Quick Answer

Use occam's razor for problem-solving as a context check: apply classic triage to routine operational friction, simplify repeatable workflows to reduce handoff errors, and switch to a safety-first stance for compliance uncertainty. For overdue invoices, silent proposals, or delivery glitches, verify records first. For tax residency, VAT, privacy, or reporting questions, confirm facts and guidance before filing, invoicing, or sharing regulated data.

The Razor's Edge: Why Elite Professionals Misuse Occam's Razor#

In client work, occam's razor for problem-solving can be a starting point, not a verdict. Start with the simplest explanation you can test quickly. That helps because a mental model simplifies reality enough for you to act, but the model is not reality.

That instinct is useful for low-stakes friction. The risk starts when you apply the same shortcut to every situation, instead of checking whether the evidence still fits. Good reasoning needs more than one lens, especially when the cost of being wrong is high.

| Decision context | Good use of the razor | Costly misuse | First verification step |

|---|---|---|---|

| Minor delivery issue | Assume a simple handoff or version error first | Assume the client is unhappy and start rewriting everything | Check the latest file, comment thread, and agreed scope |

| Quiet client | Assume delay, inbox overload, or scheduling friction | Read silence as a strategic crisis | Verify last contact date and send one clear follow-up |

| Contract or data question | Treat your first read as provisional | Act on the easiest interpretation without checking evidence | Re-read the exact clause, request, or requirement before acting |

The failure mode is not simplicity. It is treating your first clean explanation as the truth because it fits what you want to believe. The checkpoint is map updating. If the evidence does not match your first take, revise the take. An explanation can look clean on paper and still fail when you test it.

So the question that carries through the rest of this article is simple: choose the simplest explanation you can safely test first, not the one that merely feels easiest.

Related: A guide to 'Mental Models' for freelance strategists.

Part 1: The Triage Protocol - Solve 90% of Operational Problems Faster#

Use triage, not guesswork: identify the issue, start with ordinary causes, run the lowest-effort check, and escalate only when evidence no longer fits. In daily operations, the razor is a starting point you test, not a conclusion you defend.

When an invoice is late, cash-flow pressure can push you toward a dramatic story. Start narrower. Assume there may be a handoff, receipt, or payment-detail gap, then verify what you already have before you send an escalation message.

For a silent proposal, use the same sequence. Silence is not automatically a rejection. First verify the thread, the last agreed next step, and whether receipt was confirmed. Then send a short follow-up with one concrete question.

| Trigger | Working assumption to test first | Lowest-effort first check | Escalate when evidence shows |

|---|---|---|---|

| Invoice is overdue | An administrative or communication gap is more likely than intent | Recheck invoice copy, due date, recipient, and payment details; confirm receipt | Receipt is confirmed and a real dispute appears, change requests block payment, or responses stop after confirmation |

| Proposal has no reply | Decision timing or message visibility may be the blocker | Review the latest thread, proposal version, and last agreed next step | The prospect explicitly declines, requests major changes, or keeps the deal stalled without decision clarity |

To keep triage reliable, define success first, then track only the Critical Few metrics tied to that outcome. Here, that can be cash collected, proposals moved, and deliverables confirmed. Keep tracking simple enough that you can act fast; if only you can decode your system, action usually stalls.

Before you escalate, assemble a small evidence pack: invoice file, latest thread, current proposal version, and a one-line note on the last agreed step. This reduces avoidable conflict because you are escalating from records, not assumptions.

For a step-by-step walkthrough, see A guide to 'Positioning' for consultants.

- Write your three triage outcomes for the next business cycle.

- Track only the Critical Few metrics that map to those outcomes.

- Save one reusable evidence-pack template for invoice, proposal, and delivery issues.

- Run one fixed weekly triage review before reacting to new friction.

Part 2: The Simplicity Mandate - Are You Engineering Your Own Complexity?#

Use Occam's razor on your own workflow first: start with the simplest process explanation, then test it before blaming the client or the market. In practice, that means removing avoidable complexity so your system does not create its own delays.

Pick one real project and trace it end to end: lead capture, scope, delivery, invoicing, and payment reconciliation. At each step, ask one question: where is information copied, renamed, or reinterpreted? Those transfer points are where hidden assumptions multiply.

When handoffs are fragmented, you start filling gaps with guesswork. You assume contact details moved correctly, scope stayed aligned across versions, the delivered file matches what was billed, and incoming payment is matched to the right record. Sometimes those assumptions hold. Sometimes they fail quietly and show up later as admin fire drills.

Where the Admin Tax actually comes from#

Your Admin Tax usually comes from three sources:

| Source | Description |

|---|---|

| Manual re-entry | The same client, scope, dates, or amounts get typed again in another tool. |

| Duplicate tracking | The same status lives in two places that can drift. |

| Context switching | Before you can act, you have to reconstruct what was agreed, sent, and still open. |

That pattern does not just feel inefficient; it slows response and creates preventable rework. A simple check turns into an investigation because the evidence is scattered.

| Checkpoint | Fragmented stack | Integrated workflow |

|---|---|---|

| Failure points | More handoffs and more manual updates across tools and docs. | Fewer transfers and fewer opportunities for silent mismatch. |

| Visibility | Status is split across inboxes, files, and finance records. | Status is easier to verify from a primary record or workflow path. |

| Response speed | You spend time confirming which version is current. | You can answer faster because context is already connected. |

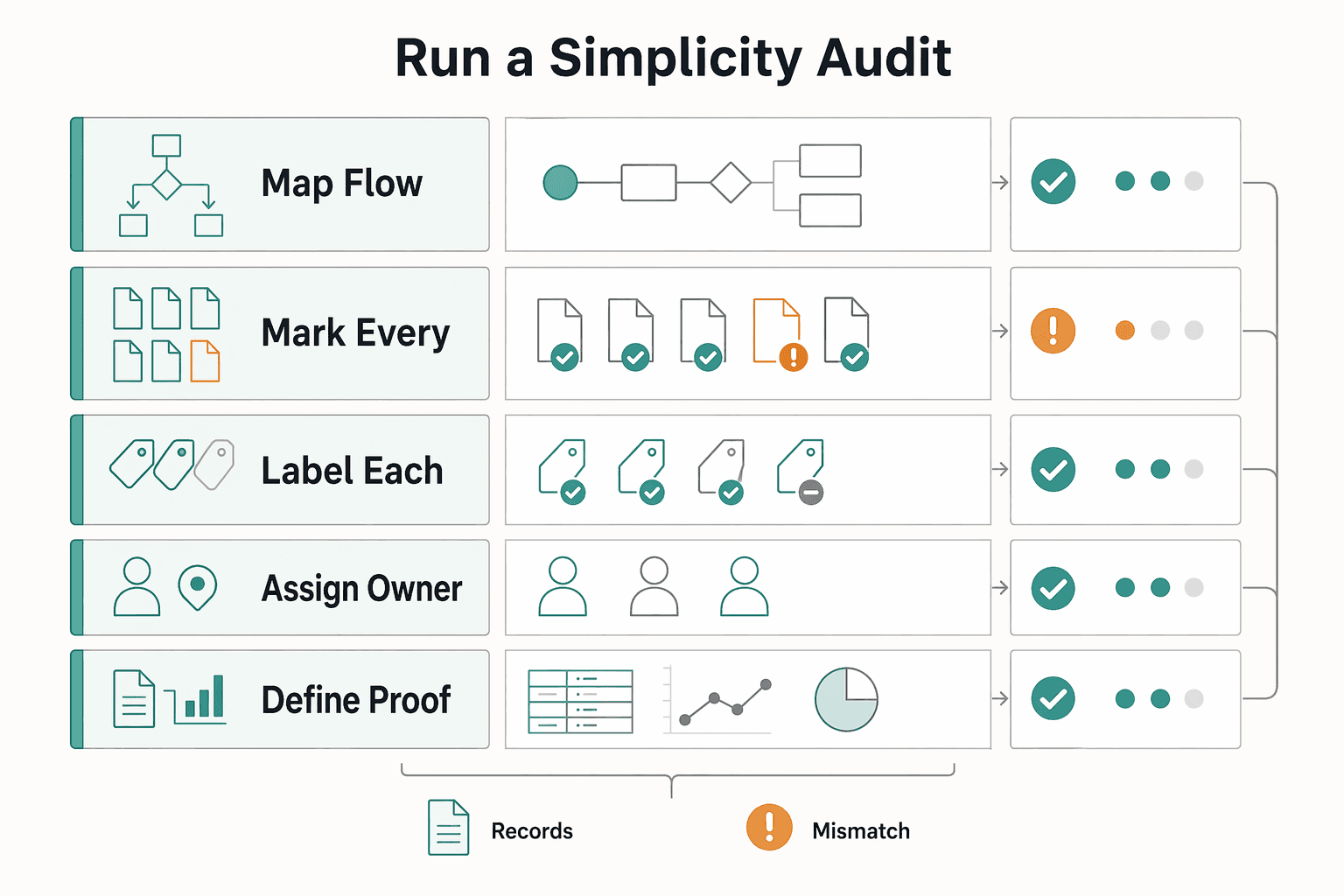

Run a simplicity audit#

Run this mini-framework on a live project or the last completed one.

| Step | What to do | Detail |

|---|---|---|

| Map the flow | Write the sequence in verbs. | captured, qualified, scoped, approved, delivered, invoiced, paid, reconciled |

| Mark every handoff | Flag each place data moves between tools, people, or documents. | tools, people, or documents |

| Label each step | Use automate for repetitive low-judgment steps with stable inputs. Use consolidate when two places track the same truth. Use keep for judgment-heavy steps where review matters. | automate / consolidate / keep |

| Assign an owner and review cadence | Every step needs one owner, even if that owner is you. Set a cadence you will actually run. | weekly in active delivery periods |

| Define proof of completion | For each handoff, state the artifact that proves done. | approval email; signed scope; sent file link; invoice; payment match; reconciliation note |

If proof is hard to find quickly, the step is too fuzzy.

Keep one caution in mind: simplicity is a starting rule, not a blind rule. If a step stays noisy or inconsistent after simplification, treat that as a signal to investigate deeper instead of forcing a simple story.

We covered this in detail in A guide to 'Antifragile' thinking for building a resilient freelance business.

Simplify aggressively where risk is internal. In the next section, the default changes when legal, tax, data, and compliance risk enter the decision.

Part 3: The Compliance Inversion - When the Simplest Assumption is the Most Dangerous#

When compliance is involved, your default changes: contain risk first, then optimize for convenience.

That is the inversion. Instead of asking, "What is the simplest explanation?", ask, "If I am wrong, which assumption creates the most damage?" In low-stakes admin work, analogy is often fine. In compliance work, inherited assumptions are often the risk.

Use this risk-first sequence#

| Step | Article guidance |

|---|---|

| Classify the issue type | Tax residency, VAT/invoicing, foreign account reporting, privacy, or contract compliance. |

| Name the downside if wrong | Late filing, incorrect treatment, missed reporting, breach of terms, or expensive cleanup. |

| Choose the safest temporary assumption | Use it only until verification is complete. |

| Verify against current authority guidance or a qualified advisor | Current rules and thresholds change. |

Tax residency is the clearest example. A risky shortcut is, "I am probably under the usual day count." A safer interim stance is that residency may be multi-factor until you verify the exact country and tax year. Treat the current day-count threshold as pending official guidance or tax-advisor verification, and keep your documentation tight.

| Issue | Risky default assumption | Safe temporary assumption | Immediate next action |

|---|---|---|---|

| Tax residency | "I am under the usual threshold, so I am not resident." | "Residency may depend on day count plus other factors; status is unresolved until verified." | Confirm jurisdiction and tax year, mark the current threshold as pending official guidance or tax-advisor verification, and assemble travel/supporting records. |

| VAT on a new cross-border client | "Invoice now and sort VAT later." | "VAT treatment may apply, so final invoice treatment waits for rule check." | Verify client location/status, service type, invoice timing, and current rules for the jurisdictions involved before finalizing. |

| Foreign account reporting | "The balance was temporary, so it probably does not count." | "Reporting may still be required; treat disclosure as possible until verified." | Check reporting year and account records, then mark the current threshold as pending official guidance or advisor verification until confirmed. |

Verify before you relax#

Your checkpoint is a small evidence pack tied to the real case, not memory or precedent. For residency, that can include travel logs, contracts, invoices, bank records, lease records, and official correspondence. For VAT or reporting issues, that can include the client file, invoice draft, account statements, and the exact guidance or written advice you relied on.

Use classic Occam triage when the downside of being wrong is mainly delay or rework. Switch to compliance inversion as soon as the issue could create filing exposure, reporting gaps, or contract risk. If someone can later ask, "Why did you treat it this way?", inversion mode should already be on.

If you want a deeper dive, read Digital Nomad Health Insurance: A Comparison of Top Providers.

Your Razor's Edge: From Problem-Solver to Risk Manager#

Use one decision rule per context, not one rule for everything. When you use occam's razor for problem-solving, start with a checkpoint: where does a simpler explanation help, and where could it hide risk?

| Context | Use this | When you use it | Concrete example |

|---|---|---|---|

| Daily operations | Triage protocol | An operations issue where the downside is mostly delay or rework | A client has not paid, a proposal got no reply, or a file link failed. First check send date, due date, inbox, permissions, and file version. |

| System design choice | Simplicity mandate | You are deciding how work should run repeatedly, not fixing one incident | Use one shared folder plus a naming rule instead of three tools and manual copy steps. Fewer moving parts usually means cleaner handoffs. |

| Compliance uncertainty | Compliance inversion | The issue touches legal, tax, privacy, or reporting consequences | Before sending regulated data or relying on a tax treatment, use the safer temporary assumption until you verify jurisdiction, period, contract, invoice draft, and the authority page behind your decision. |

This gives you a more reliable operating rhythm: fewer escalation cycles, clearer handoffs, clearer risk ownership, and faster decision recovery when an assumption fails. Keep the tradeoff in view: simplicity is useful, but not always sufficient, and sometimes a more complex model is the better fit.

Use this week:

- List open issues and label each one: operations, design, or compliance.

- Choose the matching framework before you act.

- Write one sentence with the rule you used and what evidence you checked.

- Set a review trigger, such as no reply after follow-up, a second handoff failure, or any shift into filing or data handling.

This is a professionalism shift, not a mindset slogan: you are building a durable system for your business, not just solving isolated client problems.

You might also find this useful: A guide to 'Inversion' for de-risking freelance projects.

Frequently Asked Questions

How should you use Occam's Razor in day-to-day freelance work?

Use the classic mode first: compare competing explanations and start with the one that needs the fewest assumptions. It works best as an initial pass before you have full information. If an invoice is late, first check that it was sent, the due date has passed, and the client contact actually received it. Escalate after that basic check, or sooner if the delay affects cash flow, a signed milestone, or a compliance deadline.

What should you do when a client goes quiet after you send a proposal?

Stay in classic mode unless there is a contract or reporting consequence. First assume a mundane cause, such as internal delay or a missed email, then send one short follow-up with a clear question and a specific next step. Escalate when silence blocks a signed start date, deposit, or procurement requirement.

What if a tool handoff breaks and the client says they cannot access files?

Start with the simplest operational explanation, then verify quickly. Check the share settings, the exact email address used, and whether the current folder is the one named in your delivery note. Switch out of classic mode if the handoff involves personal data, regulated data, or access rights you cannot verify cleanly.

When should you stop using the classic razor and switch to the safer mode?

Switch as soon as the issue may touch tax, VAT, foreign account reporting, privacy, or contract compliance. First make the safest temporary assumption, then treat any current rule or threshold as pending official guidance or advisor verification until the exact jurisdiction, period, and transaction are confirmed. Escalate before you file, issue the final invoice, transfer regulated data, or rely on memory instead of documents.

What should your evidence pack look like before you act on a compliance question?

Keep a record that shows both the facts you used and the rule you relied on. That can include the contract, invoice draft, client location and status details, account statements or travel records where relevant, plus the exact authority page or written advice used to decide. If you cannot match the issue to a jurisdiction, time period, and document set, treat it as unresolved and verify before acting.

Is Occam's Razor the same as first-principles thinking or risk triage?

Not exactly. Use the razor to choose the most economical starting explanation, then switch to deeper verification when the downside is material. In practice, a delayed reply can stay in classic mode at first, while unclear tax treatment calls for caution first and verification next.

Can this help with privacy or GDPR questions for client work?

Only partly. You can use classic mode to troubleshoot an operational issue, but once personal data handling is involved, move to the safer mode and verify the jurisdiction-specific requirement before you proceed. If the client is in the EU or asks for formal data handling terms, check the requirement directly or use a detailed guide like GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients. Quick-use rule: if the downside is mostly delay or rework, start simple; if the downside could be filing trouble, tax exposure, privacy risk, or breach of terms, verify first and act second. Simpler is a starting point, not an automatic proof that it is correct.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

Mental Models for Freelance Strategists to Make Better Client and Pricing Decisions

If you work independently, decision quality can matter as much as effort. One freelancer-focused source makes the point plainly: hard work alone is not enough. Decision quality and mindset matter too. Early calls can carry outsized consequences: saying yes to the wrong client, pricing fuzzy work as if it were clear, or continuing after key facts have changed.