Quick Answer

Start by running your deal like a business system: separate accounts, reserve taxes, and budget only from installments that have actually cleared. With book advances and royalties, timing matters as much as totals because payments often arrive at signing, manuscript delivery, and publication while royalty reports may come on a slower cycle. Read royalty basis terms directly from the final contract version, then audit each statement line before updating your forecast or spending decisions.

Beyond the Thrill of "Yes": A CEO's Guide to Managing a Book Advance#

Treat your book advance as business capital before you spend any of it. The first risks show up immediately: publishing contract terms, tax exposure, and cashflow control.

A headline advance is not the same as cash in hand. Advances are usually paid in installments, often at signing, manuscript delivery, and publication. Royalties may be reported only twice a year. If you budget from the total offer instead of the payment schedule, you can run short before later payments arrive.

First week triage#

Before any discretionary spending, handle these four steps:

- Open or assign a separate bank account for writing income and expenses so business and personal funds do not mix.

- Collect the core contract paperwork: draft publishing contract, payment schedule, and rights and royalty terms.

- Schedule advisor check-ins early. If you are U.S. self-employed, estimated tax payments are generally required quarterly in a pay-as-you-go system, and IRS guidance includes considering a tax professional.

- Set decision ownership now: define who handles contract terms, tax planning, cashflow planning, and approvals before money moves.

Use one checkpoint before you spend: confirm each installment trigger and timeline in the contract, and confirm any conditions tied to payment timing. A common mistake is spending against the headline number while timing and tax obligations are still unresolved. Keep the CEO mindset: protect the deal first, then plan the money. The next step is to read the contract the way a CFO would. Related: Germany Freelance Visa: A Step-by-Step Application Guide.

Deconstructing the Deal: How to Read a Publishing Offer Like a CFO#

Use this section to decide whether the offer is ready for a real decision. If you cannot identify the controlling version and pull the key money clauses exactly as written, you are not ready to judge deal quality.

Start with version control, not opinions#

Start with document status. A draft is not the final contract, and an email summary is not the controlling text. Apply that same discipline to your offer set.

If you have an email summary, term sheet, redline, and clean draft, confirm which document controls and what changed between versions. Lock down the file date, filename, and attachments before you evaluate the economics.

Extract money terms exactly as written#

Do not rely on shorthand or assumptions.

If terms like advance, earn out, non-returnable, royalty basis, escalator, or reserve appear, use the contract's own definitions and conditions.

| Deal element | What to pull from the document | Red flag |

|---|---|---|

| Payment triggers | Exact event that releases each payment and required approvals | Trigger language is discretionary or undefined |

| Royalty basis definitions | The defined basis for each format/channel and where that definition lives | Basis is referenced but not clearly defined in the controlling text |

| Escalator language | What counts toward thresholds, and where scope limits are stated | Threshold rules are vague or split across inconsistent drafts |

| Reserve language | Why amounts can be held and what releases them | Release timing is missing or open-ended |

| Rights-related revenue splits | Which rights are granted or retained and how revenue is split | Split appears in email but not in contract or rider |

Review sequence before acceptance#

Work in order. If you skip ahead to the headline number, you can miss clauses that affect payment timing and later calculations.

| Input | Detail |

|---|---|

| Version control | document name, version date, and included attachments |

| Compensation | total stated compensation and each payment trigger |

| Recoupment | recoupment or earn-out wording, if present |

| Royalty basis | royalty basis by format, channel, and territory, if present |

| Escalator | escalator clause text, if present |

| Reserve | reserve clause text and release terms, if present |

| Rights | rights granted versus retained and related split language |

| Payment release proof | proof or approval requirements before payment release |

- Confirm payment-trigger wording.

- Confirm royalty-basis definitions in the controlling version.

- Confirm escalator conditions and counting rules.

- Confirm reserve holdback and release terms.

- Confirm rights grants and revenue-split language.

Before you move to tax and cashflow planning, make sure you have extracted all eight inputs above from the controlling draft.

If any of these points are unclear, treat the offer as incomplete and resolve the text first rather than inferring missing terms. You might also find this useful: A guide to 'literary agents' and how to query them.

Pillar 1: The Corporate Shield - Mitigating Risk and Optimizing Taxes#

Decide where the money lands before the first installment arrives. Here, entity setup and tax planning are risk controls. They shape personal-asset exposure, tax treatment, and how smoothly you handle uneven payments.

Choose the structure before cash arrives#

Start with the risk question, not the tax trick. Do you need legal separation, or do you just need the simplest workable setup? Your choice affects taxes, ongoing requirements, and how much personal risk you carry.

| Option | What you get | Admin reality | Good fit | Escalate for review when |

|---|---|---|---|---|

| Sole proprietor | No separate incorporated entity | No separate-entity formalities | You accept no legal separation between you and the business | You want clearer liability separation |

| LLC | State-created entity; federal tax treatment depends on elections and members | Usually lighter than a corporation | You want a state-created entity with flexible federal tax treatment options | You need to decide the LLC's federal tax classification |

| S corporation election | IRS tax election (Form 2553), not a separate state-law entity type | Requires election and ongoing tax/compliance coordination | You are evaluating S-corp treatment as part of entity planning | You are considering Form 2553 at all |

A simple flow works here. If legal separation is not your priority, a sole proprietorship may be workable. If you want a state-created entity, an LLC is often the next step. If you are considering S-corp treatment, make it a licensed CPA or attorney review, not a DIY toggle.

One caution matters: forming an LLC does not, by itself, settle federal tax treatment. The IRS can treat an LLC as disregarded, partnership, or corporation depending on elections and member count.

Use contract timing as a planning lever#

Because advances are usually paid in installments, payment timing can affect cash flow and year-end tax planning. If installment milestones are close to year-end, ask whether the schedule can better match the actual work timeline and smooth income across years.

This only works when the trigger language is clear and achievable. If your plan depends on a bracket, phaseout, or similar cutoff, verify the current rule before you rely on it. Also remember that advances are offset against future royalty payments, so additional royalty checks may not arrive until the advance earns out.

If you live abroad, source and tax home drive the result#

For U.S. citizens abroad, start with where the services were performed, not where the publisher is located. Personal-service income is generally sourced to the place the work is done.

| Topic | Detail |

|---|---|

| Service-income source | Personal-service income is generally sourced to the place the work is done |

| Tax home | For FEIE and housing benefits, your tax home must be in a foreign country throughout the qualifying period |

| Physical presence test | 330 full days in 12 consecutive months |

| Form | Use Form 2555 if you qualify |

| 2026 FEIE maximum | $132,900 per qualifying person |

| Support file | the signed contract and installment schedule; your travel calendar and passport-entry history; work records showing where writing and revisions occurred; documents supporting your foreign tax home; publisher statements, bank records, and any Form 1099 series received |

Then confirm tax home. For FEIE and housing benefits, your tax home must be in a foreign country throughout the qualifying period. One route is the physical presence test, which requires 330 full days in 12 consecutive months. If you qualify, use Form 2555. For tax year 2026, the maximum FEIE is $132,900 per qualifying person.

Build your support file early with the signed contract and installment schedule, your travel calendar and passport-entry history, work records showing where writing and revisions occurred, documents supporting your foreign tax home, and publisher statements, bank records, and any Form 1099 series received.

Build an operational reserve policy#

Treat each installment as gross cash, not spendable cash. Move the tax portion into a separate tax account as soon as the funds clear.

If you expect to owe at least $1,000 after withholding and refundable credits, estimated-tax planning applies. Standard due dates are April 15, June 15, Sept. 15, and Jan. 15 of the following year, so track them as payment deadlines.

Use a fixed reconciliation routine. After each installment, log the gross amount, receipt date, and the trigger that released it. Reconcile that ledger to publisher statements when they arrive. Some publishers report royalties twice a year, and royalties of at least $10 may be reported on Form 1099-MISC. At filing time, compare your records against your IRS wage-and-income transcript to catch missing forms, duplicates, and timing mismatches.

Once the money is landing in the right place and tax cash is set aside, the next job is turning a lump sum into something you can live on month to month.

For a step-by-step walkthrough, see A Deep Dive into the 'Royalties' Article of the US-UK Tax Treaty for Authors. If your writing work spans countries, validate your residency assumptions before finalizing your tax set-aside plan with the Tax Residency Tracker.

Pillar 2: The Advance-to-Salary Engine - Creating Stability from a Lump Sum#

If you treat an advance as operating cash, use a conservative monthly draw and explicit review checkpoints. This is process guidance only, not legal or tax advice, and decisions should be based on your particular circumstances.

Set the draw before you spend#

Set a provisional draw from cash that has cleared and the time horizon you need to cover, not from the deal headline.

Build it in this order:

- Start with gross advance cash that has actually cleared.

- Set aside a tax reserve based on advice for your situation.

- Subtract one-time obligations that must be paid from this pool.

- Treat what remains as a tentative draw pool.

- Set a temporary monthly draw and review it as conditions change.

Before you lock in the number, check it against installment timing in your contract. If later installments are uncertain or not yet paid, base your draw on received cash only.

Stress-test the plan#

A draw is only useful if it survives delays and surprise costs. Stress-test it before you automate anything, and revise it as soon as a shortfall appears.

| Bucket | What belongs here | Why it matters | Adjust if shortfall appears |

|---|---|---|---|

| Fixed essentials | Housing, utilities, insurance, debt minimums, food, core transport | These are non-optional; your draw has to clear them first | Reduce draw, revisit assumptions, or add interim income |

| Variable business costs | Software, website, research, contractors, travel, promotion, professional services | Irregular business spend can quietly drain personal cashflow | Pause noncritical spend, separate business budget from personal draw, or re-time purchases |

| Contingency buffer | Delayed payment, extra revision cycle, medical issue, admin or banking error | Helps one bad month from breaking the system | If buffer use repeats, reset assumptions and re-forecast |

Run two scenarios before you automate transfers: an expected month, and a month with one delayed payment or one unplanned bill. If scenario two fails, revise the draw first.

Automate the money movement, then review it#

Separate accounts and use a fixed transfer cadence so the system stays auditable. Keep incoming payments, tax reserves, and personal draws distinct. Transfer personal pay only after funds clear and reserve moves are complete.

Set review triggers and act on them when a new installment arrives, delivery timing changes, a major new expense appears, or household costs stay higher for more than a short stretch. Keep a small operating file with the contract, installment schedule, account statements, recurring-expense list, and transfer log.

Negotiate for timing, not just total dollars#

When terms are still open, prioritize payout timing and milestone clarity. Ask for release triggers you can verify operationally, and avoid relying on milestones with unclear acceptance language.

If a payment trigger is hard to verify in practice, treat that cash as uncertain in your draw model until it is actually received.

Once your draw is stable, protect the longer tail of the deal. That means reading royalty reporting as carefully as you read the offer. This pairs well with our guide on How to Get Book Reviews on Amazon and Goodreads.

Pillar 3: The Royalty Audit System - Protecting Your Long-Term Revenue#

Use a simple rule: do not treat any royalty statement as proven accurate until you audit it. This is not about assuming bad faith. It is about making long-term income decisions from verified numbers.

Run one repeatable audit each statement cycle#

Repeat the same audit each cycle so you can spot changes quickly and keep a clean record.

- Gather the statement and the contract pages that govern it, plus any amendments or rights notices tied to that period.

- Map statement lines to contract terms and flag anything you cannot trace clearly.

- Reconcile against outside signals where possible: bookseller signals, BookScan, and other independent data points.

- Log variances in one place: date, period, line item, expected treatment, actual treatment, and evidence.

- Raise line-specific questions in writing, then file responses with that cycle's audit notes.

Read each line by cashflow impact, not by label alone#

Read the statement for what it changes in your forecast, not just what the line is called:

| Statement line | What to check |

|---|---|

| Sales activity lines | Check whether reported activity is broadly consistent with your outside checkpoints before you revise revenue expectations |

| Returns and reserves | If these appear, treat them as timing-sensitive lines and track whether later statements reconcile as expected |

| Rate application | Confirm the applied terms match the governing contract language for that line item |

| Rights income | If a rights deal was communicated, look for a traceable entry in reporting and flag gaps quickly |

Where to check first by channel#

Different channels create different reporting issues, so start with the same sequence each cycle: contract term, statement entry, then outside signals.

| Channel | What can mislead you | What to check first |

|---|---|---|

| Statement labels can look clear even when totals need context | Compare reported activity with contract terms and your external checkpoints | |

| Ebook | Storefront pricing can change quickly and may not reflect royalty math | Verify statement entries against contract terms; do not infer royalties from listing prices alone |

| Other formats/channels | Reporting labels and timing may vary by report | Ensure each line is traceable to a contract term or documented notice |

Retail pricing can move fast and even invert across formats, so storefront snapshots are not enough on their own. Base your check on contract terms plus statement entries.

Build evidence before you query#

Build the evidence pack first, then ask your question. Keep a compact file each cycle: the statement, relevant contract pages, the prior statement, rights-sale notices, and your outside checkpoints. When you raise a query, include the period, page or line, format, and the contract language you are applying.

Treat repetition as the main red flag. One anomaly might be clerical. Repeated mismatches across cycles or lines can point to a broader reporting problem.

Use audit records in your next negotiation#

Your audit log is also negotiation prep. Use it to ask for clearer statement categories, more traceable reporting, and better reporting transparency where your records show friction. Documented examples also help you negotiate contract language that is easier to monitor in practice.

If you want a deeper dive, read How to Calculate Your Billable Rate as a Freelancer.

Conclusion: You Are the CEO of Your Intellectual Property#

After you sign, your job is to run the deal, not admire it. With a publishing contract, the practical move is to treat the money as business capital: protect risk, manage cashflow, and verify accounting.

The three pillars lead to three outcomes:

- Risk protection: keep the signed contract, payment schedule, and tax records organized from day one.

- Cashflow stability: advances are usually paid in installments, so plan each tranche against your budget instead of treating the full advance as available now.

- Long-term royalty control: the advance is offset against future royalties, and under standard advance terms you receive additional royalty checks only after the book earns out.

Keep the safeguards simple and repeatable. Store the final agreement, negotiated changes, and royalty statements together. Confirm that statement lines match your negotiated terms, because statement forms are not always updated to reflect contract changes. If your contract includes an audit clause, treat it as a primary tool for checking publisher accounting. If reserves for returns appear, confirm that the statement shows how many copies were actually returned.

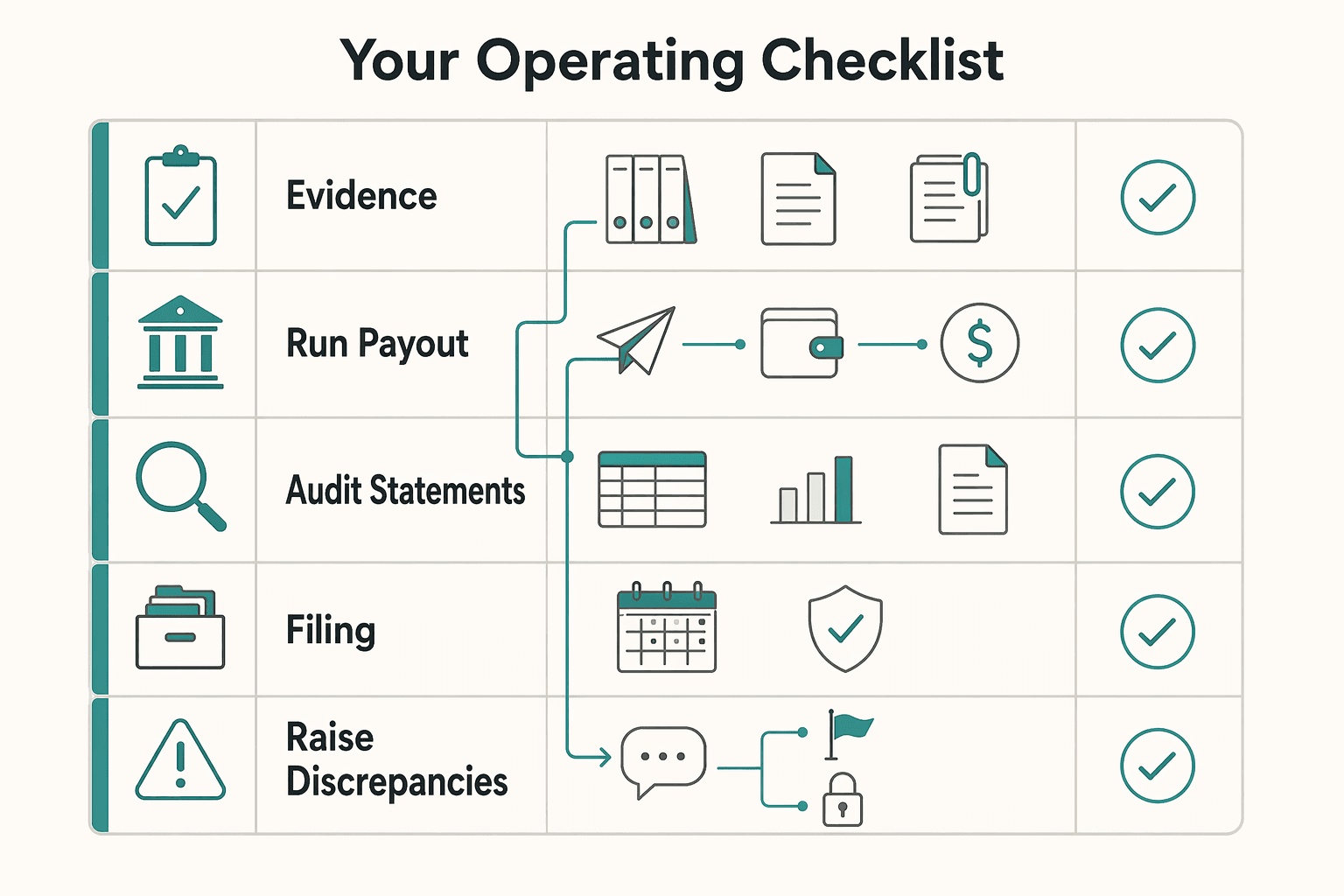

Your operating checklist#

- Set up safeguards immediately after signing: centralize contract and payment records.

- Run your payout system: map installment timing against your monthly obligations so delays do not create a cash crunch.

- Audit statements on a recurring cadence: many contracts use twice-yearly accounting periods, so calendar review dates now.

- If you are U.S. self-employed, plan for annual filing and generally quarterly estimated taxes; filing is required if net self-employment earnings are $400 or more.

- Raise discrepancies in writing with the statement period, line reference, and the contract clause you are applying.

The payoff is practical: more control, fewer surprises, and better decisions each time money or rights move. We covered this in detail in How to Find Beta Readers for Your Book and Use Their Feedback Well. If you want the same control in your client payment operations, review Merchant of Record for Freelancers.

Frequently Asked Questions

How are book advances taxed if you work as an independent author?

Advance and royalty tax treatment can vary by country, and some countries allow income averaging in some cases. Check your contract terms, tranche payment dates, agent remittances, and expense records so you can match what was paid, when, and to whom. Record each tranche separately, set aside tax cash using a verified rate that fits your situation, and confirm filing treatment with a qualified tax professional.

Should you set up an entity for a publishing deal?

Whether to set up an entity is jurisdiction-specific and deal-specific, and it is not required in every author situation. Check who is named as payee in the contract, whether your current accounts already separate publishing cashflow, and the real local admin and compliance costs. Then weigh those costs against your deal size and risk profile, and confirm the structure with qualified legal or tax counsel before changing the contracting party.

What is the most practical way to manage a large advance?

Treat the advance as business capital, not immediate long-term income security. Check your tranche schedule, often tied to signing, manuscript delivery, publication, and sometimes paperback publication, and review your agency agreement since commission is often 15% but must be verified in your documents. Reserve tax cash first, then spread the remaining funds across the months you need to cover so a delayed tranche does not create a cash crunch. | Royalty basis | What to check in your contract/statement | Payout visibility | Audit risk | | --- | --- | --- | --- | | Retail or list price | Whether your royalty percent applies to the stated retail/list price | Verify against contract terms and statement lines | Depends on statement detail | | Net sale price | Whether your royalty percent applies to the publisher’s net sale price | Verify against contract terms and statement lines | Depends on statement detail |

How do you calculate what a royalty statement actually means for your earnings?

Royalties depend on the contract base, such as retail/list price or net sale price. For each line, confirm the units or sales basis, the rate applied, and any recoup or advance balance shown. Then recalculate line by line and raise written queries with the period, page or line, and the exact contract clause you are applying.

Do you still pay tax on an advance if the book never earns out?

You usually keep upfront advance money even if sales underperform, but tax treatment depends on local rules and timing. Check payment records, contract language showing the advance structure, and the returns filed for each year you received a tranche. Do not assume later low sales automatically change earlier tax treatment. Confirm treatment with a qualified tax professional.

How does an advance affect you if you live outside your publisher’s country?

Cross-border tax treatment can vary by country and should be confirmed with a qualified professional in the relevant jurisdictions. Check your contract and payment records, then get country-specific advice before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cfo.gov/assets/files/Final%202%20CFR%20Guidance%20-%...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/source-o...trusted

- sba.gov/blog/5-ways-separate-your-personal-business-...trusted

- sba.gov/business-guide/launch-your-business/choose-b...trusted

- sec.gov/Archives/edgar/data/2013100/0001493152240205...trusted

- literatureandlatte.com/blog/publishing-101-understanding-book-advan...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

How to Get a Literary Agent Through a Structured Query Process

To get a literary agent, start by changing the job you think you are doing. You are not asking for permission. You are choosing a business partner for a process that is exciting, subjective, slow, and often emotionally hard, with rejection, long response times, and silence as part of the reality. That shift can lead to better fit and clearer decisions under uncertainty.