Quick Answer

Yes, classify the purchase before you book it. For amortization for freelance business, confirm the item is an acquired intangible tied to your trade or business, then choose treatment from the governing rule instead of invoice wording. Section 197 may apply to acquired intangibles, while startup costs under IRC §195 and some software items can follow different paths. Once treatment is set, report through Form 4562 and keep contract, payment, and date evidence linked to the filed return.

From 'Expense' to 'Asset': The Strategic Mindset Shift for the Business-of-One#

Before you book a meaningful nonphysical purchase, decide whether it is a current-year expense or an asset that may need capitalization and amortization. This section is only an orientation step; use the later checklist and framework sections to confirm what qualifies and how to report it.

Getting that call right early makes everything downstream cleaner. If you book a large cost all at once when it should be recovered over time, your results can look uneven across periods. When treatment matches the facts, your workpapers are easier to trace to the return.

The decision lens to use before you buy#

Before you classify anything, run three checks. If one of those answers is weak, pause before you book the transaction.

| Check | Question |

|---|---|

| Business purpose | Can you explain, in one sentence, how the purchase connects to your trade or business? |

| Expected useful life | Are you paying for something consumed now, or something with value beyond the current tax year? |

| Recordkeeping readiness | Can you keep the documentation to prove your position: receipts, bills, payment evidence, and supporting records? |

Those checks sound basic, but they do most of the sorting work.

Business purpose. If you cannot explain, in one sentence, how the purchase connects to your trade or business, pause.

Expected useful life. Ask whether you are paying for something consumed now or something with value beyond the current tax year. Intangible property is nonphysical property with value, but not every nonphysical purchase automatically qualifies for amortization treatment.

Recordkeeping readiness. Make sure you can keep the documents that prove your position: receipts, bills, payment evidence, and supporting records.

Expense now versus asset and amortize#

The tradeoff is straightforward: expensing can give you a current-year deduction, while capitalization and amortization spread deductions over time and usually require more support for classification and reporting.

| Decision path | Planning impact | Documentation burden | Audit defensibility |

|---|---|---|---|

| Expense-now treatment | Current-year deduction when facts support current expense treatment | Documentary evidence is still required | Strong when business purpose and current-period treatment are clear in your records |

| Asset-and-amortize treatment | Deductions spread over time | Documentary evidence plus support for classification, timing, and recovery method | Strong when treatment matches facts and your workpapers clearly tie through to the return |

Audit confidence comes from matching treatment to facts and proving it. It does not come from picking the label that sounds more conservative.

Where the risk actually sits#

The real risk is usually weak substantiation and deductions you cannot defend. Recordkeeping obligations last as long as needed to support what you reported, so longer recovery periods can mean longer support windows.

Use one guardrail here. Some intangibles are Section 197 intangibles, and those capitalized costs are generally amortized over 15 years when held in connection with your trade or business. But not every acquired intangible fits automatically, and transaction-structure limits can apply. If classification is unclear or the amount is material, involve a tax professional before you finalize the treatment. For adjacent context, see How to Handle Taxes for a Side Hustle.

What Can You Actually Amortize? A Modern Professional's Checklist#

Take a conservative view: amortization is only a possible treatment until the facts and documents support it. Before anything else, confirm the cost is tied to your business or self-employment activity and meets the baseline test of being ordinary and necessary. If that is not clear, stop there and classify it before you book any deduction.

A simple first filter helps. In common business-expense checklists, depreciation is listed separately, and software plus training/education are listed as their own categories. Use those categories as review cues, not automatic amortization outcomes.

| Item to review | Likely treatment | Why it qualifies (or does not) | Common mistake to avoid |

|---|---|---|---|

| Physical equipment (for example, laptop, camera, desk) | Separate depreciation review | Depreciation is listed as its own category in business-expense checklists | Running it through an amortization process by default |

| Software expense | Business-expense review first; amortization is not automatic | Software is a recognized expense category, but a category label alone does not settle amortization treatment | Assuming every software charge should be spread over time |

| Training or education expense | Business-expense review first | Training and education is a recognized expense category and still needs business-purpose support | Treating the category name as automatic proof of amortization |

| Any cost not clearly tied to business/self-employment income | Do not classify as deductible yet | Deduction scope here is tied to business/self-employment income | Booking a deduction before scope is clear |

| Any cost with weak or missing records | Pause and escalate classification | Proper documentation is critical for deductions | Trying to reconstruct support at filing time |

Re-verify the category cues above against current-year rules before filing.

Compliance-first file checklist (build this before booking)#

If a cost might need deeper classification review, build the file before you post the entry. That habit prevents most avoidable problems later.

| File item | What to keep |

|---|---|

| Proof of purchase and payment | Keep proof of purchase and payment. |

| Contract / invoice / receipt | Keep full contract, invoice, or receipt records. |

| Business-purpose memo | Keep a short business-purpose memo in plain language. |

| Business or self-employment tie | Keep notes showing how the cost ties to business or self-employment activity. |

| Unresolved classification questions | Keep notes on unresolved classification questions for professional review. |

If any item in that file is missing, treat the classification as open. If you cannot clearly explain what you paid for and why it is ordinary and necessary for the business, treat classification as unresolved.

When to escalate to a tax professional#

Escalate early when core checkpoints are unclear: business/self-employment scope, the ordinary-and-necessary test, or documentation quality. These cases are not automatically wrong, but they need case-specific review before filing.

If startup-versus-operating-cost classification is part of the issue, review How to Deduct Startup Costs for Your Freelance Business alongside professional tax review.

Your 3-Step Framework for Amortization#

For freelancers, run this in order: build the file, confirm treatment, then file from a clean paper trail.

Step 1 Build the asset file before you book the deduction#

Do this as soon as capitalization is on the table. Keep records in any system that clearly shows income and expenses. Your books should include a summary of business transactions, and your files should be organized by year and by income/expense type. Electronic records are acceptable if they meet the same requirements as paper records.

Save this minimum package for each asset:

- payee

- amount paid

- proof of payment

- date incurred

- the source document for the transaction (for example, invoice or contract)

- a books entry that ties to your transaction summary

Use consistent labels so the chain is obvious later, for example 2026_Intangible_Vendor_AssetName. Keep records that support income and deductions until the return's limitations period runs out.

Step 2 Confirm eligibility and period, then run straight-line#

The key judgment comes before the calculation. First confirm what the asset is, then confirm the recovery period, and only then calculate the deduction. Use this decision path:

- Confirm the item is an intangible asset, not a current expense and not a tangible asset that belongs in depreciation.

- Confirm what supports the recovery period.

- Apply straight-line only after steps 1 and 2 are documented.

For acquired Section 197 intangibles held in connection with your trade or business, the general rule is ratable amortization over 15 years beginning in the month acquired. Some acquired Section 197 intangibles may be non-amortizable in certain transactions, so check transaction facts before applying the rule. Do not apply Section 197 treatment automatically to self-created intangibles. If the facts fit startup expenditures under IRC §195, reclassify. That regime uses a separate deduction-plus-amortization structure ($5,000 immediate deduction, reduced when startup expenditures exceed $50,000, with the remainder over 180 months).

Use a neutral calculation template:

Annual amortization deduction (simplified) = capitalized basis / recovery period

Then apply the timing and reporting rules that govern the filed amount.

The control point is support for the recovery period from the Code and filing instructions, not a guessed timeline.

Step 3 Tie the deduction to the return and your file#

Once treatment is set, the last job is traceability. Claim amortization on Form 4562 and attach it to your return. On the 2025 form, Part VI line 42 covers amortization that begins in that tax year. Line 44 totals the amount and sends you to the instructions for where to report it next.

| Checkpoint | What the section says |

|---|---|

| Form 4562 | Claim amortization on Form 4562 and attach it to your return. |

| Part VI line 42 | On the 2025 form, this covers amortization that begins in that tax year. |

| Line 44 | This totals the amount and sends you to the instructions for where to report it next. |

| Books and support | Match Form 4562 amounts to your amortization schedule, asset file, and books. |

Operator checklist:

- match Form 4562 amounts to your amortization schedule and asset file

- match books to the same capitalized basis and current-year deduction

- verify current-year reporting details at IRS.gov/Form4562 and IRS.gov/ScheduleC before filing

Do not hard-code prior-year return lines. Keep one traceable chain: source document, payment proof, books entry, amortization schedule, Form 4562, return.

Safe default versus escalate#

When facts are unclear, the safe default is simple: do not force the deduction. Escalate for professional review if acquired-versus-self-created status is unclear, recovery-period support is unclear, the case may fall under IRC §195 startup-cost treatment, or the transaction may fall into a Section 197 non-amortizable exception.

Ready to operationalize your checklist instead of managing it in scattered notes? Start with Gruv's tools hub for practical tax and compliance workflows.

Amortization in Action: 3 Scenarios#

This is where documentation discipline matters most. Tax-amortization specifics are not confirmed in this section, so use a hold-and-escalate approach until treatment is verified.

| Asset type | Amortization approach | Documentation to retain | Common error to avoid |

|---|---|---|---|

| Multi-year software or platform license | Do not finalize treatment from labels alone. Keep classification open until documentation is sufficient. | Contract/terms, payment proof, and any additional supporting documentation needed for classification and business-purpose analysis | Booking a final treatment before documentation is complete |

| "Perpetual" or long-use creative license | Treat marketing language as unverified until enforceable terms are reviewed. | Full terms, proof of purchase, and records that support classification and business-purpose analysis | Assuming "perpetual" automatically answers classification |

| Purchased business rights or customer-related intangible | Route to a separate review path and escalate when classification is unclear. | Acquisition documents, transfer/payment records, and supporting business documentation | Mixing unclear items into routine processing without separate review |

You buy a multi-year software license#

Start with the underlying terms, not the invoice description. Keep the treatment unresolved until you have enough documentation to support the classification and business-purpose analysis.

Your outcome should be either "supported by documents" or "not yet supportable." If terms are unclear, pause and escalate.

You buy a "perpetual" creative asset library#

"Perpetual" in marketing copy is not a final determination. Use the actual terms and available records to decide whether the file is supportable, and avoid assigning a concrete tax method or timeline here.

Your outcome is a documented yes/no on documentation sufficiency, not a guess. If you only have a receipt and no full terms, keep treatment unresolved and escalate.

You acquire customer rights or another business intangible#

Treat this as a higher-control case from day one. Build the file with available agreements and transfer/payment evidence, then add any supporting documentation you need for classification and business-purpose analysis.

Keep this separate from routine items until classification is confirmed. If records are incomplete or the structure is hard to parse, hold treatment and escalate.

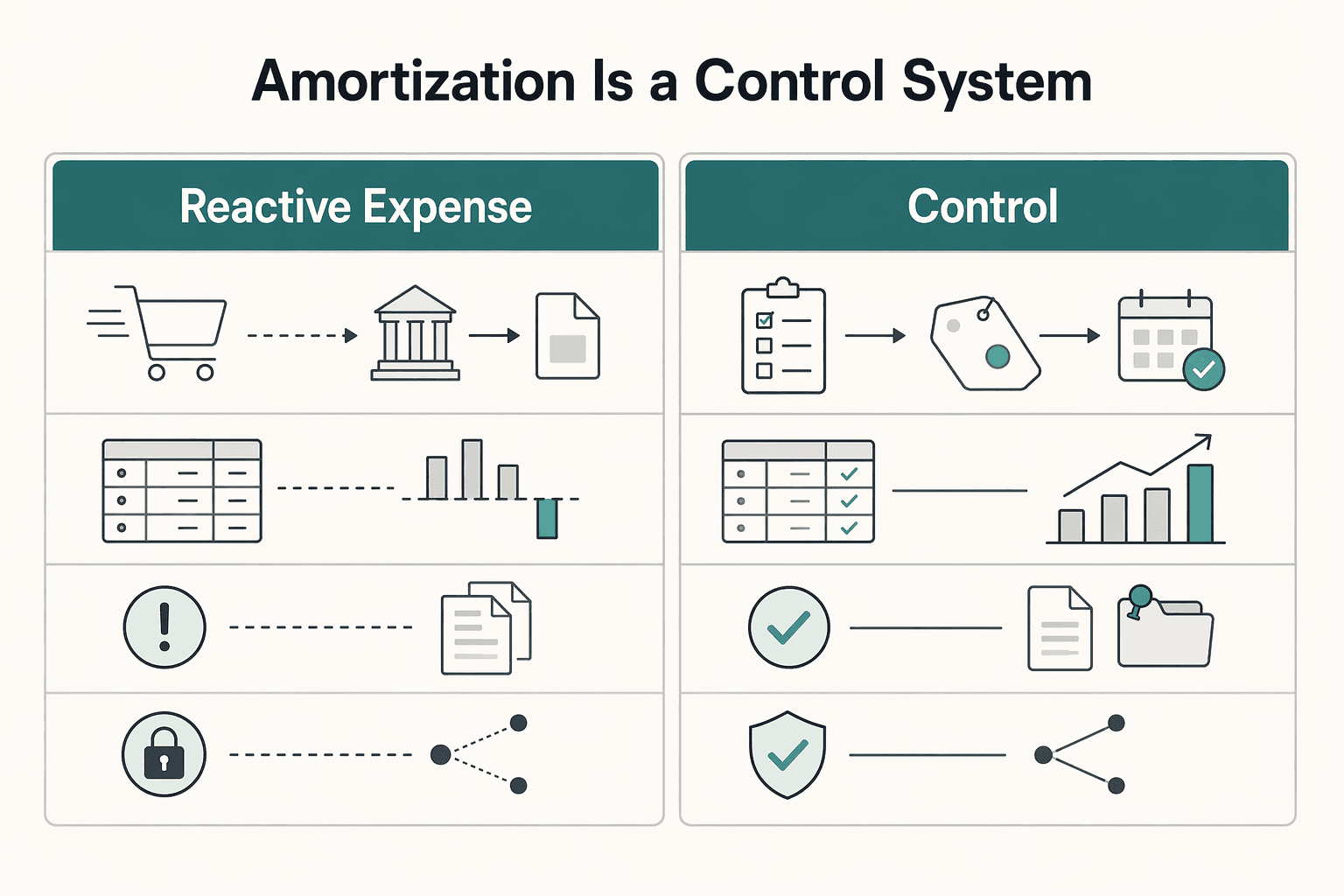

The Bottom Line: Amortization Is a Control System#

The practical point is simple: you stay in control when you classify a purchase before you book it, choose treatment based on facts, and keep support in one file. If you wait until after the cash leaves your account, you are reacting. If you classify first, you are deciding.

If you are self-employed, start with scope. IRS Publication 334 provides general federal tax guidance for self-employed persons (including sole proprietors and independent contractors) and statutory employees. A trade or business is generally an activity carried on to make a profit. If that scope fits, use Publication 551 (12/2025) to verify whether the item belongs in an intangible-asset review. Its Business Assets section includes Intangible Assets, with subtopics such as patents, copyrights, and franchises, trademarks, and trade names.

| Approach | Planning visibility | Documentation burden | Audit defensibility |

|---|---|---|---|

| Reactive expense handling | Low. You decide after payment, often from the invoice label alone. | Light at first, then harder when key facts are missing. | Weaker when ownership, transferred rights, or business purpose are unclear. |

| Controlled asset treatment | Higher. You classify before booking and see the likely deduction path earlier. | Moderate but predictable when you keep one asset file. | Stronger because treatment aligns to agreement terms, dates, and business use. |

Use this control checklist:

- Classify the purchase. Confirm whether it is physical or nonphysical, then decide whether it needs intangible-asset review.

- Choose treatment. Determine the tax treatment under the applicable rules based on the facts.

- Document support. Keep the contract or license, invoice, payment proof, transfer evidence, if any, and a short memo on business purpose and dates.

- Review annually. Check IRS.gov/Pub334 for post-publication developments before filing.

If facts are unclear or outside Publication 334's scope, consider getting professional tax advice. Escalate international business questions to IRS.gov/International, since Publication 334 points those topics there.

We covered this in detail in How to Choose a Tax Preparer for Your Freelance Business.

If you want invoicing, payout tracking, and an audit-ready record trail in one system where supported, talk to Gruv to confirm coverage for your setup.

Frequently Asked Questions

How do you tell whether a purchase belongs in amortization?

Use a quick filter before you book an item. Confirm it is a nonphysical business asset, then confirm whether it is an acquired intangible covered by Section 197 or an item that follows a different rule set. Acquired Section 197 intangibles are generally amortized ratably over 15 years starting in the acquisition month, while some excluded intangibles, including certain software, can follow separate rules. If the spend is education or startup related, test it under those specific rules first instead of forcing it into an amortization bucket. | Method | Usually applies to | Deduction timing | Typical reporting path | | --- | --- | --- | --- | | Amortization | Intangible property, including acquired Section 197 intangibles and some excluded intangibles with separate rules | Spread over a defined recovery period (for example, 15 years for Section 197, or 36 months for certain software under separate regulations) | Commonly claimed on Form 4562 and carried through the return | | Depreciation | Business or income-producing property subject to depreciation rules | Recovered over the asset’s tax life under depreciation rules | Commonly reported on Form 4562 | | Immediate expensing | Certain current business expenses, and some elected property costs | Deducted in the current year if the rules are met | Schedule C for qualifying current expenses; Form 4562 for Section 179 elections |

What kinds of freelancer purchases are most likely to qualify?

Start with acquired intangible rights, not self-created value. A purchased client list is a strong example because customer-list intangibles are explicitly named in Section 197. Software licenses and other separately acquired rights can qualify in some cases, but classify them only after reviewing the actual agreement and acquisition facts. For domains and long-term API rights, treat classification as contract-specific and verify before booking.

Can you amortize software licenses or long-term API rights?

Sometimes, but you should not classify from marketing copy or invoice labels alone. Certain software excluded from Section 197 may use a 36-month amortization period beginning on the first day of the month placed in service. For long-term API rights, verify the specific rights acquired, term, renewal, transfer, cancellation, and who legally holds the rights before you book treatment.

What about a purchased domain name or a purchased client list?

A purchased client list is explicitly named in Section 197. Domain treatment can vary with deal structure and with the rights actually transferred, so keep the purchase agreement, transfer proof, payment records, and any allocation memo together. If ownership or use did not meaningfully change, treat that as a review trigger.

Can you amortize role-relevant training or certification costs?

Do not default training to amortization. If education maintains or improves skills in your current work, or is required to keep your current status, it may be deductible. If it qualifies you for a new trade or business, it is not deductible. As a self-employed filer, you generally report qualifying education on Schedule C.

Are start-up costs handled the same way as other intangibles?

No. Section 195 starts from a stricter baseline where start-up expenditures are generally not immediately deductible unless election rules apply. When they do apply, the statute allows up to $5,000 immediately, phased down once total start-up costs exceed $50,000, with the remainder amortized over 180 months from the month the active trade or business begins. For that process, see How to Deduct Startup Costs for Your Freelance Business.

How does this change your cash flow or tax timing?

Your cash outflow happens when you buy the asset. The tax effect changes because amortization spreads deductions across later periods instead of taking the full benefit now. That can stabilize reporting, but you should not expect a full current-year write-off unless immediate-expensing rules clearly apply.

What records should you keep, and when should you talk to a tax professional?

Keep a complete file: invoice, proof of payment, full contract or license terms, transfer evidence, business-purpose memo, placed-in-service date, and any purchase agreement with allocation details. Talk to a tax professional if facts are cross-border, bundled across multiple assets, involve related parties, have unclear ownership, or are material. Escalate as well when Section 197 is in play but the intangible may be self-created rather than acquired.

Do you need special software to track this?

No, but you do need a consistent asset file with basis, dates, classification notes, and reporting path. A spreadsheet can work if you include checkpoints for acquisition month, placed-in-service month, and support documents before year-end. Do not treat the $2,500 de minimis safe harbor as a shortcut for these intangible classification decisions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

How to Deduct Startup Costs for Your Freelance Business

**If you want to claim startup costs safely, run a system that classifies each expense, confirms business start timing, applies startup deduction and amortization rules, and saves proof for every decision.**