Quick Answer

For 2026 launches and updates, submit only after your build, metadata, privacy disclosures, and reviewer notes all match the shipped app. Keep the app record in Prepare for Submission until your evidence pack is complete, use a pass/fail release gate, hand off a full review package, and separate sales, proceeds, and payments after launch for clean bookkeeping and tax-ready records.

Phase 1: The Pre-Flight Compliance Audit#

For an iOS App Store submission, your first job is not packaging the build. It is spotting the mismatches that create review friction before you submit. Apple review can include manual checks for first publication and updates, and missing metadata, thin reviewer instructions, and privacy gaps are common reasons things slow down or get rejected.

A practical checkpoint is to keep the app record in Prepare for Submission until your evidence pack is complete. Move it to Ready for Review only when the required metadata is in place and you actually intend to submit. That sounds obvious, but it is where teams get sloppy. They upload a build, then realize the privacy text, reviewer notes, or account-access details do not match the version they just froze.

Pick your enrollment path before you pay#

Do not treat enrollment as paperwork to sort out later. This article does not establish exact Apple enrollment differences between Individual and Organization for seller name, liability, or admin setup, so use this as a verification table, not a set of assumptions. Work through it before you pay the $99 annual fee.

| Decision point | If you enroll as Individual | If you enroll as Organization |

|---|---|---|

| Seller display name | Verify what name Apple will display on the listing and whether you are comfortable publishing under it. | Verify what name Apple will display on the listing and whether it matches your brand records. |

| Verification burden | Confirm current identity checks and required documents. | Confirm current entity checks, required documents, and who must provide them. |

| Liability posture | Check with your own legal advisor how this setup maps to personal risk. | Check with your own legal advisor how this setup maps to entity risk. |

| Payout and admin workflow | Verify who controls banking, tax, and account access if you are the only operator today. | Verify who needs access to payouts, finance records, and release permissions as the team grows. |

If you are unsure, do not guess. Verify the enrollment path in current Apple enrollment guidance before you proceed.

Document privacy as behavior, not boilerplate#

Privacy review is easier when you describe what the app actually does, not what a template policy says. Before review, write down four things for every user-facing feature and every SDK: what data is touched, why it is processed, how a user can ask questions or request action, and where that same behavior is disclosed.

| Privacy item | Applies to | Related disclosure |

|---|---|---|

| What data is touched | Every user-facing feature and every SDK | Where that same behavior is disclosed |

| Why it is processed | Every user-facing feature and every SDK | Where that same behavior is disclosed |

| How a user can ask questions or request action | Every user-facing feature and every SDK | Where that same behavior is disclosed |

| Where that same behavior is disclosed | Every user-facing feature and every SDK | Policy text, in-app prompts, onboarding copy, and App Store Connect disclosures should all describe the same reality |

The goal is consistency. Your policy text, in-app prompts, onboarding copy, and App Store Connect disclosures should all describe the same reality. A simple working sheet is enough if it has these columns:

- Feature or SDK

- Data involved

- Purpose

- Where collected or accessed

- Stored or transmitted where

- Internal retention/deletion notes (if any)

- Policy section

- App Store disclosure check

That last column matters most. A common failure mode is drift. The app changed, the SDK changed, or a new event was added, but the App Store disclosures did not.

Treat monetization and tax as records setup, not a later cleanup job#

These sources do not establish jurisdiction-specific tax rules. Treat this as a records setup checkpoint, not tax advice. Set up the payout destination, decide who reconciles deposits, and create a bookkeeping trail that ties each app sale or subscription report back to your business records. Where local tax treatment, withholding, or indirect tax rules apply, verify them for your jurisdiction before launch.

One last operator note belongs here, not at the end of the release checklist. Prepare reviewer notes while you are still auditing. If sign-in is required, include test-account guidance in the review comment. That small step cuts avoidable back and forth, and once the app moves to Waiting for Review, screenshot and app preview edits are restricted. Related: A Guide to App Store Optimization (ASO) for Mobile Apps.

Phase 2: The Predictable Submission Engine#

This phase is where you make the submission process repeatable instead of hopeful. Treat release as a pass/fail process: one package that covers build quality, metadata accuracy, and reviewer handoff. Delays cost momentum, so your goal is to remove reviewer confusion before upload.

Use one rule: if a reviewer could be blocked, surprised, or forced to guess, do not submit yet.

Use a pass/fail gate before upload#

Run this gate on every release candidate:

| Review risk area | Verify before upload | Include in Review Notes |

|---|---|---|

| Performance and completeness | Test core flows on physical devices, remove dead ends (placeholder text, unfinished screens), and confirm required sign-in or purchase paths are reachable | Short start-to-finish test path and where the reviewer should begin |

| Privacy consistency | Make sure in-app prompts, policy language, store privacy disclosures, and actual app/SDK behavior describe the same thing | Note which permission prompts appear in review and when they appear |

| Minimum functionality | Confirm the app delivers a complete user outcome without reviewer guesswork | One sentence on the main user outcome and fastest path to see it |

| Spam/clone risk | Check branding, copy, layout, and feature scope for obvious reskin/template signals | If similar to another app you own, explain the distinct audience or use case |

Most submission friction here is mismatch, not catastrophe: the metadata or assets describe one experience, while the uploaded build behaves differently.

Make the product page match the shipped flow#

Your listing should match what a reviewer can actually open in this build. Align screenshots, preview video, and description to real in-app paths. If key screens require login, permissions, hardware, or accessories, make that explicit and make the review path reach those screens cleanly.

Hand off a review package, not a loose note#

Prepare one review package for each submission:

| Package item | What it covers | Timing |

|---|---|---|

| Demo account or test credentials | With the right role | For each submission |

| Role-based test path | From app launch to primary value | For each submission |

| Feature flags | Active in this build, plus intentionally disabled areas | For each submission |

| Hardware/accessory/environment setup | Steps if needed | For each submission |

| Escalation contact | Can respond during review | During review |

| Apple review fields/attachments | Verify current fields/attachments in your account | Before release |

| Update-review behavior | Verify current behavior for your app type/account | Before release |

Keep it in one place so whoever responds during review is working from the same build context the reviewer sees.

Use TestFlight as your launch-readiness rehearsal. Collect feedback in a structured format (device, steps, expected result, actual result, risk area), triage by review risk first, then confirm fixes before final submission.

Do not assume beta approval removes later review work; review steps can repeat for new builds, so confirm the current path in your account. If you want a deeper business-side planning view, read Value-Based Pricing: A Freelancer's Guide.

Phase 3: The Missing Chapter: Post-Launch Revenue & Global Operations#

Approval is the handoff, not the finish line. After launch, the work shifts from submission tasks to operating discipline: cash tracking, tax-ready records, and update cadence.

Separate performance reporting from cash movement#

Treat Sales, Proceeds, and Payments as three different bookkeeping buckets, then map each one to the current labels in your App Store Connect account.

| Bucket you track | How to use it operationally | Cash-flow meaning | Common mistake |

|---|---|---|---|

| Sales | Track customer demand and product performance | Not bank cash | Recording it as cash received in the same cycle |

| Proceeds | Track platform-calculated net amounts before/around payout | Intermediate value between activity and deposit | Assuming it must equal the bank deposit exactly |

| Payments | Reconcile to actual payout records and bank receipts | Cash received | Matching to the wrong reporting period |

Use one rule consistently: performance metrics are not the same as liquidity. Reconcile each payout to its statement and bank receipt, not to dashboard totals alone.

Lock down Agreements, Tax, and Banking before volume grows#

Inside Agreements, Tax, and Banking, set this up so monthly close is repeatable:

- Confirm account ownership aligns with your legal operating entity.

- Confirm which payout currencies your bank account can receive.

- Check for transfer/intermediary fee risk that can reduce landed deposits.

- Use fixed bookkeeping categories for sales activity, platform fees, refunds/adjustments, and cash received.

Maintain the same records every cycle:

- Payout statements

- Platform fee detail

- Refund/adjustment detail

- Bank receipts

- Tax-supporting exports used for filings

Treat cross-border tax as an ongoing records workflow#

If you are a U.S. taxpayer abroad, validate FEIE eligibility early and keep validating it. The IRS defines foreign-earned income as compensation for personal services rendered by you, and FEIE-related treatment requires your tax home to be in a foreign country.

| Topic | Rule or figure | Note |

|---|---|---|

| Foreign-earned income | Compensation for personal services rendered by you | FEIE-related treatment requires your tax home to be in a foreign country |

| Tax home | In a foreign country | Required for FEIE-related treatment |

| Physical presence test | 330 full days in 12 consecutive months | Those days do not need to be consecutive |

| Full day | 24 consecutive hours (midnight to midnight) | If you do not reach 330 full days, that test fails |

| 2025 FEIE maximum | $130,000 | Per qualifying person |

| 2026 FEIE maximum | $132,900 | Per qualifying person |

One qualification path is the physical presence test: 330 full days in 12 consecutive months. Those days do not need to be consecutive, but a full day is 24 consecutive hours (midnight to midnight). If you do not reach 330 full days, that test fails, including common disruption scenarios. The IRS also publishes an annual Revenue Procedure for countries with adverse-condition time waivers, so review that each year if your location changed.

For reporting, timing discipline matters: income is generally applied to the year the work is performed, even if payment arrives later, and you still file a U.S. return reporting income when claiming FEIE. The FEIE maximum is $130,000 (2025) and $132,900 (2026) per qualifying person. If you claim a foreign housing exclusion, it reduces the foreign earned income available for FEIE. FBAR may apply if account balances cross the current reporting threshold; verify that threshold from official IRS/FinCEN guidance before using it in a filing workflow.

Keep a post-launch operating cadence#

Run updates as an operations control, not just a product habit. Write release notes that clearly call out fixes and any changes affecting access, permissions, or billing. Monitor support and refund signals for repeat issues, then prioritize updates that protect revenue continuity, keep disclosures aligned with the live build, and preserve audit-ready records.

For a step-by-step walkthrough, see How to Get Your App Featured on the App Store.

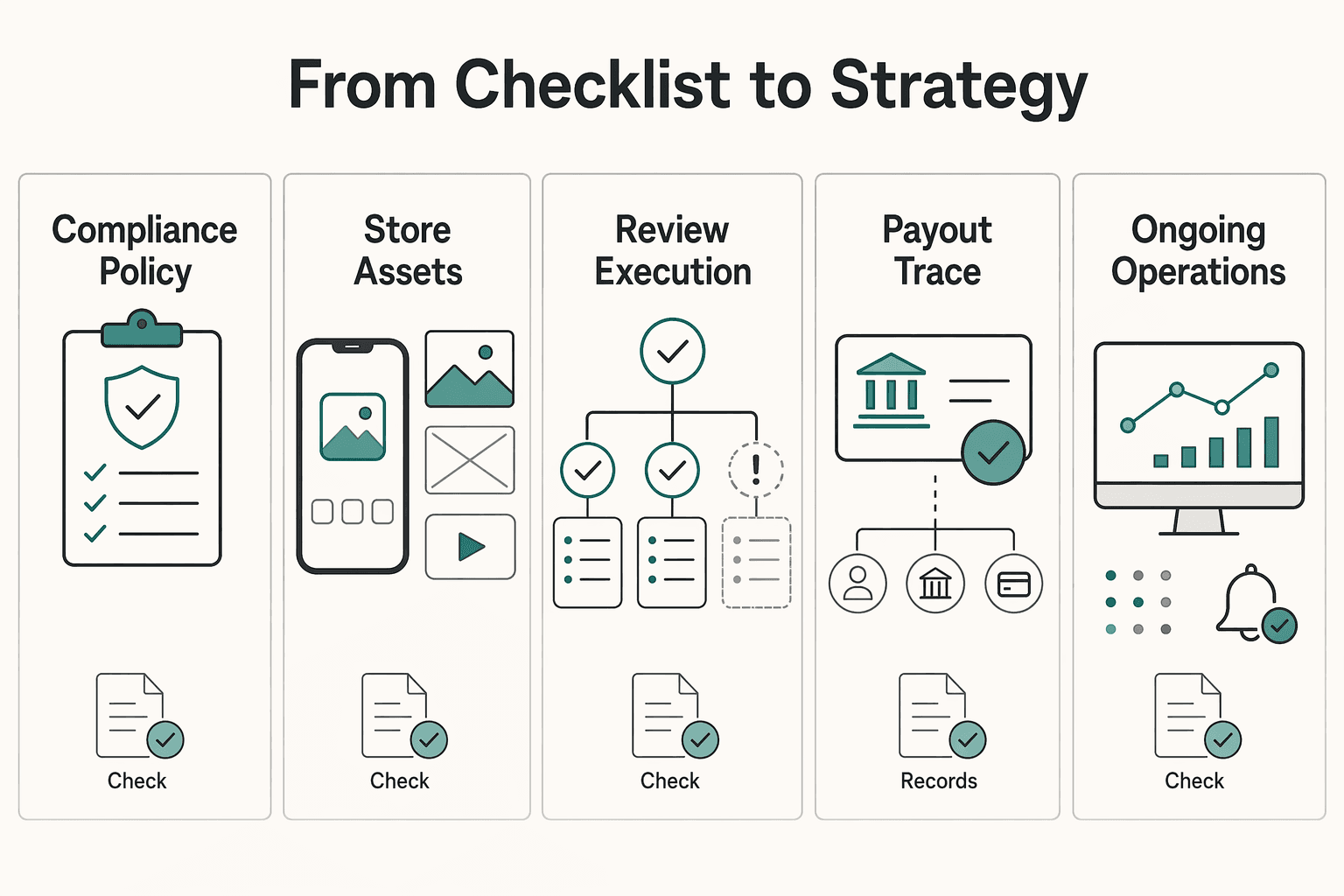

From Checklist to Strategy#

Predictable App Store submission comes from systems, not last-minute fixes. Treat this as an operating sequence: run your phase checks, verify current Apple requirements, and execute in order.

| Lane | Last-minute behavior | Strategic behavior |

|---|---|---|

| Compliance | You check policy after the build is done, then patch issues under time pressure. | You use the App Review Guidelines early and review against all five sections: Safety, Performance, Business, Design, and Legal. You keep your data map, SDK list, and policy version current so App Privacy answers can be verified before submission. |

| Store assets | You pull screenshots from an old build and edit copy in App Store Connect at the end. | You lock assets to the release candidate and verify the full set Apple calls out: app name, icon, description, screenshots, app previews, and keywords. You check for metadata drift before you submit. |

| Review execution | You submit once, wait, and rebuild context from memory if questions come back. | You test the release candidate on physical devices and/or in TestFlight, then submit with a dated release pack (final checklist, screenshots, and change notes). If a submission is already in progress, you still check whether additional items can be submitted so work does not stall. |

| Post-launch finance | You treat approval as the end and leave release evidence scattered. | You keep versioned submission records so reporting, bookkeeping, and handoffs can trace what shipped and when. |

| Ongoing operations | You launch once and improvise every update. | You run release discipline as a repeatable process because apps are expected to keep improving to remain on the App Store. For 2026 planning, verify the current baseline, including the April 28, 2026 requirement to upload with the iOS & iPadOS 26 SDK or later, and recheck channel choices where alternative distribution paths apply. |

Next step: run the phase checks now, confirm current requirements in App Store Connect and the App Review Guidelines, and execute your release in sequence. You might also find this useful: A Guide to Google Play Store Submission for Android. For your broader operating stack, use Browse Gruv tools or Talk to Gruv. ---

Frequently Asked Questions

What are the most common reasons for rejection?

The article does not provide a verified Apple rejection list. It says to verify current Apple requirements and focus on build quality, metadata alignment, and privacy alignment, with evidence like test checklists, approved screenshots, SDK inventory, and privacy policy versions.

Do you need a lawyer to write a privacy policy?

The article does not provide verified legal standards for app privacy policies. Use counsel based on your risk profile and jurisdictions, and make sure your policy matches actual app and SDK behavior.

How long does the review process take?

No verified App Store review-time expectation is provided here. Check current platform guidance before announcing dates, and keep buffer in your launch plan.

How should you handle App Store payouts as an expat?

Separate sales, proceeds, and actual cash payments in your books, and send payouts to an account that matches your operating entity. If you are a U.S. taxpayer abroad, FEIE-related benefits generally require foreign earned income, a foreign tax home, and qualifying status under IRS rules, and you still file a U.S. return reporting the income, typically using Form 2555. If you use the physical presence test, track 330 full days in 12 consecutive months, with a full day defined as 24 consecutive hours from midnight to midnight. Keep monthly records such as payout statements, bank receipts, travel logs, and tax workpapers, and verify the current FBAR reporting threshold and deadline separately.

What is the difference between a Bundle ID and an SKU?

The article does not include verified Apple definitions for Bundle ID versus SKU. Confirm current definitions and usage directly in Apple Developer and App Store Connect documentation before submission.

Can you change your app name or screenshots after approval?

The article does not verify post-approval rules for app-name or screenshot changes. Re-check current Apple guidance before each release.

What is IDFA, and do you need to use it?

The article does not include verified ATT or IDFA policy details. Confirm current Apple requirements and make sure your declarations match actual code and SDK behavior before submission.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ec.europa.eu/competition/antitrust/cases1/202419/AT_40437...trusted

- fda.gov/media/189509/downloadtrusted

- in.nau.edu/wp-content/uploads/sites/139/2025/09/Complet...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- nrm.dfg.ca.gov/FileHandler.ashxtrusted

- sunyacc.edu/continuing-education-catalogtrusted

- developer.apple.com/app-store/submittingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Run App Store Optimization Like an Operator for Mobile Apps

ASO works when you treat it like a recurring operating practice, not a burst of edits when installs dip. If you are working solo or with one helper, keep it to four controls you can actually manage: metadata, creative, experimentation, and risk. Think of this as a practical four-part ASO stack with a simple report card for execution.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.