Quick Answer

Confirm your accounting method and prior return treatment first. For most cash-basis unpaid service invoices, the claim is generally no; accrual treatment only opens the door to further checks. Then test whether the item is a bona fide debt, whether collection efforts are documented, and whether recovery is still realistic. End with a one-page claim, non-claim, or escalate memo so your file can be reviewed without guesswork.

You can know your bad-debt position before tax season panic#

Start with one clear call: how your records and prior return treated this income. Do not start with "Can I deduct this?" until that part is clear. You may not need a complex strategy here. You need a consistent, documented position you can explain if questioned.

Make one clean call before you do anything else#

Before you analyze any unpaid invoice, confirm how your books and prior filing treated this type of income. If you cannot answer that from your records, stop there first, then use your paper trail to answer four basics:

- how the income was recorded in bookkeeping

- whether you tracked receivables or mostly recorded cash received

- whether prior return treatment matched that pattern

- whether tools, bookkeepers, or treatment changed midyear

If those items conflict, treat that as a records problem to fix before you take any deduction position.

Use IRS material as a checkpoint, not a permission slip#

IRS publications are useful checkpoints, but they are not the last word. Publication 17 says it is not intended to replace the law or change its meaning. It also notes that a court decision may be more favorable to taxpayers than the IRS interpretation, so do not treat one publication as your final answer.

Publication 17 also tells you to check IRS.gov/Pub17 for future developments. Do that before you rely on publication language during filing season.

Publication 525 can help you frame the income-treatment question because it covers items like constructive receipt and advance payments. That context matters. You need to confirm what counted as income, and when, before you move into deduction analysis.

Follow a short sequence and know when to stop#

Keep the process short and deliberate:

- Confirm treatment from records and prior return pattern.

- Identify what the unpaid amount is in your file.

- Verify how that amount was treated for tax purposes.

- If records are mixed or incomplete, stop and escalate.

Those stop rules are part of the method, not a failure. If treatment changed during the year, your books do not match what was filed, or the unpaid amount is not clearly documented, fix the file first.

A one-page memo is enough: invoice, client, amount, dates, treatment, supporting documents, and your current call: claim, no claim, or escalate. That keeps this from turning into a last-minute guess.

For related context, see A Freelancer's Guide to the US-Australia Tax Treaty.

Make the accounting-method call first#

The first real decision is your accounting method. Before you spend time on fairness, invoice age, or collection history, confirm whether your filed pattern is cash basis or accrual accounting.

Use this quick screen:

| Question | cash-basis accounting | accrual accounting |

|---|---|---|

| How to read your file | Check whether prior return treatment follows cash received | Check whether prior return treatment recognizes receivables when earned |

| How unpaid invoices usually affect the first tax call | This file does not establish a bad-debt deduction for unpaid service invoices | Method status alone does not establish a bad-debt deduction |

| What to do next | Confirm limits in current IRS guidance before claiming anything | Continue to eligibility testing in primary IRS guidance before claiming anything |

Keep Topic No. 453 as an IRS checkpoint, but do not overstate it from memory. There is no quoted Topic No. 453 rule text here, so use it to confirm your lane and limits, not to make unsupported line-by-line claims.

Do not guess your method from software labels alone. Confirm it from prior return treatment before drafting anything on Schedule C (Form 1040). Compare the return pattern to bookkeeping inputs, check for method drift, and resolve conflicts first. Also verify current IRS updates at IRS.gov/ScheduleC. This article references the 2025 Instructions for Schedule C (Form 1040).

One more guardrail: secondary bookkeeping articles can help with terminology, but they are not controlling IRS authority. For example, the direct write-off entry of debit bad debt expense and credit accounts receivable is useful bookkeeping language. It is not, by itself, a tax-position foundation.

Related: A Freelancer's Guide to Donating to Charity (and the Tax Benefits).

Define the debt correctly before you try to deduct it#

Classification comes before deduction. Nonpayment is a fact pattern, not an automatic tax result.

| Debt lane | Usually fits when | In this context |

|---|---|---|

| Business bad debt | The debt came from credit extended in your trade or business (a profit-seeking activity). | An unpaid client invoice from your regular freelance work can fit this lane. |

| Nonbusiness bad debt | The debt is not related to your trade or business. | A personal loan to family or friends is the common example. |

Next, confirm it is a bona fide debt: a real loan with an expectation of repayment. If there was no clear repayment obligation when the money went out, the classification is weak.

Also separate "late" from "bad." Delayed payment alone is not enough. You need support that the debt is uncollectible and that you made documented collection efforts, such as letters, invoices, and phone calls.

Use Publication 334 as a framework, not a one-step verdict. It gives general guidance for self-employed taxpayers and emphasizes facts-and-circumstances analysis, so "my client did not pay me" is only the start of the review.

If you want a deeper dive, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Run a 10-minute eligibility check before you spend more time#

Treat this as triage. You are deciding whether to keep going or pause before you spend more effort on a bad-debt position.

Run these four checks in order:

- Method check

Confirm how you report income on filed returns, then make sure your books and return treatment are consistent. In this context, use your recent Schedule C (Form 1040) records and the accounting-method sections in Pub. 334 Chapter 2 as checkpoints.

- Trade-or-business check

Write down why the item is tied to an activity carried on for profit, and capture the facts and circumstances instead of assuming status.

- Scope check

Decide whether Pub. 334 is enough for your fact pattern or only a starting point. If the issue is cross-border or otherwise outside Pub. 334 coverage, treat it as out of scope for a Pub. 334-only read.

- Update check

Before you finalize any position, confirm there are no later developments at IRS.gov/Pub334.

Hard stops that save time. Pause and document why if either of these is true:

- You cannot clearly document the trade-or-business context for the item.

- Your fact pattern is outside Pub. 334 scope and you have not expanded your source set.

A quick scenario contrast.

| Scenario | What to verify first | Practical triage outcome |

|---|---|---|

| Unpaid service invoice | Whether the item is documented in your trade-or-business/Schedule C context | Continue only after records and context are clear |

| Unrepaid client loan | Whether the business context and transaction facts are documented clearly enough to classify the item | Pause and escalate if classification is unclear |

| Disputed invoice with partial payment | What is agreed, what is disputed, and whether Pub. 334 alone is enough for the issue | Treat it as a dispute fact pattern first; escalate if scope is unclear |

Create a one-page output before any claim decision. Before you decide anything, create a one-page continue / pause / escalate memo with:

- business context and accounting method

- item facts such as invoice versus advance or loan, dates, and parties

- four-check results

- conclusion of

continue,pause, orescalate - missing facts or sources that would change the answer

If your method and scope call is still fuzzy, use a practical checklist workflow before drafting your memo: Explore Gruv tools.

Decide when "unpaid" becomes "worthless"#

This is usually where the file either holds up or falls apart. Overdue does not equal worthless. Treat a debt as worthless only when your records show collection is no longer realistic. Until then, this is receivables management, not a deduction conclusion.

What "worthless" means in practice#

Use a practical test: could a third party read your file and see why collection is no longer realistic?

That call should rest on the same gates you already checked: bona fide debt, business connection, and basis in the debt. In this context, basis means the amount was already included in income.

Under the cash method, income is generally recognized only when paid, so an unpaid service invoice may not create basis. Accounting method is a gating checkpoint here, so align your books and return treatment before you debate worthlessness timing.

What counts as reasonable collection steps#

You need a documented sequence of collection effort and outcome.

- dated letters or invoices requesting payment

- documented follow-up contact, including phone calls

- records showing nonpayment despite those efforts

If collection is still active and recovery remains realistic, a worthlessness conclusion is usually premature.

Decide the year from evidence, not frustration#

Use a simple rule: if recovery is still realistic, keep it in your receivables process. If recovery is no longer realistic, move to the year-of-claim question.

Keep one more classification check in view. One nonbusiness bad-debt source requires 100% worthlessness, while one business bad-debt source discusses entirely or partially worthless debt. If classification is still unsettled, pause and document that before you lock the year.

Build the evidence pack before filing#

A workable claim file should stand on its own. The goal is a consistent record tied to the return you are filing, not a backfilled explanation after the fact.

Use Schedule C (Form 1040) as the organizing frame for Profit or Loss From Business, then map each document to a clear filing purpose.

What to include.

| Document | IRS-facing purpose | What it should show | Red flag if missing |

|---|---|---|---|

| Invoices, contracts, and receipts | Substantiate the deduction | Business purpose, amount, and date for each claimed expense | The claim depends on memory instead of records |

| Return-prep records aligned to your books | Keep records and filing treatment consistent | The amounts and categories used in your records and return prep | Records and return inputs conflict |

Current-year Schedule C instruction check | Verify guidance and line mapping before filing | Future Developments updates and current line references | Checklist still uses prior-year line mappings |

| Schedule placement check | Confirm the item belongs on the correct schedule | Whether the deduction is claimed on Schedule C or elsewhere (for example, Schedule 1-A) | Item is prepared for the wrong schedule |

Pre-filing checks. Before you file, do a short cleanup pass:

- Review current-year

Schedule Cinstructions, includingFuture Developments, before finalizing. - Re-check any checklist line references against the current form year.

- Do not reuse stale mappings. For example, 2025 instructions note an expense formerly from line 48 is now reported on line 27b.

- Confirm the item belongs on

Schedule Cat all, since some deductions are claimed onSchedule 1-A (Form 1040)instead.

Failure modes to catch early. Most preventable trouble shows up in one of three places:

- Weak substantiation: records are incomplete, scattered, or dependent on memory.

- Stale line mapping: checklist references were not refreshed for the current form year.

- Wrong schedule placement: an item prepared for

Schedule Cis actually claimed on another schedule.

A good final test is simple: if someone else can read the file and reach the same conclusion without calling you, the pack is probably ready.

For a step-by-step walkthrough, see A Guide to Vehicle Expense Deductions for Freelancers.

Keep jurisdiction lines clean if you work globally#

If you are filing a U.S. return, use IRS authority for that return and keep CRA logic out of it. This section is U.S.-anchored.

Schedule C (Form 1040) is for Profit or Loss From Business, and its instructions state that section references are to the Internal Revenue Code unless otherwise noted. Keep to that line. This article uses U.S. anchors, so non-U.S. readers should treat it as background rather than a filing rulebook. A common red flag is importing CRA reasoning into a U.S. position, or importing IRS Schedule C logic into a Canadian position.

Use one blunt rule: match the rule source to the return you are actually filing. If the question is about a U.S. return position, stay inside IRS materials. If the filing obligation is in Canada, stop before applying U.S. conclusions and check CRA guidance or local advice.

Before you finalize any U.S. position, re-open the current Schedule C instructions and check IRS.gov/ScheduleC for post-publication updates. The grounding here points to the 2025 instructions, so that check matters if you are filing later or relying on older prep notes.

The common failure mode is document drift, not bad intent: notes in one jurisdiction's terms, books labeled for another, and a return position that quietly blends both. If you file in more than one country, keep separate jurisdiction-specific notes and label each conclusion with the authority you used.

This pairs well with our guide on A Freelancer's Guide to the US-Canada Tax Treaty.

Avoid the mistakes that trigger preventable risk#

Most preventable risk starts the same way: filing from incomplete facts or mixing separate compliance topics into one conclusion.

| Red flag | Article note |

|---|---|

| Assuming filing Form 8938 replaces FBAR (FinCEN Form 114) | Filing Form 8938 does not replace FBAR; keep them separate in your notes and verify each one against its own rules |

| Applying one Form 8938 threshold to everyone | Thresholds vary by taxpayer context and can be higher for joint filers or taxpayers residing abroad |

| Forgetting Form 8938 timing | Form 8938 is attached to your annual return and filed by that return's due date, including extensions |

| Reporting every foreign-linked account on Form 8938 without checking exclusions | Check exclusions, including accounts maintained by a U.S. payer |

| Assuming Form 8938 is still required when no income tax return is required | If you are not required to file an income tax return for the year, you do not need to file Form 8938 |

Do not let labels outrun your facts. If your documentation is thin or your timeline is unclear, treat the issue as unresolved and avoid forcing a filing position too early.

Use a simple file-quality test: could a third party follow what happened from your records alone? If not, pause and tighten the record before you classify anything on a return.

Treat broad search-result advice as incomplete. Generic claims that collapse foreign-asset reporting, foreign-account reporting, and debt classification into one answer are not decision-ready on their own. If the guidance does not separate Form 8938 and FBAR (FinCEN Form 114), it is missing context you need for a filing decision.

Keep Form 8938 and FBAR separate from debt classification. Keep them separate in your notes and verify each one against its own rules.

Red flags to stop on:

- Assuming filing

Form 8938replacesFBAR (FinCEN Form 114). - Applying one

Form 8938threshold to everyone, even though thresholds vary by taxpayer context and can be higher for joint filers or taxpayers residing abroad. - Forgetting

Form 8938is attached to your annual return and follows that return's due date, including extensions. - Reporting every foreign-linked account on

Form 8938without checking exclusions, including accounts maintained by a U.S. payer. - Assuming

Form 8938is still required when no income tax return is required for the year.

If debt classification, timing, or jurisdiction is ambiguous, involve a qualified tax professional before filing, especially when Form 8938 and FBAR are also in play.

You might also find this useful: A Guide to the Qualified Business Income (QBI) Deduction for Freelancers.

Know where this issue touches your broader compliance stack#

A bad-debt position does not live on its own. Once you classify an invoice, the rest of your file should tell the same factual story: books, return posture, and any separate foreign-asset reporting.

Keep one factual record across filings. A write-off is not just one return line. It sits inside your invoices, ledger, bank activity, and collection notes, and for some freelancers, foreign-asset or foreign-account reporting. If those records conflict, the file gets harder to defend.

Before filing, run a quick consistency check:

- Invoice treatment in your books matches the amounts and dates used elsewhere.

- Client names, balances, and timing are consistent across supporting records.

- Your timeline is not contradicted by business records, addresses, or account activity without a clear explanation in your file.

Fixing one item while leaving related records inconsistent can create avoidable risk. That does not automatically create a Form 8938 or FBAR issue.

Keep the boundaries clear. This section is about invoice treatment, not a substitute for offshore-account, FATCA-related, or state-filing analysis.

Form 8938 is a separate IRS form for specified foreign financial assets when applicable thresholds are met. IRS materials cite aggregate value exceeding $50,000 as a base trigger for certain U.S. taxpayers. Filing Form 8938 does not relieve you of a separate FBAR filing when FBAR is otherwise required.

Two filing points matter:

- Form 8938 is attached to your annual return and filed by that return's due date, including extensions.

- If you are not required to file an income tax return for the year, you do not need to file Form 8938, even if foreign assets exceed an otherwise applicable threshold.

State questions may be separate. A federal conclusion on unpaid invoices does not by itself resolve state filing obligations. For that, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. If the broader issue is recurring write-downs from weak pricing, payment terms, or collections, go next to The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Use the order that prevents contradictions. A practical way to reduce contradictions is to work in order:

- Finalize invoice treatment in your books first, including documentation for how you treated collectibility and timing.

- Confirm your return posture next, including whether an income tax return is required.

- Then review Form 8938 and FBAR separately under their own rules.

Use Form 8938's own checkpoint as a cross-check: it asks whether any foreign assets were acquired or sold during the tax year. If your records do not align across these steps, stop and resolve the mismatch before filing.

Related reading: A Freelancer's Guide to the US-UK Tax Treaty.

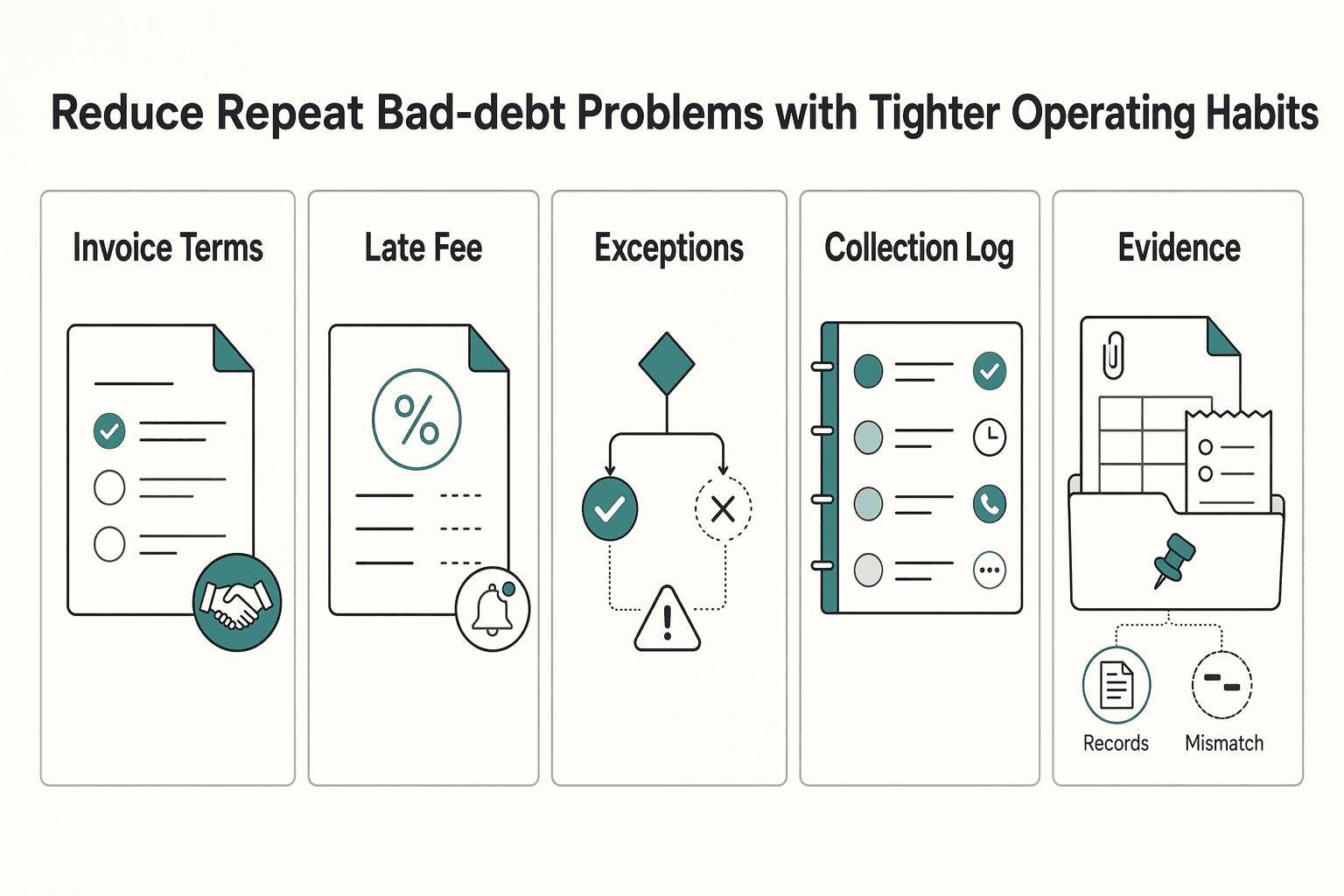

Reduce repeat bad-debt problems with tighter operating habits#

To reduce repeat bad-debt problems, tighten your process before invoices go late. Small process misses can turn into larger, costly problems over time. Shortcuts can feel faster up front, but they can raise downstream costs and slow execution.

| Workflow step | What to do |

|---|---|

| Invoice terms | Confirm clear payment terms and due date on the invoice |

| Late-fee language | Include clear late-fee language if you intend to apply it |

| Escalation timing | Set escalation timing in advance, such as final notice and next internal step |

| Collection log | Log reminders, replies, promises, disputes, and partial payments |

| Evidence archive | Archive evidence in one place: agreement, invoice, delivery or work proof, messages, payment history, final status |

Set terms once, then use them consistently. Exceptions can create avoidable risk. Before making one, pause and pressure-test it: is it necessary, and can you afford the downside if payment drifts or fails?

Use one standard set of terms across your agreement and invoice so timing, dispute handling, and late-fee language stay aligned.

Run a simple, repeatable collection workflow. The goal is consistency, not complexity. Use a checklist you can follow every time:

- confirm clear payment terms and due date on the invoice

- include clear late-fee language if you intend to apply it

- set escalation timing in advance, such as final notice and next internal step

- log reminders, replies, promises, disputes, and partial payments

- archive evidence in one place: agreement, invoice, delivery or work proof, messages, payment history, final status

Keep records clean for year-end decisions. Clean records do not create tax eligibility, but they can make year-end decisions easier to explain and defend. Specific U.S. bad-debt tax treatment still needs separate verification.

If you use Gruv, audit-ready invoice and payment records can help you keep that trail organized where supported. Do not treat software records as a guarantee of any tax outcome. Consistent, dated records are a practical way to show your collection effort in plain language.

The practical next step is a documented yes-or-no decision#

At the end of this review, each unpaid invoice can land in one of three buckets: claim candidate, non-claim, or escalate. The goal is a file someone else can follow without guesswork, not a creative argument.

| Memo field | What to record |

|---|---|

| Invoice details | Invoice number, client, issue date, due date, and amount |

| Accounting context | Your accounting context for the decision |

| Item type | What the item is: unpaid invoice, dispute, or another arrangement |

| Books/records | Whether the amount appears in your books/records |

| Evidence on hand | Contract, invoice, payment terms, statements, reminders, call log, and supporting schedules |

| Final call | Claim candidate, non-claim, or escalate |

| Reason | One-sentence reason for the call |

Use a short memo per invoice. If you want the same list as a checklist, record these fields for each invoice:

- Invoice number, client, issue date, due date, and amount

- Your accounting context for the decision

- What the item is: unpaid invoice, dispute, or another arrangement

- Whether the amount appears in your books/records

- Evidence on hand: contract, invoice, payment terms, statements, reminders, call log, and supporting schedules

- Final call: claim candidate, non-claim, or escalate

- One-sentence reason for the call

Also keep bookkeeping and tax analysis separate. Bad debt expense is an accounting entry for receivables you do not expect to collect, and that entry alone may not be enough to support a tax claim.

Escalate borderline files early. If the documents are thin, terms are unclear, or the agreement and invoice do not line up, escalate early instead of forcing a weak position. A simple enforceability check helps: payment terms should be stated in both the service agreement and the invoice.

Build a plain, review-ready evidence file. Keep one organized digital folder per invoice with contracts, invoices, statements, logs, and supporting schedules. A common benchmark in the provided guidance is keeping records for six years after the relevant tax year, but confirm the retention rule for your jurisdiction. If anything is mixed-use, include only the business portion in your claim file. When support is weak, a documented non-claim is usually safer than forcing a weak claim.

Need the full breakdown? Read A Freelancer's Guide to the US-Germany Tax Treaty.

If your facts are borderline across jurisdictions, get a compliance-workflow sanity check before filing: Contact Gruv.

Frequently Asked Questions

Can freelancers on cash-basis accounting deduct unpaid client invoices?

Usually no. The guidance provided here says cash-basis taxpayers generally do not get this bad-debt tax break because the unpaid amount was not previously reported as income. Start by checking whether the amount was ever included in income at all.

When can an unpaid invoice be treated as a worthless debt instead of just late?

Late is not enough. In the provided guidance, being unpaid alone is not enough; the debt must be 100% worthless before it can be deducted.

What is the difference between business bad debt and nonbusiness bad debt for freelancers?

Nonbusiness bad debt is a bona fide loan with a real expectation of repayment, reported on Form 8949. Do not treat business bad debt and nonbusiness bad debt as interchangeable. If your fact pattern is an unpaid client invoice, do not relabel it as a loan unless your documents actually support that structure.

What proof should I keep before claiming a bad debt deduction?

Keep evidence of both the debt and your collection attempts. The source-backed examples here are letters, invoices, and phone-call records. If you are claiming a loan-based debt, keep written repayment terms, such as a promissory note, that show repayment intent.

Do U.S. IRS bad-debt rules apply if I live abroad or also file in another country?

The sources here support U.S. bad-debt concepts only. They do not establish how a non-U.S. return treats the same unpaid amount. If you file in more than one country, verify each country's rules separately.

If I am accrual-basis, does that automatically mean I can deduct every unpaid invoice?

No. Accrual basis is only one gate. It addresses whether the amount was previously included in income. You still need a defensible worthless-debt position and documented collection efforts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ecfr.gov/current/title-7/subtitle-A/part-1trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- hed.nm.gov/uploads/documents/CCNS_Catalog_2025.12.19.pdftrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/forms-pubs/about-form-8938trusted

- law.lis.virginia.gov/vacodefull/title22.1trusted

- law.uh.edu/blakely/story-telling/Speaking%20for%20Victi...trusted

- asja.org/no-tax-break-if-client-stiffs-youexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.