Quick Answer

Yes, a charitable remainder trust can fit when you are still before closing on an appreciated asset, want income over a defined term or lifetime, and genuinely intend a charitable remainder. The trust can sell assets within the structure and distribute through a fixed-dollar CRAT stream or a valuation-based CRUT stream. The tradeoff is commitment: once funded, principal is generally not available for personal liquidity, and trustee administration becomes part of your ongoing operating load.

You've Secured a Major Windfall. Don't Let a Six-Figure Tax Bill Be Your Reward.#

If you are preparing to sell a highly appreciated asset, tax drag shows up early. A personal sale can lock in a large gain before you decide how to redeploy the proceeds.

| Filing status | NIIT threshold |

|---|---|

| Single or head of household | $200,000 |

| Married filing jointly | $250,000 |

| Married filing separately | $125,000 |

Federal capital gains are not taxed at one fixed rate. They depend on your overall taxable income. The 3.8% Net Investment Income Tax can also apply above IRS thresholds. Those thresholds are $200,000 for single or head of household, $250,000 for married filing jointly, and $125,000 for married filing separately. Some states also tax capital gains, so model any combined rate only after verification.

Your key decision window is timing: are you still before closing, or are you already holding proceeds? Before closing, planning options may still be available. After proceeds are received, the gain is usually already realized, and your options are typically much narrower.

Ask your CPA and deal counsel one direct question early: is the sale already effectively committed?

Do not assume "not closed yet" means planning is still open.

One Tax Court outcome discussed in a March 15, 2023 summary found that donating stock two days before closing was too late. The court did not set a bright-line deadline.

Also gather your basis records now. If adjusted basis is not documented, you cannot model your true sale-tax exposure.

| Path | Taxable base at sale | Reinvestable capital right after sale | Planning flexibility |

|---|---|---|---|

| Sell personally | Personal gain measured against adjusted basis at sale | Reduced by federal tax, possible 3.8% NIIT, and any state tax | Lowest after closing |

| Pre-sale planning path | Depends on structure and timing before closing | Potentially more capital available to reposition | Highest before closing |

| After-sale planning only | Gain is usually already fixed from the completed sale | Limited to what remains after tax exposure | Narrow, mostly post-tax choices |

The rest of this guide helps you decide whether a charitable remainder trust fits your facts, timing, and charitable goals. It can be a strong tool in the right situation, but it is not the right move for every windfall.

You might also find this useful: A Guide to Setting Up a Trust for Asset Protection.

What is a CRT, and Why Should a "Business-of-One" Care?#

A charitable remainder trust (CRT) can make sense when you want one structure to do three things at once: move an appreciated asset before sale, pay income to living beneficiaries, and leave a required remainder to charity.

If you do not want a real charitable transfer at the end, this is usually the wrong tool.

In practice, a CRT is an irrevocable trust that holds contributed assets, makes required periodic payouts, and then sends the remainder to one or more qualified U.S. charitable organizations. Under IRC §664, CRATs and CRUTs are generally not subject to subtitle A income tax. That is why the sale inside the trust matters. The tradeoff is real: assets you contribute generally cannot be taken back, and UBTI is an explicit exception with an excise-tax consequence.

First, you move the asset into the trust#

In practice, you transfer the asset into the trust before the trustee executes a sale. Typical candidates include closely held business interests, concentrated stock, and real estate. Virtual currency is treated as property for federal tax purposes, but eligibility still depends on trustee and trust-specific constraints.

| Asset type | Note |

|---|---|

| Closely held business interests | Listed as a typical candidate |

| Concentrated stock | Listed as a typical candidate |

| Real estate | Listed as a typical candidate |

| Virtual currency | Treated as property for federal tax purposes, but eligibility still depends on trustee and trust-specific constraints |

Confirm that the trust is signed, funded, and actually holding the asset before the trustee executes the sale.

Next, the trustee executes the sale and reinvestment#

Once the asset is in the trust, the trustee handles the sale inside the trust and reinvests the proceeds. IRS guidance states that CRTs can defer income taxes on the sale of assets transferred to the trust.

This is not just paperwork. You are deciding who sells, who manages the assets, and how concentrated wealth gets turned into an income-producing portfolio.

Then, payouts run under the design you chose#

A CRT must pay income to at least one living beneficiary, for life or for a term of up to 20 years. The two main payout designs are:

- CRAT: fixed dollar payout each year.

- CRUT: annual payout set as a percentage of trust value.

The payout rate must be at least 5% and no more than 50%, and the charitable remainder must be at least 10% of initial net fair market value. Payout design is not just a preference. It has to satisfy structural limits.

Finally, charity receives what remains#

The remainder goes to qualified U.S. charities at the end of the payout term.

That charitable transfer is mandatory, and you cannot later reverse it by reclaiming principal.

| You keep | You give up |

|---|---|

| Choosing the trustee | Reversing the transfer after funding |

| Setting beneficiary and payout design at drafting | Open access to principal for personal use |

| Choosing CRAT (fixed) vs. CRUT (variable) | A purely personal-sale outcome with no charitable remainder |

| Naming charitable recipient(s), subject to trust terms | Unlimited flexibility once documents are final |

For a business-of-one, this matters when most of your net worth sits in one appreciated asset and you need that value to become ongoing cash flow. The mechanics can work, but they are only the first layer. Before you implement anything, compare CRT outcomes against a taxable sale with side-by-side math.

For a step-by-step walkthrough, see How to Set Up a Donor-Advised Fund (DAF).

The Strategic Math: CRT vs. Paying Capital Gains#

This is usually a tradeoff decision, not a search for a universal winner.

A CRT can keep more sale value working right after the transaction. In exchange, you give up flexibility and take on irrevocability, a required charitable remainder, and more complexity.

Assumptions that move your result#

Model outputs are only as good as the inputs. Verify these before you rely on a comparison:

- Asset basis and unrealized gain

- Jurisdiction and filing profile

- Current tax-rate assumptions, after verification

- Trust type (

CRATorCRUT) - Payout design, beneficiary term (life or up to 20 years), and market return assumptions

- Modeled outcomes, after verification

Your result will vary by profile. The same sale value can lead to very different outcomes depending on basis, tax exposure, trust design, and portfolio performance after funding.

| Decision point | Sell personally and pay capital gains | Use a CRT before sale |

|---|---|---|

| Immediate tax impact | You generally handle capital-gain tax at sale under your current tax profile. | The trust itself is generally exempt from income tax during the trust term, so the in-trust sale changes immediate tax treatment at the trust level. |

| Reinvestable base after sale | You invest what remains after taxes are paid. | More of the gross sale value can stay invested inside the trust from the start. |

| Projected income-path behavior | Your income path depends on how you invest and withdraw personally. | CRAT: fixed dollar annuity. CRUT: fixed percentage of annually revalued assets, so payouts move with portfolio value. |

| Tax timing to you | Tax is typically paid at sale, then future income follows personal tax rules. | Gain from appreciated assets sold inside the trust is generally taxed to the income beneficiary through annual payments over time. |

| Charitable remainder effect | No mandatory charitable transfer. | Remaining assets must pass to a qualified charity at the end of the trust term. |

| Liquidity access | You keep direct access to post-tax principal. | You receive the payout stream set by the trust. Principal is not open for personal access, and the trust is irrevocable once funded. |

| Complexity burden | Fewer structural and administrative moving parts. | Higher setup and administration burden, plus trustee selection, investment oversight, and compliance work. |

The core advantage is usually the capital path, not "no tax."

If an appreciated asset is sold inside the trust, more capital may remain invested earlier. Gains are generally recognized to you through payouts over time. That can be useful when you want long-term income and already intend to make a charitable transfer.

The balancing point is control. Once funded, the trust cannot be undone, and you are committed to the payout structure and charitable remainder. If you expect to need unrestricted principal for business uses or personal liquidity, the taxable-sale path may fit better even when the tax math looks less efficient.

Keep one modeling guardrail in place: do not treat the § 7520 rate as a return forecast.

It is used to calculate the charitable deduction at inception. Post-funding results depend on investment performance, asset allocation, market conditions, and trustee decisions.

As a practical screen, check that the asset size justifies the added burden. A commonly cited starting point is around $100,000 because setup and ongoing administration can otherwise absorb too much of the benefit.

For related tax-planning context, see A Guide to Backdoor Roth IRAs for High-Earners.

De-Risking the "Irrevocable" Decision: How to Retain Control#

The hardest part of this decision is usually not the tax math. It is whether you can accept that assets transferred into a CRT are generally not coming back.

If you may need that principal for business or personal liquidity, this structure is usually a poor fit no matter how attractive the model looks.

Irrevocable does not mean zero control. It means most of your control sits at the drafting stage. Flexibility that is not written into the trust terms is often unavailable later, or much harder to change.

What you control before funding#

Before assets move, you can set the core terms that matter most:

- Noncharitable beneficiaries

- Payment term, for life or up to 20 years

- Payout structure (

CRATorCRUT) - Payout rate, within the 5% to 50% range and subject to qualification rules

You may also be able to reserve a power to substitute the charitable remainder beneficiary, but only if that right is expressly drafted.

Do not assume it exists by default.

Control limits are jurisdiction-specific, so verify local-law constraints before funding.

What you no longer control after transfer#

Once assets are transferred, you generally cannot reclaim them. You can receive payments under the trust terms, but the principal is no longer your emergency reserve. Some limits are structural:

- Payment duration is fixed by design, either life or the selected term

- The charitable remainder must be at least 10% of the initial net fair market value contributed

- In a

CRAT, the governing instrument must prohibit additional contributions

A common failure mode is over-focusing on deferral and underestimating the loss of direct access and post-transfer flexibility.

CRAT vs. CRUT through a control-and-risk lens#

| Risk lens | CRAT | CRUT |

|---|---|---|

| Payout basis | Fixed dollar amount each year | Fixed percentage of trust assets, valued annually |

| Income stability | More stable in nominal dollars | Varies with annual asset value |

| Inflation exposure | Fixed dollars can lose purchasing power | May track growth better if assets grow, but there is no automatic inflation protection |

| Market sensitivity | Lower impact on payout level | Higher, because payout depends on annual valuation |

| Payout administration | Fixed payout amount once set | Requires annual valuation to calculate payouts |

| Additional funding after setup | Additional contributions are not allowed | Do not assume contribution flexibility without verifying the trust form and document |

| Tends to fit | You prioritize predictable income | You can tolerate payout variability tied to asset value |

Choose based on cashflow tolerance, not preference alone.

If fixed obligations drive your monthly plan, a CRAT may be easier to plan around. If you have outside liquidity and can absorb variability, a CRUT may fit better.

A short pre-commit checklist#

Before you fund, pressure-test the decision like an operator, not a shopper. Use this checklist to see whether the tradeoffs work in real life:

- Confirm cash-reserve needs. Keep enough liquid assets outside the trust for taxes, living costs, and business surprises.

- Stress-test income variability. Model flat and down-market scenarios, especially for

CRUTpayouts tied to annual valuation. - Define trustee oversight. Decide who reviews valuations, payout calculations, investment statements, and Form 5227 filing.

- Document change rights in the trust terms. If you want any reserved powers, draft them explicitly and verify them under local law.

If you complete these checks before funding, "irrevocable" becomes a defined set of tradeoffs you can manage, not a vague risk. Related: How to Run a Profit & Loss Report in QuickBooks.

What Are the Real Risks and Costs? A Transparent Look#

Use a stricter standard than tax upside alone. A CRT is a high-commitment structure, so the real test is cashflow reliability, administrative burden, and your comfort with transferring appreciated assets into an irrevocable trust.

Costs you can actually price#

Start by separating costs into two buckets: setup and ongoing costs.

Ask your advisor and trustee to itemize both in writing before you move any asset.

Before you fund, ask exactly how payouts are calculated and reviewed each year. In a CRUT, trust assets are revalued at the end of each year, and payouts are based on that value. In a CRAT, confirm the payout terms in the document and confirm that additional contributions are not allowed after initial setup.

Where structure changes your risk exposure#

| Exposure | CRAT | CRUT |

|---|---|---|

| Payout basis | Payout terms are set at creation | Percentage of trust assets, based on end-of-year valuation |

| Valuation checkpoint | Valued at creation | Revalued at the end of each year |

| How payouts can change | No annual revaluation of trust assets in payout mechanics | Annual revaluation can change the payout basis year to year |

| Funding after setup | Additional contributions are not allowed after initial setup | Verify contribution rules in your draft documents |

Both structures must keep annual payouts within the 5% to 50% range, but the path to that payout is different.

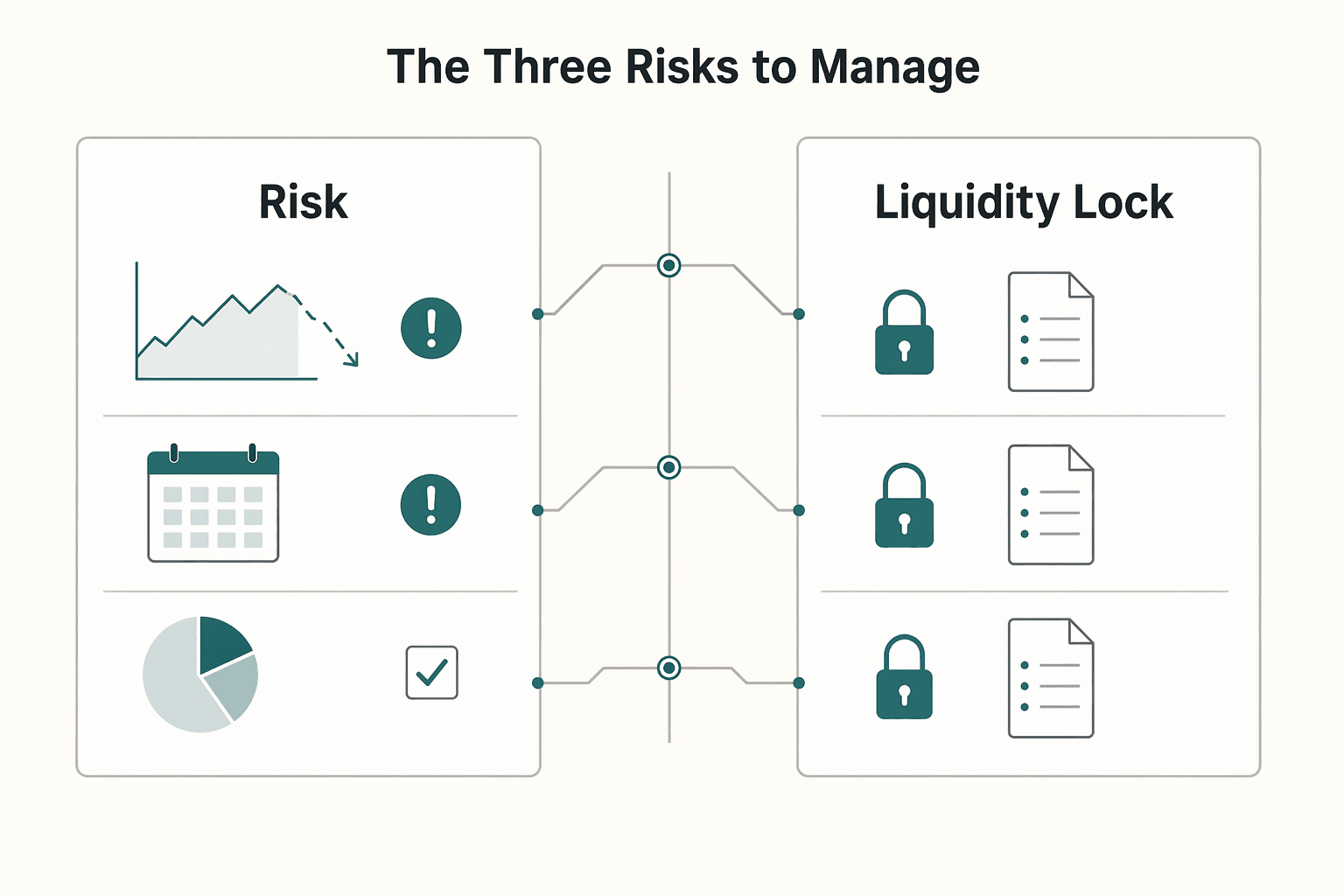

The three risks to manage#

Keep the main risks concrete:

| Risk | Management step |

|---|---|

| Market risk | Stress test the plan under weaker portfolio values and confirm the allocation can support the chosen payout approach |

| Trustee risk | Ask for the written fee schedule, valuation process, reporting cadence, and payout calculation method; set a recurring oversight review; confirm beneficiary designations |

| Liquidity lock-in | Keep a separate reserve outside the trust for taxes, living costs, and business gaps |

Market risk: This matters most if you depend on distributions for living expenses.

Trustee risk:

Treat trustee selection as an operating decision.

Ask for the written fee schedule, valuation process, reporting cadence, and payout calculation method, then set a recurring oversight review. Also confirm beneficiary designations, because gift taxes may apply if the noncharitable beneficiary is someone other than you or your spouse.

Liquidity lock-in: Once assets are transferred to an irrevocable trust, plan as if those assets are committed for trust purposes rather than short-term emergencies. Keep a separate reserve outside the trust for taxes, living costs, and business gaps.

Before you proceed#

- Choose your payout tradeoff: terms set at creation (

CRAT) or annual valuation-linked payouts (CRUT). - Get draft documents and written fee terms before any transfer.

- Verify beneficiary designations and possible gift-tax exposure.

- Keep enough liquidity outside the trust so your plan does not depend on accessing transferred principal for emergencies.

This pairs well with our guide on A Freelancer's Guide to Donating to Charity (and the Tax Benefits).

Before you commit to a long-term trust payout plan, pressure-test your ongoing receive-and-withdraw costs. That helps keep cashflow predictable. Use this payment fee comparison.

Your Next Move: Is a CRT the Right Strategic Tool for You?#

If you need to keep full access to principal, this is probably a no. A CRT is irrevocable, so the decision should come down to fit: your asset situation, your income needs, and your real charitable intent.

Run four go/no-go checks#

Start with four practical checks before you spend time on drafting.

- Do you have a real liquidity event tied to appreciated property?

If yes, a CRT may be relevant because the structure is built around transferring appreciated assets, like stock, real estate, or private business interests, and having the trust sell them. If you do not have a pending sale or a concentrated appreciated position, a CRT may add complexity without solving your main problem.

- Is the asset size practical for this structure?

Use the current practical minimum asset size only after verification. Then test that amount against setup cost, ongoing administration, and trustee minimums.

- Do you want durable income more than maximum flexibility?

A CRAT pays a fixed annuity and does not allow additional contributions. A CRUT pays a fixed percentage of annually revalued assets and may allow additional contributions. Confirm your payout design, term structure, and contribution flexibility against the trust form and documents before you rely on it.

- Is the charitable outcome a true objective for you?

A CRT is a split-interest vehicle, not just a tax tactic. The remainder goes to charity, so treat that as a core goal, not a side effect.

Compare CRT vs. selling outside a trust#

| Decision point | CRT | Sell and reinvest outside a trust |

|---|---|---|

| Immediate tax impact | Planning sources describe the trust-level sale of contributed assets without immediate capital gains tax inside the trust | Tax treatment follows your personal sale and reinvestment path |

| Income predictability | Can be designed as fixed annuity (CRAT) or percentage-based payout (CRUT) | Depends on your portfolio and withdrawal policy |

| Control and liquidity | Principal is transferred irrevocably | You keep direct ownership and can change course more freely |

| Charitable outcome | Remainder passes to charity at term end | No built-in charitable remainder unless you add one separately |

The core tradeoff is control versus structure. Selling directly often keeps liquidity simpler, while a CRT may improve planning outcomes in the right case but adds legal drafting, ongoing administration, trustee execution, and advisor coordination.

Bring this checklist to your advisors#

- Gather asset details: current value, adjusted basis, holding period, and expected sale timeline.

- Define income needs in plain numbers: amount, frequency, and fixed vs. variable preference.

- Shortlist trustee options and confirm operational responsibilities in the trust documents.

- Take this file to an estate attorney and tax advisor for side-by-side modeling.

If your answers are clear on all four checks, you are close to a decision. If not, pause and model before you commit.

If you want a deeper dive, read A Guide to QuickBooks Self-Employed for Freelancers.

If a CRT is likely your next move, align your post-sale money flow with compliance gates and audit-ready operations by starting a practical planning conversation through Gruv.

Frequently Asked Questions

What is the minimum amount for a charitable remainder trust?

The grounding materials here do not state a single fixed dollar minimum. They do require that the charitable remainder be at least 10% of the initial net fair market value. Verify your proposed funding amount and trust design against that test and your expected income and administration needs before making an irrevocable transfer.

What are the main disadvantages of a charitable remainder trust?

The main disadvantages are loss of access to principal, ongoing administration, and a payout that may be fixed or variable depending on structure. In a CRAT, the payout is a fixed dollar amount each year. In a CRUT, it is a percentage of trust assets determined annually, so the amount can rise or fall with valuation. Verify payout mechanics, the annual valuation process, and who handles reporting before you commit.

Can you fund a charitable remainder trust with cryptocurrency?

Potentially yes, because the IRS treats virtual currency as property for federal income tax purposes. If virtual currency is sold, the IRS says capital gain or loss must be recognized. Verify valuation, liquidation, and reporting mechanics before you commit.

How long does the income stream from a CRT last?

You can set payments for one or more beneficiaries' lives or for a fixed term of up to 20 years. That choice affects your cashflow plan and whether the draft meets the rule that the charitable remainder must be at least 10% of the initial net fair market value. Verify beneficiary designations, term design, and that the draft passes the 10% remainder test before signing.

Who should be the trustee of my CRT?

The trustee is a fiduciary responsible for holding and managing trust property. The better choice between an individual and a corporate trustee depends on your operating capacity and oversight needs, because trustee execution drives valuation, payouts, filings, and beneficiary reporting. Verify who files Form 5227, how each beneficiary's distributions are reported, and how CRUT valuations are performed.

Can I change the charity later on?

The grounding materials here do not establish a universal right to change the charity later. Because the trust is irrevocable, any change authority should be treated as document-specific and confirmed during drafting before you assume it exists.

Do I owe tax when I receive distributions?

Often yes, at least in part. Distributions follow statutory ordering rather than one flat tax character, with ordinary income first, then capital gain, and corpus last. Verify how your advisor models likely distribution character over time and whether unrelated business taxable income exposure could trigger trust-level excise tax.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- codes.ohio.gov/ohio-revised-code/chapter-109trusted

- congress.gov/113/chrg/CHRG-113shrg93919/CHRG-113shrg93919...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- federalregister.gov/documents/2017/11/15/2017-23953/medicare-pro...trusted

- govinfo.gov/content/pkg/FR-2008-07-14/xml/FR-2008-07-14.xmltrusted

- irs.gov/charities-non-profits/charitable-remainder-t...trusted

- irs.gov/individuals/international-taxpayers/frequent...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

A Guide to QuickBooks Self-Employed for Freelancers

**QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.**

How to Run a Profit & Loss Report in QuickBooks

**Use your QuickBooks profit and loss report as a risk control system, not a bookkeeping chore.** If you invoice clients, this report helps you spot margin pressure and make earlier operating decisions.

When a Trust for Asset Protection Makes Sense for Your Business

Use a trust only after your core liability setup is solid. A trust for asset protection is an escalation layer, not a substitute for entity separation, insurance, or clean operations.