Quick Answer

Book incurred costs at period end before invoices arrive. In this accrued expenses guide, that means posting an adjusting entry for completed contractor work, recorded software usage, or tax tied to recognized revenue, then moving matching cash to reserve. Use invoice status to decide classification: no bill yet is accrued expense, bill received is accounts payable. Reconcile estimates to actual bills so your close supports spending, pricing, and commitment decisions.

Why a Simple Accounting Shift is Your Best Defense Against Financial Anxiety#

If your cash balance looks healthy but you still do not trust your month-end numbers, you likely have a timing problem, not just a revenue problem. The fix is simple. Stop treating the bank account as the full story and start recording costs when you incur them, not only when cash leaves.

That shift gives you better control. Under the cash method, the practical question is, "What got paid?" Under the accrual method, the better month-end question is, "What did this month actually cost me?" IRS Publication 538 frames the difference around timing. The cash method follows receipt and payment timing, while accrual accounting is meant to match income and expenses to the correct period. In practice, that can change real decisions, like whether the month was actually profitable, whether an owner draw is safe, or whether new spending should wait.

An accrued expense is a cost that has already happened but is not yet in the books. That matters because month-end decisions should reflect work received and usage consumed, even when the invoice has not arrived. If a contractor finished client work on the 29th, or your usage-based software ran all month, your bank balance may look generous while your actual free cash is already spoken for.

In 2026, a $1,200 software overage, a $2,500 subcontractor invoice still in transit, and a $900 tax top-up can all belong in the same close. If you ignore them, a 25% reserve target can look safe while your real obligations are already higher.

| Liability bucket | Bank balance signal | Accrual-adjusted signal | Decision impact |

|---|---|---|---|

| Contractor or assistant work already completed | Cash still looks available until the invoice arrives | You estimate the earned labor cost and record it as an accrued expense | You avoid treating gross receipts as spendable profit |

| Usage-based software or service consumption already incurred | No visible hit yet if billing posts next month | You record the month's consumed usage based on documented calculations | You decide earlier whether current pricing still covers tool costs |

| Other unbilled goods or services already received | Looks like "nothing owed yet" because there is no bill in inbox | You recognize the obligation in the period the service was received | You get a cleaner read on margin before committing to more work or spend |

The tool that makes this work is the accrual adjusting entry you post at period end, before statements go out. You are not trying to predict the future. You are capturing obligations that already exist, using reasonable, documented calculations.

Three ways this lowers stress at month-end#

First, check what has already been delivered or consumed but not yet billed. That means reviewing completed contractor work, open service periods, and usage reports before you close the month. Then record the estimate now instead of waiting for the vendor to tell you what you already know happened. The result is simple but important: you can tell whether the month produced real surplus cash or just the appearance of it.

| Action | Support to review | Why it matters |

|---|---|---|

| Check what was delivered or consumed but not yet billed | Completed contractor work, open service periods, and usage reports | Shows whether the month produced real surplus cash or just the appearance of it |

| Put evidence behind every estimate | Time logs, agreed rates, a vendor dashboard export, service dates, or another document saved with the entry; current cutoff, reserve rule, or threshold pending source verification if used | Makes the estimate easier to defend and true up later |

| Reconcile the estimate when the actual bill arrives | Compare the invoice to the estimate and note missing usage data, unapproved rate changes, incomplete time logs, or service periods booked in the wrong month | Improves later decisions on pricing, hiring pace, and discretionary spending |

Second, put evidence behind every estimate. A solid accrual ties back to time logs, agreed rates, a vendor dashboard export, service dates, or another document you can save with the entry. A common problem is loose round-number guessing with no support. Those estimates are hard to defend and even harder to true up later. If your internal policy uses a cutoff, reserve rule, or other threshold, verify the value against your accounting policy, contract terms, or official source records before using it in the accrual.

Third, reconcile the estimate when the actual bill arrives. If the invoice matches closely, your close is working. If it does not, you learn where your evidence is weak: missing usage data, unapproved rate changes, incomplete time logs, or service periods booked in the wrong month. That feedback loop improves later decisions on pricing, hiring pace, and discretionary spending because your liability picture gets sharper with each close.

Keep one boundary clear before you go further. If you have incurred the obligation but have not received the bill, you are dealing with an accrued expense. Once the invoice is in hand, that same obligation moves into accounts payable. If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

Accrued Expenses vs. Accounts Payable: A Litmus Test for the Business-of-One#

Use this close rule every period: if the cost was incurred but no invoice is in hand, book an accrued expense; if the invoice has arrived, book accounts payable. The split is invoice status, not payment status.

| Decision point | Accrued expense | Accounts payable |

|---|---|---|

| Trigger | Work, service, or usage already happened, but no invoice yet | Vendor invoice or bill has been received |

| Recognition timing | At period end through an adjusting entry for costs not yet recorded | When the invoice is posted |

| Amount basis | Estimate using current reliable information | Exact amount on the invoice |

| Balance-sheet impact | Estimated current liability if due within the next 12 months | Actual current liability if due within the next 12 months |

| What you do next | Save support, book the estimate, then await the invoice | Schedule payment, then reconcile and clear any prior accrual for the same item |

Keep the handoff tight during close:

- Identify incurred but unbilled costs and post the adjusting entry.

- When the invoice arrives, record the payable as the actual supplier liability.

- Reconcile the invoice to the earlier estimate and clear the accrual so you do not double count one obligation.

Getting the classification right directly affects decisions. If you wait for invoices, margin looks stronger than it is, reserves run light, and pricing or spend decisions get delayed.

For each estimate, keep a compact evidence pack:

- work confirmation or delivery proof

- usage report, dashboard export, or prior-usage basis (for example, a $1,200 estimate from known history)

- contract terms, rate sheet, and internal cutoff note pending source verification

Next, focus on where these liabilities usually hide before close so they do not slip through. For a faster read on where they appear on statements, see How to Read a Balance Sheet. For a related workflow, see The Best Way to Handle Shared Expenses with a Freelance Collaborator.

The 3 Hidden Liabilities That Can Sink a Solo Business#

At close, start with three buckets: unbilled contractor work, unbilled usage-based tool costs, and tax tied to recognized revenue. If you miss any of them, your cash looks safer than it is, and that can push bad spending decisions.

| Liability bucket | Trigger | Evidence to collect | Estimate basis | Owner | Decision risk |

|---|---|---|---|---|---|

| Contractor and VA costs | Service was rendered by period end, but no invoice is received yet | Approved hours, milestone signoff, deliverable handoff, contract terms, rate sheet, cutoff note | Agreed hourly rate, milestone amount, or expected fee from current terms | You or your bookkeeper | Margin looks higher than reality, so you commit cash that is already spoken for |

| Usage-based tools | Usage happened before billing-cycle close, but final bill is pending | Usage export, billing dashboard snapshot, pending overage/threshold notice, billing-cycle cutoff date, activity log | Period-to-date usage plus known late-period activity and current pricing data | You, ops lead, or bookkeeper | Spend lands late and makes a normal month look unstable |

| Tax on recognized revenue | Revenue is recognized before filing/payment, so tax liability builds in period | Revenue report, estimate worksheet, prior remittance record, assumption note | (selected base × source-verified current rate assumption) - amounts already remitted | You, with tax advisor input if needed | You treat reserve cash as free cash and create pressure before estimated payments |

For contractor and VA costs, use a strict cutoff rule: if work was delivered by period end, accrue it; if the invoice has arrived, move it to accounts payable. Keep proof that the work was completed in-period, not just expected, then reconcile the estimate when the invoice posts. Clear the accrual against the payable or payment so you do not carry both and double count the same obligation.

For usage-based tools, assume partial visibility until proven otherwise. Check usage exports, pending overage notices, and billing-cycle cutoffs before close. If data is incomplete, use the latest reliable export plus a conservative add-on for known end-of-period activity, and mark it for true-up when the invoice arrives.

Tax is the least visible bucket, so keep the principle simple: liability builds as income is earned or received, not only at filing time. For U.S. readers, estimated taxes are generally handled during the year, often quarterly, and Form 1040-ES is the working reference; verify any threshold-specific decision against official tax guidance or source records before use. Document your assumptions, update them when revenue changes, and move reserve cash on a fixed cadence so the liability is funded, not just recorded.

From there, run this as a repeatable close flow in order: identify, estimate, then fund.

A 3-Step Framework for Turning Liabilities into a Strategic Tool#

Use the same close sequence every time: identify, estimate, then fund. That keeps accrued expenses useful as a decision control instead of turning them into last-minute cleanup.

Identify what was incurred before period end#

Capture accrual candidates before invoices arrive. These are costs already incurred but not yet paid. For each line, record: owner, source evidence, cut-off status, category, and provisional amount.

| Accrual candidate | Evidence to capture | Record with the line |

|---|---|---|

| Contractor work | Approved hours or milestone proof plus agreed terms | Owner, source evidence, cut-off status, category, and provisional amount |

| Usage-based tools | Latest reliable usage record, pricing reference, and billing-cycle cut-off note | Owner, source evidence, cut-off status, category, and provisional amount |

| Tax tied to recognized revenue | Revenue report, estimate worksheet, and assumption note | Owner, source evidence, cut-off status, category, and provisional amount |

- Contractor work: approved hours or milestone proof plus agreed terms.

- Usage-based tools: latest reliable usage record, pricing reference, and billing-cycle cut-off note.

- Tax tied to recognized revenue: revenue report, estimate worksheet, and assumption note.

If you cannot show the work or usage happened by period end, hold the line for review instead of accruing it. This prevents "expected bills" from being treated like incurred obligations.

Estimate each line and log the assumption#

Estimate by liability type and document the ground rules with the number. The estimate is not complete without the assumption record.

| Liability type | Estimate basis | Documentation note |

|---|---|---|

| Contract labor | Agreed terms and completed work | Current assumption pending source verification |

| Usage-based software | Latest reliable usage and current pricing | Incomplete input and confidence level pending source verification |

| Tax tied to recognized revenue | Current internal method | Log the base/rate assumption in plain language |

Add a confidence tag to each estimate so review is faster. If history is available, compare against at least 12 months of actuals as a reasonableness check; if not, flag uncertainty clearly.

Post it, fund it, then true up#

Post the accrual first so the liability is visible on the balance sheet, then move matching cash to the reserve you use for payment. When the actual bill posts, update the estimate with actual costs and clear the old estimate; if your books move the item to accounts payable, reclass where applicable so the same obligation is not carried twice.

| Quality gate | What to check | Failure mode | Corrective action |

|---|---|---|---|

| Evidence attached | Each line has source support and cut-off status | Guesswork gets accrued | Hold posting until support is attached or defer to next close |

| Assumption log | Method and dated assumption note are present | Estimate cannot be reviewed later | Add method, assumption, and owner before close |

| Category accuracy | Line is mapped to the correct liability category | Margin or liability view is distorted | Reclass before reporting |

| Reserve alignment | Reserve transfer matches posted accrual total | Books and cash plan drift apart | Recalculate and adjust transfer immediately |

| Actual-cost update | Actual bill is matched to prior estimate | Old accrual remains or is double counted | Reconcile variance, clear estimate, and reclass where needed |

For implementation details in your workflow, use How to Manage Bookkeeping for Your Freelance Business.

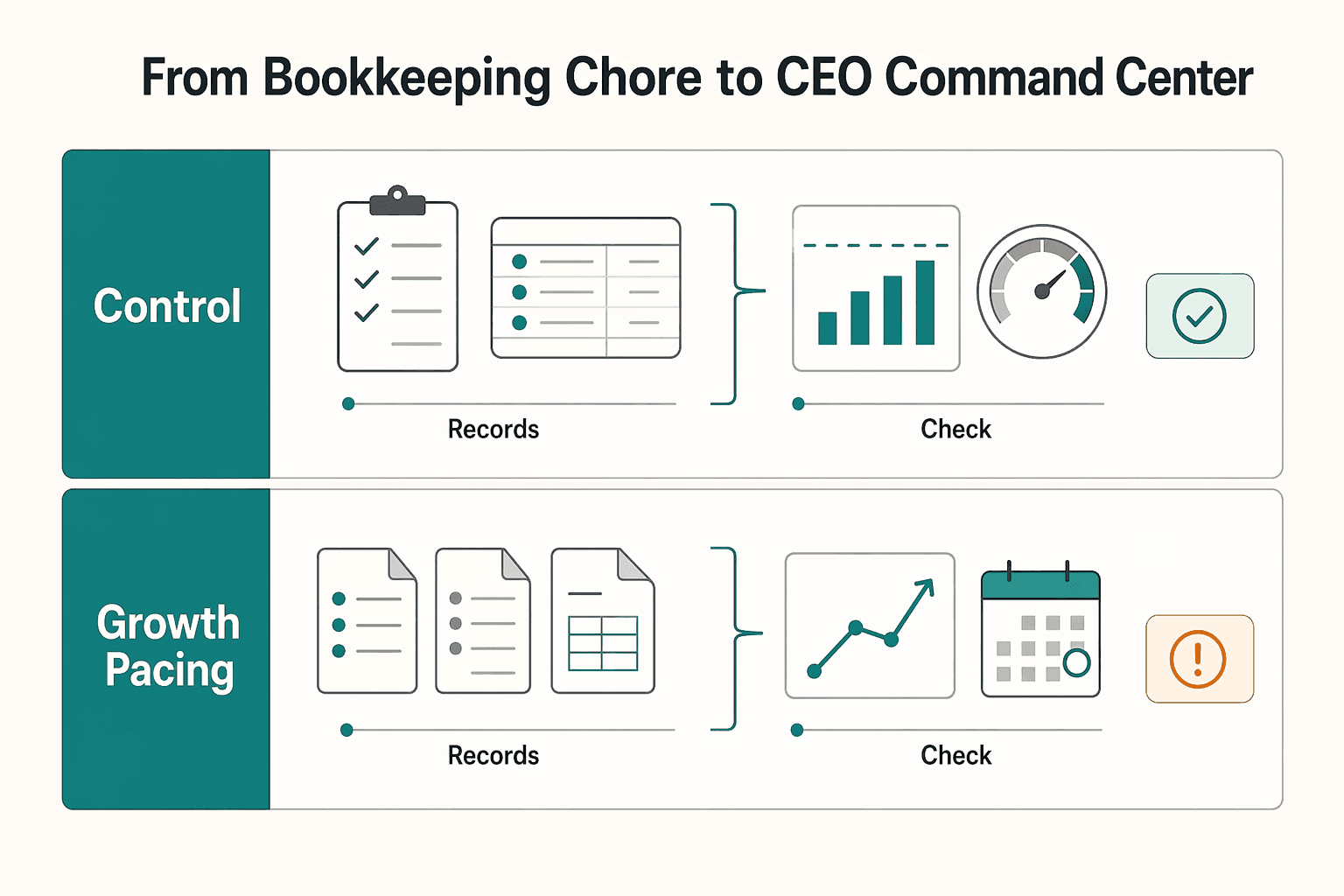

From Bookkeeping Chore to CEO Command Center#

Your close becomes useful when you treat accrued liabilities as a decision control, not a bookkeeping afterthought. If you wait for invoices or a low bank balance, you react late; if you log what was already incurred at period end, you can adjust spending, pricing, and growth before final review.

In practice, switch your question from "what cleared cash?" to "what obligation already exists?" Under accrual accounting, the point is to match income and expense in the correct period, not by payment date. For your close, focus on current liabilities due within the next 12 months and make operating calls while you can still act.

| Decision area | What you check before final close | What you do next |

|---|---|---|

| Spending control | Unbilled contractor work completed by period end | Book the accrual, move matching cash to reserve, and pause discretionary spend until that is done |

| Pricing control | Variable software usage that increased during delivery | Recheck scope, margin, or renewal terms before pricing similar work again |

| Growth pacing | Estimated tax tied to recognized revenue | Set aside cash now and confirm upcoming estimated-tax due dates |

Use a short, repeatable close checklist:

- Identify incurred but unbilled costs, and keep evidence notes (approved hours, usage exports, tax worksheet).

- Record the accrual and move matching cash to a labeled reserve; if a bill is already received, treat it as accounts payable.

- Run one decision gate before final review: spend now, reprice, or delay the next commitment.

Anchor each step in evidence, not memory. A common failure is double counting: you book an estimate, then record the bill later without clearing or reversing the original accrual. If you need a refresher on method choice, see A Guide to 'Accrual' vs. 'Cash Basis' Accounting for a Small Agency. We covered this in detail in A Guide to QuickBooks Self-Employed for Freelancers.

Frequently Asked Questions

How should I handle tax accruals without waiting for quarter-end panic?

Use the same sequence as the rest of your close: estimate the tax tied to recognized revenue, record the liability, then move matching cash into a tax reserve. If you are in the US, the IRS says taxes must be paid as income is earned, and individuals generally have to make estimated payments if they expect to owe $1,000 or more, while corporations generally use a $500 threshold. Individuals generally use Form 1040-ES to figure estimated tax. Keep the revenue report, your estimate worksheet, and a dated note showing the rate or base assumption you used, because underpaying estimated tax can trigger penalties.

How do I tell an accrued expense from accounts payable in the middle of close?

Ask one question first: has the cost already been incurred by period end, even if no bill has arrived? If yes and it is still unrecorded and unpaid, treat it as an accrued expense. If the vendor has already billed you or you bought on supplier credit and the amount is currently due, it belongs in accounts payable. Your checkpoint is cutoff proof, not invoice timing, so save the work log, usage report, or tax worksheet that shows the obligation existed before period end.

Quick comparison

| Item | Accrued expense | Accounts payable | | --- | --- | --- | | What triggers it | Cost was incurred by period end but not yet recorded or paid | Supplier credit or billed amount currently due | | What evidence to keep | Cutoff proof, estimate method, supporting source file | Vendor bill, contract, approval, due details | | Next move | Record estimate now and true up when actual arrives | Record payable and pay or schedule payment |

Which categories should I review first if I want the biggest risk reduction?

Start with the items most likely to exist before a bill shows up: wages, taxes, and other services incurred before billing. Those are the liability lines most likely to build quietly and distort your balance sheet if you only book them when cash leaves. For each one, keep one source document and one assumption note: approved hours plus rate, a revenue report plus tax worksheet, or other period-end support showing the obligation existed before close.

What is the cleanest way to clear an accrued item when the real bill arrives?

Compare the actual bill to the estimate before you post payment, then clear or adjust the original accrual so you do not carry both the estimate and the billed amount. If your books move the vendor bill into accounts payable, payment should reduce that payable balance, not sit beside an old accrual that never got reversed or reclassed. Attach the final bill, note the variance, and clear the line the same day you record the actual so the audit trail stays obvious.

Should I use reversing entries for accrued expenses?

You can, but treat them as optional, not automatic. Reversing entries are an optional accounting-cycle step, and teams often use them because they reduce the risk of counting expenses twice when the actual bill lands in the next period. If you use them, document which accruals are set to reverse and review those lines early in the next close so a reversal does not create a new mismatch.

Does this still matter if I manage the business mostly from cash in the bank?

Yes, because cash only shows what has been paid, not what you already owe. Accrual basis accounting records expenses in the period they occur, which makes it a better operating view when you are deciding whether you can hire, spend, or draw cash. If you keep an internal accrual view, use the same method each period and save the same evidence fields each time so your numbers stay comparable. A good close stays boring on purpose: same checklist, same evidence fields, same reserve step, same reconciliation cadence. That consistency is what turns liabilities from surprises into decisions you can trust.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Freelance Bookkeeping for Faster, Safer Client Payments

Control over cash starts with records you trust. When entries are current, categorized, and easy to trace, you spot risk earlier and make calmer decisions about follow-up, spending, and month close.

How to Read a Balance Sheet for Freelancers and Small Teams

Use your balance sheet as a dated decision dashboard, not an accounting exercise. It shows what your business owns, what it owes, and what is left on that date. Use it to make better calls on cash safety, client risk, tax readiness, and growth timing.