Quick Answer

Start with a clear order for choosing a 401k investment: set your salary deferral, confirm employer match and vesting terms in plan documents, then choose either one target-date fund or a self-managed stock-and-bond mix. If you want lower maintenance, the one-fund route is usually cleaner. If you want control, assign each fund a specific role and maintain it. Before submitting elections, verify loan and withdrawal features because they depend on your plan.

Start here if you want to choose your 401(k) in one sitting#

Treat this as a cash flow and behavior decision first, and a fund-picking exercise second. The goal is to help you make a workable choice from a real plan menu without guessing, chasing what is hot, or changing course every time markets move.

A 401(k) is the account wrapper. In this setup, employees choose how much salary to defer, meaning you delay receiving part of that pay now so it goes into the plan instead. That distinction matters because it is easy to spend all your time comparing funds and almost none deciding whether your contribution level actually fits your income.

If you are a freelancer, creator, or small-team operator, start with risk you can live with when revenue is uneven. Your investment choice should not force you into reversing course the first time invoices are late or a client churns. A useful rule is simple: pick a contribution rate and investment approach you can keep during a slow quarter, not just during a strong month. An early mistake is building an aggressive allocation when your real constraint is unstable cash flow, then cutting contributions or pulling back at the worst time.

The decisions you control right now are narrower than they seem:

- Your salary deferral level. Set this deliberately instead of treating it as an afterthought. Employee salary deferrals are always 100% vested, so that money is fully yours in the plan.

- Whether you are capturing any employer match available. Do not assume every plan offers one, and do not assume all employer contributions are immediately yours. Employer contributions may vest on a graduated vesting schedule, so check the vesting language in your plan documents before you count matched dollars as portable.

- How simple or hands-on your fund setup should be. You do not need a clever allocation on day one. You need one you can explain and stick with.

Before you click submit, do one verification pass in the actual plan documents or enrollment materials. Confirm three things in writing: your match formula if there is one, the vesting schedule on employer contributions, and any plan features you may be tempted to use later, such as participant loans or in-service withdrawals. Loans can be permitted in a 401(k), but access and terms depend on the plan. In-service withdrawals can trigger a possible 10% additional tax if you are under age 59-1/2.

One more operator note if you run a business and are setting up or overseeing the plan side. A 401(k) can be used by a business of any size. In this IRS setup context, annual filing of Form 5500 is required. Also, governing rules differ across pension systems, and state and local plans are generally governed by state laws. For a cross-border example, see Tax Implications for an Australian Resident Owning a US LLC.

Know the building blocks before you pick funds#

Start with one distinction: your 401(k) plan is the account wrapper, and the funds are the investments inside it.

| Option label | What it is | Planning note |

|---|---|---|

| Target-date fund | Bundled, hands-off option that adjusts over time | Designed for set-and-forget use; a starting point if you want less ongoing maintenance |

| Mutual fund / ETF | Investment vehicle that can hold many securities | If you combine several, you usually need to choose and maintain your own mix |

| Stock fund | Growth-oriented exposure | Plan menus may label segments such as large-cap, mid-cap, small-cap, or international stock |

| Bond fund | Invests in bonds | Typically plays a stabilizing role relative to stock-heavy choices |

Your choices usually come from a fixed menu set by the employer and plan provider, often 10 or more options, but the lineup varies by plan. Many plans keep you in funds, while some may allow individual stocks, bonds, or ETFs, so confirm the actual menu in your enrollment screen or fund lineup document before comparing options.

Use the labels as a job description for each option:

- Target-date fund: a bundled, hands-off option designed for set-and-forget use that adjusts over time.

- Mutual fund / ETF: investment vehicles that can hold many securities; if you combine several, you usually need to choose and maintain your own mix.

- Stock fund: growth-oriented exposure (for example, a large-cap fund focused on very large U.S. companies; your menu may also label other stock segments such as mid-cap, small-cap, or international stock).

- Bond fund: invests in bonds and typically plays a stabilizing role relative to stock-heavy choices.

If you want less ongoing maintenance, start with a target-date option. If you build your own mix, check each fund's role first so you do not accidentally stack multiple stock funds and end up with more stock exposure than you intended.

Use a 30-minute decision sequence instead of browsing funds randomly#

Use this order: choose how you will run the account, set contribution behavior, pressure-test the choice, then review on a schedule.

Pick your operating mode now#

Choose one mode and keep it clean.

- One-fund mode: use a single target-date fund if you want fewer moving parts.

- Self-managed mode: use a stock-fund and bond-fund mix only if you are willing to maintain that mix over time.

Avoid mixing modes without a clear reason, because it can leave you with more stock exposure than you intended.

Set contributions before fund fine tuning#

Set contributions before comparing similar funds. Contribution discipline comes first: do not skip retirement-account contributions, and do not pull money out of retirement accounts, to chase other investments. Retirement-account contributions are presented as beneficial for tax, estate planning, and asset protection reasons.

If your plan includes matching terms, verify those terms in your own plan documents or enrollment flow before you finalize elections.

Apply one commitment test and set one review rhythm#

Before you submit, make sure you can explain your allocation in one sentence and still follow it during market swings. If you cannot explain it simply, simplify it.

Then set one recurring review cadence and avoid ad hoc changes between reviews. Change course only when something material has changed, such as your job, income stability, or risk tolerance.

Compare the two paths and pick one on purpose#

Pick based on maintenance reality, not fund-browsing momentum: if you want fewer moving parts, use a target-date fund; if you want control and will maintain the allocation, use a self-built mix.

| Path | Simplicity | Control | Maintenance burden | Common failure modes |

|---|---|---|---|---|

| Target-date fund | High. One fund handles a bundled mix that adjusts over time. | Lower. You accept the manager's mix and glide path. | Low. Mostly contributions plus periodic review. | Choosing by year label alone, or adding extra stock funds and accidentally changing the risk profile. |

| Self-built mix | Lower. You choose each component. | High. You set the stock/bond split and fund mix. | Higher. You must monitor drift, overlap, and fit over time. | Overcomplicating the lineup, skipping maintenance, or changing funds based on recent performance. |

A target-date fund is built to provide an age-appropriate allocation over time, and it has become the most common default path in plans. The tradeoff is that target-date funds are not interchangeable: GAO reports they vary considerably, including near retirement, where some hold 35 percent or less in equities and others 60 percent or more.

So use one verification step before submitting: check the target year, then confirm the fund's current stock/bond mix in the fact sheet or plan page. Do not assume funds with similar years behave the same way.

A self-built approach is sensible only when extra control solves a real need and you will maintain it. In many menus, that means combining a large-cap fund, mid-cap fund, small-cap fund, international stock fund, and bond fund. The tradeoff is direct: customization can improve fit, but it also raises behavior risk and monitoring workload.

Use a quick self-check before choosing a self-built mix: write each fund's job in one line. If two funds do the same job, you may be creating overlap instead of diversification.

Who this fits:

- Freelancers or creators with variable income: a one-fund setup is often cleaner because cash flow is already variable and fewer investment decisions reduce tinkering risk.

- Steady salaried contributors in a standard 401(k): either route can work, but a self-built mix fits best when you want allocation control and will review on schedule instead of reacting to headlines.

For more on core holdings, see A Guide to Index Fund Investing for Freelancers.

Put contribution order first because it changes outcomes more than fund tinkering#

After you choose your investment path, outcomes are usually driven more by contribution behavior than by more fund tweaking. In your 401(k) plan, use this order: capture available employer match first (if your plan offers one), then increase salary deferral deliberately as cash flow allows.

That priority keeps you focused on controllable levers. You cannot predict markets, but you can control contribution consistency, your allocation approach, and whether you stick to it long enough to work. The practical check is simple: confirm your plan's actual match and deferral-change process in plan documents, then follow that process on purpose.

Use benchmarks as context, not as your exact target#

General savings benchmarks can be useful for orientation, but they do not set the right deferral rate for your income pattern, expenses, or plan limits. For variable earners, exact targets are often unknown until you map them to your month-to-month cash flow.

Use an operational rule instead of a motivational target:

- Set a minimum recurring deferral you can sustain in normal or weaker months.

- Add a pre-set increase rule for stronger revenue months, so you are not deciding from scratch each time.

Discipline beats constant tinkering#

Inside the same 401(k) plan, consistent contributions plus a disciplined allocation approach usually matter more than frequent allocation changes. If your current mix still fits your risk, periodic review is usually more useful than reacting to headlines.

"Set it and forget it" should not mean ignore it for 30 years. The better middle ground is to automate contributions, keep the setup simple, and revisit only when your income stability, plan menu, or risk tolerance changes.

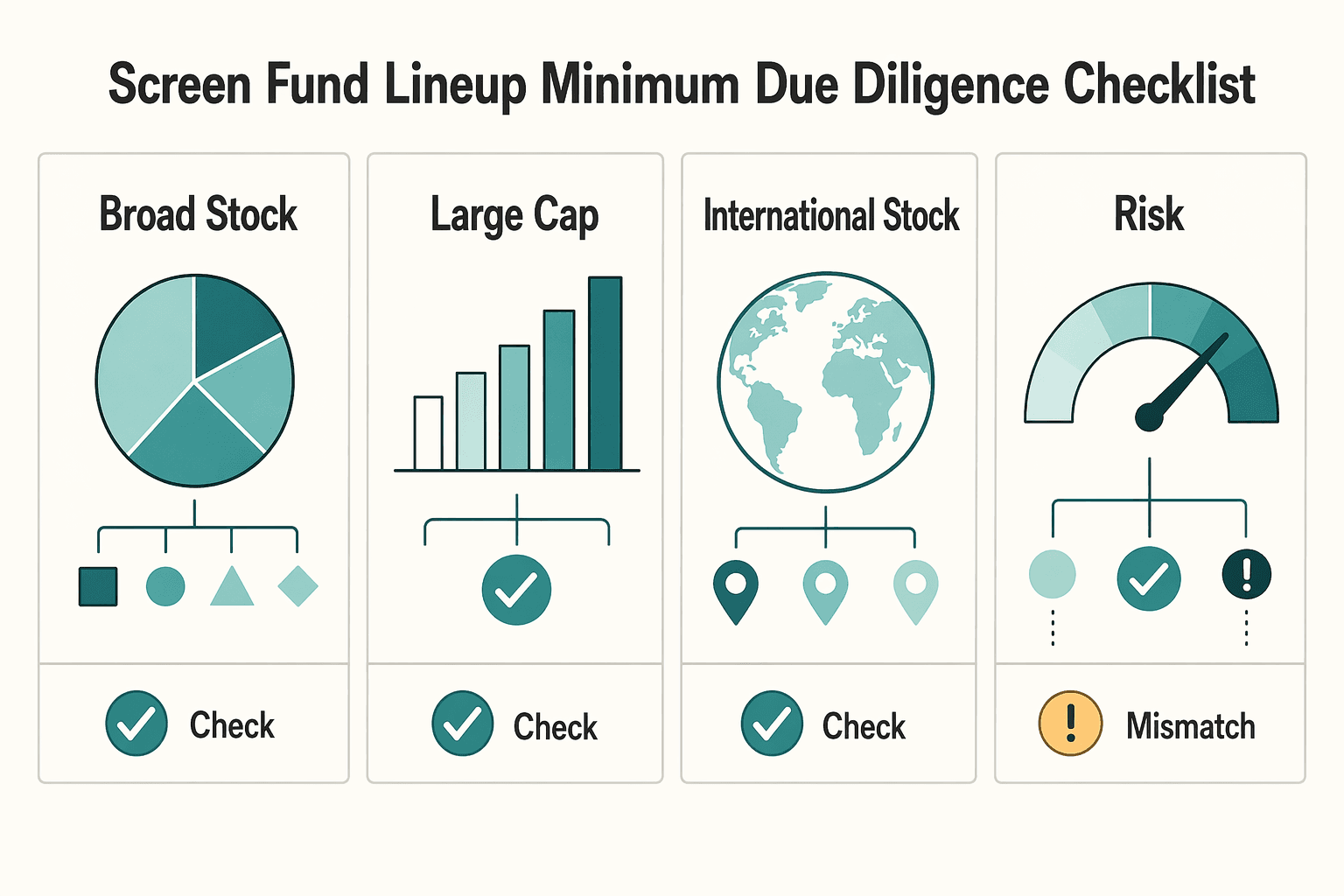

Screen your fund lineup with a minimum due diligence checklist#

Use a minimum due diligence checklist so every fund you select has a clear role before you submit elections. Treat the checklist as a decision aid, not a substitute for judgment.

Start with one line per mutual fund or exchange-traded fund (ETF):

| Fund option | Strategy label (from the plan page) | Asset bucket | Overlap risk to check | Role in your allocation |

|---|---|---|---|---|

| Broad U.S. stock fund | Broad U.S. equities | Stock fund | May duplicate a large-cap-heavy fund | Core stock exposure |

| Large-cap fund | U.S. large companies | Stock fund | May duplicate other U.S. stock holdings | Targeted stock exposure |

| International stock fund | Non-U.S. equities | Stock fund | May overlap with global stock exposure elsewhere | Diversify stock exposure |

| Bond fund | Broad or investment-grade bonds | Bond fund | May duplicate other bond holdings | Stability and risk balance |

Use two operating rules while you review:

- Run an overlap check so large-cap exposure is not duplicated across funds with similar holdings.

- If one bucket grows beyond the risk mix you intended, rebalance back to your target mix.

Before you confirm elections, run one final verification checkpoint:

- Each selected fund must have a one-sentence job in the portfolio.

- If a fund has no clear job beyond recent performance appeal, remove it.

If you are also choosing the plan provider, keep that review separate from fund selection. Provider due diligence should cover service scope, fee structure (what is included vs extra), and who handles compliance tasks such as Form 5500 filing and annual testing.

Understand IRS plan rules that affect real-world choices#

Separate plan mechanics from fund selection before you make changes. In a U.S. 401(k), IRS-linked rules on salary deferrals, loans, and withdrawals define how the plan operates, but they do not decide your portfolio mix.

| Topic | What the article says | Type |

|---|---|---|

| Salary deferrals | Employees can defer part of wages, and deferred amounts are generally taxed when distributed | Plan mechanic |

| Participant loans | A plan may offer participant loans, but it is not required to | Optional feature |

| Hardship withdrawals | A plan may offer hardship withdrawals, but it is not required to | Optional feature |

| In-service withdrawals | If allowed, distributions can face a possible 10% additional tax when you are under age 59-1/2 | Optional feature |

| Form 5500 filing | Regular 401(k) plans require annual Form 5500 filing | Administration |

| Nondiscrimination testing | Regular plans require testing so benefits do not favor highly compensated employees | Administration |

A 401(k) allows employees to defer part of wages, and deferred amounts are generally taxed when distributed. Confirm how your plan processes salary deferrals in its election flow and plan documents before you change contribution settings.

Treat loans and hardship withdrawals as optional plan features, not guaranteed tools. A plan may offer participant loans and hardship withdrawals, but it is not required to. If in-service withdrawals are allowed, distributions can face a possible 10% additional tax when you are under age 59-1/2.

If you are self-employed or running a small business, check administration duties separately from investing decisions:

- Regular 401(k) plans require annual

Form 5500filing. - Regular plans also require nondiscrimination testing so benefits do not favor highly compensated employees.

- Administrative costs may be higher than in more basic arrangements.

Use one quick filter: is this a plan rule or a portfolio rule? Loan availability, filing, and testing are plan-structure questions; stock-versus-bond allocation is an investment-strategy question. This guidance is U.S.-specific, so confirm local equivalents before acting in non-U.S. systems.

For a step-by-step walkthrough, see A Guide to Real Estate Investment Trusts (REITs).

Avoid the mistakes that quietly derail 401(k) investors#

Four quiet mistakes usually do more damage than the fund picks themselves: underfunding, unmanaged complexity, borrowed advice, and missed cross-border reporting checks.

| Mistake | What can go wrong | Article check |

|---|---|---|

| Choosing funds before locking contribution behavior | You can underfund the account while an employer match is available | Confirm your salary deferral rate, whether a match exists, and when changes take effect |

| Building a complex mix without a rebalancing rule | A long list of mutual funds can drift away from your intended risk | Define each fund's role and target percentage, set a review date, and rebalance back to target when allocations move materially |

| Treating anecdotal picks as universal advice | A coworker's favorite fund or an online allocation may not fit your plan menu, risk tolerance, or behavior under stress | Match outside ideas to your own plan options and the level of maintenance you will actually do |

| Ignoring cross-border reporting edge cases when they apply | Portfolio choices do not replace tax reporting obligations | Pull year-end statements, map each account to the institution that maintains it, and verify your filing status first |

Mistake 1: choosing funds before locking contribution behavior. If you set allocations before confirming payroll deferral settings, you can underfund the account while an employer match is available. Start with the payroll election screen and plan materials: confirm your salary deferral rate, whether a match exists, and when changes take effect.

Mistake 2: building a complex mix without a rebalancing rule. A long list of mutual funds can drift away from your intended risk if you never rebalance. If you build your own mix, define each fund's role and target percentage, then set a review date and rebalance back to target when allocations move materially.

Mistake 3: treating anecdotal picks as universal advice. A coworker's favorite fund or an online allocation is not automatically right for your 401(k) plan menu, risk tolerance, or behavior under stress. Use outside ideas as prompts, then match choices to your own plan options and the level of maintenance you will actually do.

Mistake 4: ignoring cross-border reporting edge cases when they apply. Portfolio choices do not replace tax reporting obligations. Certain U.S. taxpayers with specified foreign financial assets exceeding $50,000 report them on Form 8938, attached to the annual income tax return; thresholds are not uniform, and higher thresholds can apply for joint filers or taxpayers residing abroad. Required filers report financial accounts maintained by a foreign financial institution, and some accounts are excluded, including accounts maintained by a U.S. payer. If you are not required to file an income tax return for the year, Form 8938 is not required.

If FATCA, Form 8938, FBAR, or FinCEN might be relevant, do not guess from forum advice. Pull year-end statements, map each account to the institution that maintains it, and verify your filing status first.

Choose one path today and commit to a simple review rhythm#

Choose your path now: a one-fund target-date fund approach, or a small multi-fund allocation you can maintain without guesswork.

Pick the version you can explain in one sentence#

If you want low maintenance, use a target-date fund. If you want more control, build a deliberate mix from broad-based market index funds or other plain stock and bond fund options in your plan menu, and write down your target weights.

Use a simple test: can you explain what you own and why in plain language? A core caution still applies here: do not buy investments you do not understand.

Lock contribution decisions before you tweak fund choices#

Start with your plan document. It is where plan-specific details live, including employer match and vesting schedule.

Then set your salary deferral rule so capturing the employer match is not left to memory. Also confirm with your plan manager whether your plan offers Roth 401(k), traditional 401(k), or both before making major contribution-type changes.

Keep one lightweight record and one review habit#

Keep one short record with:

- your allocation and each fund's job

- your salary deferral rule and match checkpoint

- your review triggers (for example, income change, plan-menu change, or risk-tolerance change)

At each review, check whether your holdings still match your written allocation and whether contributions still fit your cash flow. If nothing material changed, leave the plan alone.

If your income or filing situation crosses borders, treat major 401(k) changes as a tax-checkpoint moment. Cross-border retirement decisions can involve local filing and tax considerations, so confirm details for your case before acting.

Frequently Asked Questions

What should I pick first in a 401(k) if I feel overwhelmed?

Start with the decision that changes outcomes fastest: your salary deferral rate. Then pick the simplest investment option you can explain in one sentence and stick with during a bad market. A common failure mode is spending all your time comparing funds while contributing too little.

How do I decide between a target-date fund and building my own fund mix?

The IRS excerpts here do not rank one as better. Use a target-date fund if you want a simpler, lower-maintenance approach. Build your own mix only if you are willing to give each fund a job, write down target weights, and maintain that process over time. The real tradeoff is not intelligence. It is maintenance and behavior.

Is increasing my contribution rate more important than choosing “perfect” funds?

Usually, yes. The IRS notes that elective salary deferrals are generally excluded from current taxable income, except for designated Roth deferrals, so increasing contributions can matter immediately for both savings rate and tax treatment. In practice, a solid contribution habit plus a simple allocation usually beats endless tuning inside the same 401(k) plan.

What IRS rules should I check before using a participant loan or hardship withdrawal?

First, confirm your specific plan even allows them, because the IRS treats participant loans and hardship withdrawals as optional plan features, not universal rights. Next, check whether what you are considering is an in-service withdrawal, because the IRS says it may be subject to a 10% additional tax if you are under age 59-1/2. Do not rely on a generic article here. Use your plan documents and the transaction labels in your account portal.

Can I hold a 401(k) and an Individual Retirement Account (IRA) at the same time?

In general, yes. The IRS says a business establishing a 401(k) can also have other retirement plans, which is the key point: one plan does not automatically block another. Treat them as separate decisions and verify the specific rules that apply to each account.

How often should I review and rebalance my 401(k) investments?

Set one review cadence you will actually follow, then avoid changing funds every time markets get noisy. The IRS materials here do not give a required rebalancing frequency. So use a practical checkpoint instead: review when your allocation has clearly drifted from your written target or when your job, cash flow, or risk tolerance has materially changed. If you cannot imagine maintaining that process, keep the fund lineup simpler.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cityofsacramento.gov/content/dam/portal/hr/documentlibrary/DCPC/N...trusted

- congress.gov/crs_external_products/R/PDF/R47996/R47996.3.pdftrusted

- congress.gov/bill/119th-congress/house-bill/1/text/ehtrusted

- dol.gov/sites/dolgov/files/ebsa/about-ebsa/our-activ...trusted

- federalregister.gov/documents/2022/12/01/2022-25783/prudence-and...trusted

- gao.gov/assets/gao-11-118.pdftrusted

- irs.gov/retirement-plans/choosing-a-retirement-plan-...trusted

- irs.gov/retirement-plans/choosing-a-retirement-plan-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Tax Implications for an Australian Resident Owning a US LLC

There is no one-size-fits-all shortcut for US LLC tax decisions across Australia and the United States. Setting up a US Limited Liability Company (LLC) is one step; getting the tax treatment right in both systems is where risk starts. If you are handling **australian owning us llc tax** decisions, treat this as a classification and documentation problem first, not a shortcut hunt. If you run a business of one, your job is to pick the defensible path and keep the paperwork tight.

How to Manage Your First Paycheck After Graduation

**Treat your first paycheck as a cashflow test, not a spending signal.** If you want to handle it well, the real job is not deciding what to buy or save this week. It is making sure next month still works if a payment arrives late, a deposit is smaller than expected, or you cannot immediately explain where money came from.