Quick Answer

No. Airbnb coverage should be your fallback, while your own short-term-rental policy remains the primary contract. Host damage requests run through the Resolution Center with a 14-day filing window and a 24-hour guest response step, so timing and cash flow can become your problem first. Keep control by setting up legal separation, matching the named insured to operations, and documenting insurer approval before bookings.

Layer 1: The Foundation - Your Personal & Legal Shield#

Before you rely on AirCover for Hosts, build your own base first. You need a legal setup you can defend, a policy that clearly allows how you host, and a simple exposure worksheet so you know what you are trying to protect.

Keep your entity and operations aligned#

Your entity only helps if your day-to-day operation matches it. A sole proprietorship does not create a separate legal entity, and an LLC is most useful when the paperwork, insurance, and operating details all point to the same owner and operator.

Before you scale, align practical details: property title or leaseholder, permit or registration holder, listing operator, and insured name or names. These details can vary by jurisdiction and policy form, but your file should clearly show who owns the property, who runs the listing, and who is insured.

Keep business and personal money separate. Use separate accounts, and keep a clear document trail for rent collection, expenses, approvals, and insurance records.

Choose the base policy based on how you actually host#

Start from a conservative assumption: most standard homeowners or dwelling policies are not built for short-term-rental accident exposure. Depending on your insurer and your hosting pattern, you may need notice, an endorsement, or a business or STR-specific policy.

| Route | Usually fits | Main risk or exclusion | Confirm before booking |

|---|---|---|---|

| Homeowners/dwelling policy without STR approval | Not a durable option for active hosting | Business-use exclusions can apply; undisclosed hosting can create claim risk | Whether any short-term rental use is allowed |

| Existing policy + endorsement/rider | Limited or occasional hosting when offered by insurer | Coverage can be narrow and condition-based | Endorsement explicitly allows STR use at your address and is active before guest stay |

| STR-specific or business policy | Frequent hosting or clearly commercial operation | Terms differ by carrier and policy form | Policy is written for STR activity, with correct insured party and clear property/liability terms |

If your hosting looks like a business, treat it like one and get clear insurer confirmation. Airbnb also says AirCover is not a substitute for your own insurance and advises you to check for overlap with your insurer.

Verify before accepting bookings#

Do this work before the first booking, not after a claim. A clean pre-booking file prevents avoidable disputes about whether the use was allowed in the first place. Before you accept guests, use this checklist:

| Check | What to confirm |

|---|---|

| Local compliance status | Registration, permit or license, zoning, and any lease, condo, co-op, or HOA limits |

| Insurer disclosure | Disclose short-term-rental use to your insurer and keep a record of the response |

| Policy file | Save your final policy documents, including any endorsement, and key approval records before you accept guests |

If any one of these is unclear, pause before you accept guests.

Local rules are not uniform. For example, Massachusetts requires at least $1,000,000 liability coverage per short-term rental and also requires operators to notify their home insurer about intended short-term-rental use.

Build a simple exposure worksheet#

This worksheet does not need to be fancy. It just needs to show what a serious claim could reach and where your current coverage falls short.

- List assets, for example: property equity, cash, investment accounts, vehicles, and other material assets.

- List liabilities: mortgage, loans, credit lines, and other debts.

- Note plausible loss scenarios: guest injury, guest-caused damage, fire or water damage affecting neighbors, and enforcement-related disruption.

- Current coverage benchmark pending Airbnb policy or insurance-document verification.

- Set a target liability range based on what a serious claim could put at risk.

If the gap is large, take that as a stop signal. Tighten entity operations, upgrade insurance fit, and finish documentation before you grow bookings.

Related: The Pros and Cons of Short-Term vs. Long-Term Rentals.

Layer 2: The Commercial Shield - Your Primary, Controllable Defense#

This is your primary insurance layer because it is the part you can choose, document, and manage before a claim happens. If you rely only on platform-managed protection, reimbursement for damage or theft can be challenging, and the claims path is not fully under your control.

Choose for underwriting fit, then price#

Price matters, but fit comes first. If the wording does not match how you actually host, a lower premium does not solve the problem.

Before you compare quotes, use this filter. If the policy wording does not match your actual operation, stop there and fix that mismatch first.

- Is this policy intended to respond as primary coverage for your hosting activity, or only as supplemental coverage?

- Is short-term rental use clearly reflected in the application, binder, and endorsements for your exact address?

- What is the real claims path: first notice, adjuster assignment, escalation, and required evidence?

Compare structure before premium#

The right comparison starts with structure, not rankings. You are checking how the policy is built, where gaps can appear, and who handles the claim when something goes wrong.

| Policy structure | Control point to verify | Typical gap or friction to check | Claims handling check | Coordination with dwelling policy |

|---|---|---|---|---|

| Standalone STR commercial policy | Confirm the named insured and covered location match your operation | Confirm whether property, liability, and income-loss parts are in one contract or split | Confirm where first notice is filed and who owns the file | Confirm whether this replaces or sits alongside your dwelling setup |

| Dwelling policy + STR endorsement | Confirm the endorsement is active for short-term rental use | Confirm what the endorsement adds and what exclusions remain | Confirm whether one or multiple claims teams handle losses | Confirm endorsement timing and address/use alignment |

| Supplemental commercial layer + dwelling policy | Confirm which policy is primary for each loss type | Confirm overlap or "other policy responds first" friction | Confirm whether notice must be given to both carriers | Confirm both policies acknowledge hosting activity |

Decision checklist by risk type#

The fastest way to compare policies is to test them against the losses you are most likely to face. That keeps you from buying a policy that looks broad in marketing but breaks down in actual claim scenarios.

| Risk type | What to verify |

|---|---|

| Guest-caused property damage | Whether guest-caused damage, theft, or vandalism is handled under your property terms, and under what deductible or sublimits; ask specifically about care, custody, and control (CCC) |

| Liability tied to hosting activity | Bodily injury and property damage limits, and where liability coverage applies in your own forms; if you offer extras linked to the stay, confirm they are covered |

| Business interruption / income loss | What event triggers coverage, how income loss is calculated, and what documentation is required; request the actual endorsement text before binding if wording is unclear |

| Exclusion review | Review exclusions before purchase; if forms are withheld until binding, treat that as a process risk |

- Guest-caused property damage

Confirm whether guest-caused damage, theft, or vandalism is handled under your property terms, and under what deductible or sublimits. Ask specifically about care, custody, and control (CCC). CCC refers to property in your possession or direct responsibility; when you take possession, you may assume a legal duty of care. Standard CGL forms can exclude property in your care, custody, or control, and without separate CCC coverage, losses may be out of pocket.

- Liability tied to hosting activity

Confirm bodily injury and property damage limits, then verify where liability coverage applies in your own forms. If you offer extras linked to the stay, confirm they are covered instead of assuming they are.

- Business interruption / income loss

If income-loss coverage is included, confirm what event triggers coverage, how income loss is calculated, and what documentation is required. If wording is unclear, request the actual endorsement text before binding.

- Exclusion review

Review exclusions before purchase, not after a loss. If forms are withheld until binding, treat that as a process risk.

Set up your claim-ready file#

A good policy still creates friction if your records are scattered. Set up the file now so you are not trying to reconstruct the basics during a live claim.

- Collect and store declarations, full policy forms, endorsements, application, and binder in one place.

- Verify named insured, property address, and mortgagee or additional-interest details against your real operating setup.

- Write a one-page claim SOP with reporting channel, timing expectations, and required first-evidence items.

- Limits, sublimits, deductibles, and waiting periods must be verified from current policy forms, endorsements, or insurer records before use.

- If you use smart entry, retain access logs and checkout-expiring credentials where supported. These records can help establish who accessed the property and when.

Once you lock in your primary policy, map how money moves through your hosting business so payouts and records stay traceable: Review the Gruv docs.

Layer 3: The Platform Backstop - Positioning AirCover as Your Final Safety Net#

Treat AirCover as backup, not your primary protection. Airbnb says it is not a substitute for personal insurance, and its programs do not replace homeowners, renters, or other applicable liability coverage.

Use a simple ownership test here:

- Who owns the policy or program terms?

- Who controls claim decisions?

- What options do you have if a claim is denied?

With AirCover, your path runs through Airbnb processes and terms. For liability matters, Airbnb says claim information is sent to a third-party insurer, which assigns a representative and resolves the claim under policy terms.

Use the ownership test, not the marketing label#

The label can make this look simpler than it is. AirCover for Hosts is a program bundle, not a single insurance policy. Airbnb describes it as including guest identity verification, reservation screening, Host damage protection, Host liability insurance, and a 24-hour safety line.

Host damage protection is a reimbursement program, not an insurance policy. For eligible guest-caused damage, Airbnb requires you to file in the Resolution Center within 14 days of checkout. The guest then has 24 hours to respond before Airbnb Support reviews unresolved, partial, or declined requests.

In practice, that can create a cash-flow issue because you may need to pay for urgent repairs before reimbursement is resolved.

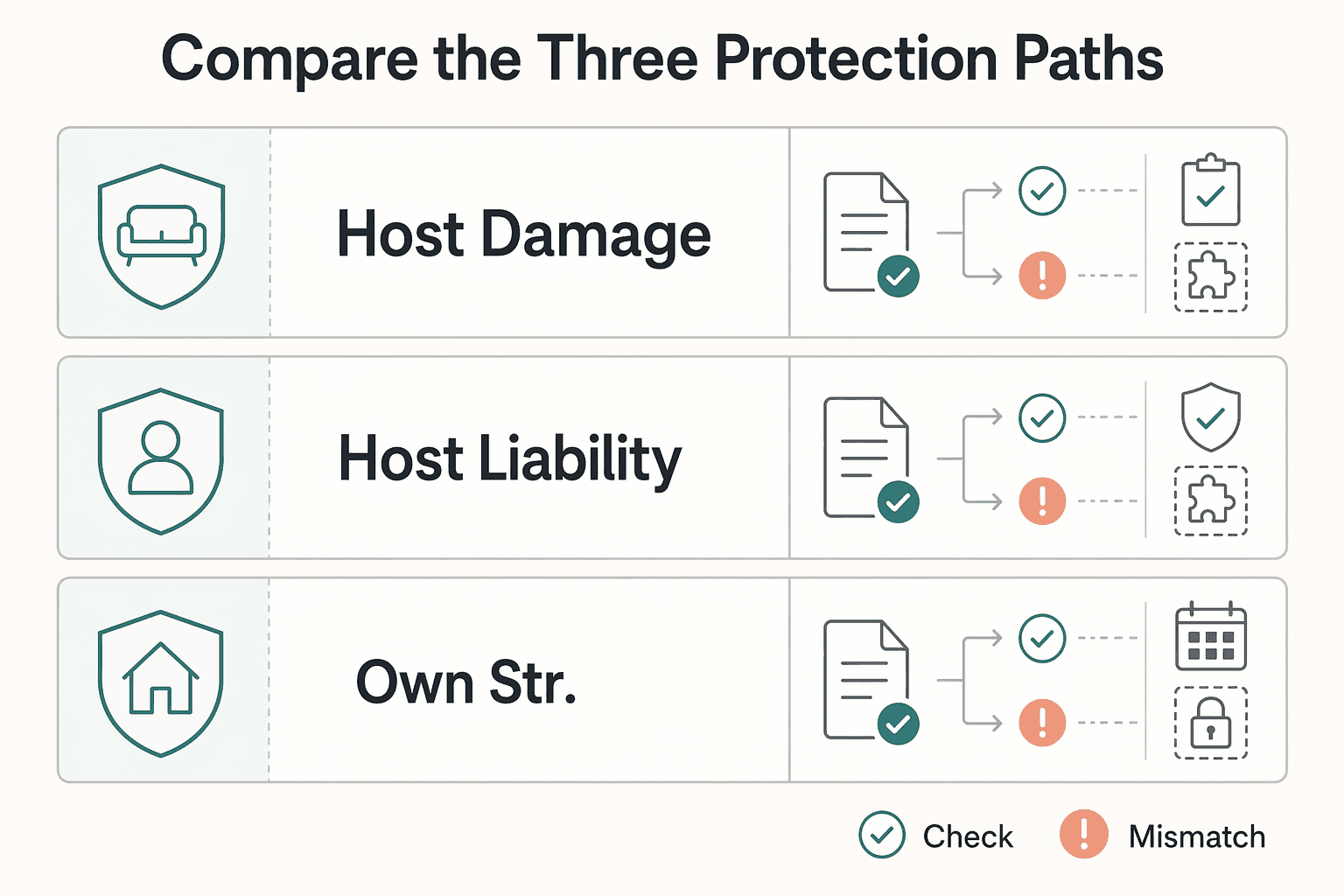

Compare the three protection paths#

Once you separate your own policy from the platform backstop, the tradeoffs are easier to see in the table below.

| Protection path | Claim pathway | Payout timing | Review or appeals control | Cash-flow impact |

|---|---|---|---|---|

| Host damage protection | File in Resolution Center within 14 days; guest gets 24 hours; Airbnb Support reviews unresolved cases | No verified guaranteed payment timeline | Governed by Airbnb terms and process; U.S. Host Damage Protection terms include arbitration and class-action waiver | You may carry out-of-pocket repair cost while waiting |

| Host liability insurance | Report incident; claim is routed to a third-party insurer; insurer assigns a representative and decides under policy terms | No verified guaranteed payment timeline | Decision process is controlled under insurer policy terms | May help with covered liability costs, but you do not directly control handling |

| Your own STR commercial policy | Follow your carrier or broker notice process under your policy terms | Carrier- and form-specific | Defined by your policy terms and applicable law | Depends on deductibles, reserves, and claim handling terms |

Before you rely on stated limits or layering, check two things:

- Airbnb pages show conflicting Host damage numbers (

$3Mon one Help page vs$1Mon the AirCover page), so verify the current page, jurisdiction, and terms at decision time. - For hosts with 6+ active listings at time of loss, Airbnb's HLI summary says that effective March 1, 2025, coordination with other insurance may apply on an excess basis depending on policy language.

Map common gaps to Layer 2 features#

Use the platform gaps to pressure-test your own policy, because that is where you regain control.

| AirCover gap or friction point | What to verify in your own policy |

|---|---|

| Host damage protection does not cover normal wear and tear | Property terms for guest-caused accidental damage vs maintenance, plus your reserve and inspection process |

| HLI does not cover damage to your own place or belongings caused by a guest | Property coverage, deductibles, sublimits, and related endorsements for guest-caused loss |

| HLI may coordinate as excess for some 6+ listing hosts | Primary vs excess order, dual-notice requirements, and listing or use alignment in your policy documents |

| Airbnb states other exclusions apply | Current exclusion detail pending Airbnb policy or insurance-document verification. |

Incident workflow checklist#

When something happens, sequence matters as much as coverage. Your goal is to preserve evidence, meet deadlines, and avoid notice mistakes.

| Step | Key detail |

|---|---|

| Document loss immediately | Dated photos or video, messages, invoices or estimates, and relevant access records |

| Notify both channels quickly | File required Airbnb workflows within deadline, and notify your own carrier where your policy may respond |

| Preserve evidence | Keep evidence until claim handlers confirm what can be repaired, replaced, or discarded |

| Track deadlines in one place | 14-day Resolution Center filing, 24-hour guest response stage, and carrier notice deadline pending insurer or policy-document verification |

The common mistake is waiting on one channel and missing the deadline on the other.

Conclusion: Trade Anxiety for Control#

The operating decision is straightforward: control the protection you own, and treat AirCover as a backstop. Airbnb says AirCover is not a substitute for personal insurance, and its Host liability insurance is still subject to policy terms, conditions, and exclusions.

Use this sequence:

- Confirm legal separation first. A sole proprietorship does not create a separate business entity, and while an LLC or corporation can help protect personal property, that protection has limits.

- Confirm your primary policy setup. Make sure the named insured on the policy is the correct person (or persons), because that party has policyholder status.

- Then use AirCover as supplemental support for Airbnb-booked stays. Airbnb describes automatic coverage for those stays, including up to $1M Host liability insurance and up to $3M Host damage protection. Those limits do not replace your own policy.

What this gives you: more control over your primary recovery path. What this does not guarantee: full reimbursement on every loss, no exclusions, or a frictionless claim outcome every time.

Keep this as a recurring process, not a one-time setup. Review your entity structure and policy documents periodically so they still match how you actually host.

For a step-by-step walkthrough, see Do You Need Separate Short-Term Rental Insurance?.

If your rental operation is becoming cross-border, get a quick program-fit check before you add new payment workflows: Talk with Gruv.

Frequently Asked Questions

Is AirCover enough for hosts?

AirCover for Hosts is included automatically and free for Airbnb-booked stays, but it may not be enough on its own for every host. Verify the terms and exclusions in the policies you rely on.

What is the biggest risk of relying only on AirCover?

The biggest risk is a claim-path mismatch. Host liability insurance applies to certain legal-liability events, while guest-caused damage to your own place or belongings is handled under Host damage protection, and intentional acts are excluded from host liability insurance. For liability claims, use Airbnb’s intake form, then follow the assigned third-party insurer representative under policy terms.

Does AirCover cover loss of income?

Do not assume it does. Airbnb describes host liability insurance around certain liability events, so verify current terms before relying on any income-related protection.

How do I calculate how much insurance I need?

There is no fixed formula in this article. Set your limits based on your exposure and the policy terms you can verify, then review those limits before renewal.

What are the key things AirCover for Hosts does not cover?

Airbnb states host liability insurance excludes intentional acts, and damage to your own place or belongings caused by a guest is handled under Host damage protection instead. Airbnb also lists applicability carve-outs, including stays through Airbnb Travel, LLC, Experiences or Services, and hosts offering stays in Japan. Verify exclusions and eligibility terms for your listing type and location.

What is the difference between Host damage protection and Host liability insurance?

They are different claim paths. Host liability insurance applies when you are found legally responsible for certain injury or property-damage events, while Host damage protection addresses guest-caused damage to your own place or belongings.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- dfs.ny.gov/consumers/help_for_homeowners/homeowner_tena...trusted

- mass.gov/info-details/short-term-rental-insurancetrusted

- sba.gov/business-guide/launch-your-business/choose-b...trusted

- sba.gov/blog/5-ways-separate-your-personal-business-...trusted

- sec.gov/Archives/edgar/data/1559720/0001559720250000...trusted

- airbnb.com/help/article/3145external

- airbnb.com/help/article/937external

- content.naic.org/article/consumer-insight-renting-out-your-ho...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

The Pros and Cons of Short-Term vs. Long-Term Rentals

You are probably not chasing the biggest headline revenue number. You want rent that arrives, stays collected, and does not turn into a second job or a cross-border tax headache. For an owner living internationally, the real choice between a short stay and a long-term lease is about risk first. Which model gives you lower compliance exposure, less remote operating drag, and more cash left after fees, taxes, and reporting?

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.