether reverse-charge or withholding treatment applies, and any local threshold or filing questions still needing verification | Contract reference, verified tax-treatment note, invoice currency | Client tax details received, approvals, advice relied on, final invoice copy |

| Client asks to split work or invoices | Whether the structure would sidestep a threshold, approval step, or filing rule that still needs verification | Only the real commercial scope and actual service period | Written scope rationale, approval notes, records showing invoice format matches reality |

Privacy needs the same execution discipline:

- Map what personal data you access, where it comes from, where it goes, and why you need it.

- Assign roles for this engagement: who sets purpose/means, and whether you act only on the client's instructions.

- Set minimum controls for access control, risk assessment, governance, and data-loss prevention.

- Define a breach-response workflow: detect, contain, notify the client through the agreed path, then run a post-incident review.

- Put a DPA in place when applicable rules or the client's policy require it for the role and data flow you confirmed.

Before kickoff, run this compliance check:

- Confirm governing laws, rules, and client policies for this engagement.

- Confirm tax registration, filing, and threshold questions that still need verification.

- Confirm authority boundaries and who approves final terms and payouts.

- Confirm your data map, role assignment, and whether a DPA is required.

- Record your procedure note with current version/date and an update cadence.

You might also find this useful: A Guide to Credit Insurance for B2B Sales.

You Are the Architect of Your Success#

Treat this as system design, not upside chasing. In this kind of arrangement, your job is to decide upfront how cash-flow reliability, contract control, and compliance discipline will be handled before deals get messy.

Use the same three pillars as your execution routine for the next cycle. For compensation, confirm where credit, approvals, and payout handling are written. For contract control, keep one current agreement and one current comp version so your working terms stay clear. For compliance ownership, keep your own record trail from day one so you can quickly resolve mismatches.

| Area | Reactive commission-only behavior | Architected operator behavior |

|---|---|---|

| Compensation design | Focuses on upside first | Confirms how credit, approvals, and payment records are handled |

| Contract terms | Starts from verbal alignment | Works from written terms with clean version control |

| Compliance ownership | Assumes records will be handled elsewhere | Maintains a complete, organized record trail |

If the day-to-day work no longer matches the paperwork, pause and realign before pushing more deals forward.

For your next engagement cycle:

- Confirm signed terms match how you will actually work

- Set a recurring review for approvals, attribution, and unpaid amounts

- Store each commission-related change in one clear location

- Tighten loose terms before the next deal using How to Structure a Commission-Based Independent Contractor Agreement

For adjacent planning, revisit How to Set Sales Quotas for a SaaS Team. If you need program-specific payments guidance, Talk to Gruv.

Frequently Asked Questions

Is a commission-only sales structure legal?

It can be, but the answer depends on your jurisdiction and whether you are actually being treated as an independent contractor or as an employee. Commission employees and independent contractors are different categories, and state rules may be stricter than the federal baseline, including wage rules that apply to most workers. If the day-to-day arrangement looks more like employee oversight than contractor autonomy, treat that as a classification warning and check whether the contract matches how you will work day to day.

What is a good commission rate for a consultant or 1099 sales rep?

There is no supported standard rate you can safely copy, so do not anchor on internet averages. Set your price by the sales cycle, how clearly revenue can be attributed to you, and how long cash may sit between “Booked,” “Earned,” and actual payout. If those checkpoints are vague, any percentage can look good on paper and still pay badly in practice.

Should you choose pure commission, a retainer plus upside, or an employee plan?

Choose based on cash-flow risk and control, not just upside. If deals can take months, or more than a year after booking to fully complete, pure commission pushes timing risk onto you unless the payment rule is very tight. Use this quick comparison, then mirror the choice in both the contract and the comp plan. | Model | Cash-flow predictability for you | Who usually carries more timing risk | Easier to justify when | |---|---|---|---| | Commission-only contractor | Low unless payout timing is fixed in writing | You | Attribution is clear and the sales cycle is short enough to fund yourself | | Retainer plus performance component | Medium | Shared | You are doing strategy, market development, or a long-cycle sales effort | | Employee commission plan | Varies by jurisdiction and wage plan | More employer responsibility applies | The company wants tighter control, policy compliance, and employee-style supervision |

How do you negotiate a draw against commission?

If a draw is offered, get the terms in writing, including the amount, payment timing, and how it connects to commission payouts. Verbal reassurance is not enough, especially where commission payment can be delayed until the company collects from its customer. Ask for the draw language in the same document that defines commission triggers and payout timing.

What are the biggest red flags in a commission-only offer?

The first red flag is uncertainty. If you cannot look at a calendar and know the expected commission payment date, or the plan does not define “Booked” and “Earned,” expect dispute risk. The second is employee-style control layered onto contractor terms, which can create classification and compliance risk.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/daffars/mp5315-contracting-negotiationtrusted

- comptroller.texas.gov/purchasing/docs/96-1809-4.0.pdftrusted

- dgs.ca.gov/-/media/Divisions/PD/PTCS/PAU/FISCAL-Financi...trusted

- documents.dgs.ca.gov/dgs/fmc/gs/pd/GSPD13-005.pdftrusted

- documents.dps.ny.gov/public/Common/ViewDoc.aspxtrusted

- eeoc.gov/best-practices-private-sector-employerstrusted

- farmingdale.edu/courses/index.shtmltrusted

- gsa.gov/system/files/MULTIPLE%20AWARD%20SCHEDULE%20%...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

How to Structure a Commission-Based Independent Contractor Agreement

Commission agreements usually fail when key terms stay ambiguous. In practice, disputes start when the contract blurs contractor classification, leaves payout timing unclear, or leaves room for competing interpretations.

How to Create a Sales Playbook for Your SaaS Team

A sales playbook can help you avoid the wrong deal, not just win the right one. Treat each opportunity as a business risk decision first and a sales opportunity second. If you take on a prospect who is wrong for your offer, the impact often shows up later: unclear expectations, slower payment, rushed delivery, and product decisions shaped by the wrong customer.