Quick Answer

Build good strategy bad strategy for freelancers around verifiable controls, not motivation. Use three layers: compliance gates first, profit decisions second, and delivery stability third. In practice, that means keeping a presence log and trigger register, pricing from recent project evidence, and matching payments to invoices before moving money. If a rule is unclear, mark it as pending verification and check it before acting.

Beyond Good vs. Bad Strategy: The Freelancer's Operating System for Global Success#

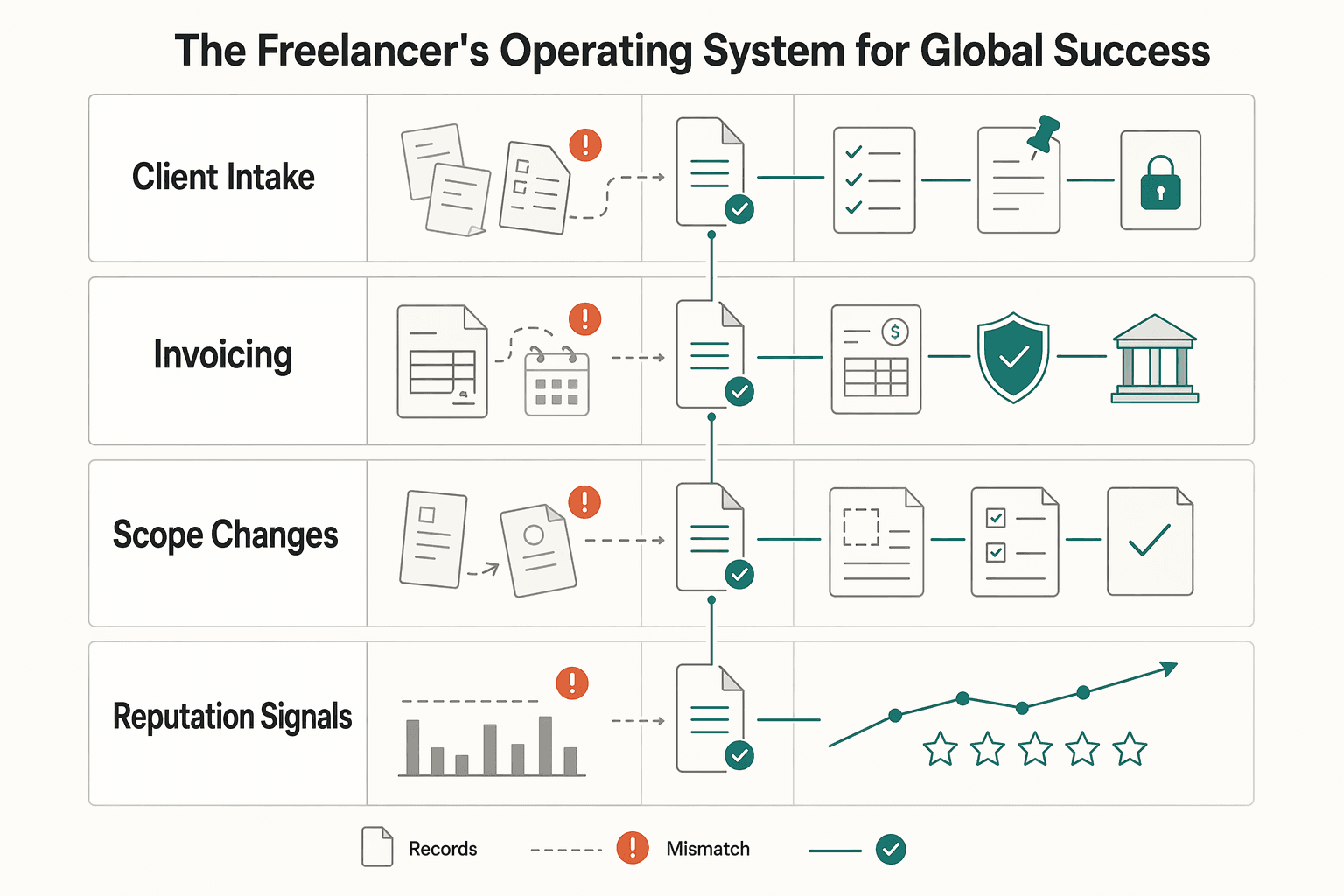

You do not need more resolutions. You need a system you can check under pressure, so intake, invoicing, scope changes, and client-facing signals do not depend on memory or mood.

For freelancers, the practical version of good strategy versus bad strategy is simple: replace intentions with verifiable gates. "I should be stricter" is not a system. "No work starts until the brief is approved, the invoice is issued, and the upfront payment has cleared" is.

| Moment | Reactive behavior | System-led behavior |

|---|---|---|

| Client intake | Starts after a promising call or chat thread | Confirms scope, contacts, approvals, and records what was agreed |

| Invoicing | Sends a bill after work is already moving | Uses one invoice pattern and checks payment status before kickoff |

| Scope changes | Absorbs "small extras" to keep things friendly | Logs the change, restates impact, and gets written approval |

| Reputation signals | Notices weak testimonials or stale portfolio pages too late | Reviews public proof regularly and fixes the first weak signal prospects will see |

One failure mode is starting without an advance and then not getting paid. One freelancer described that exact outcome, then switched to refusing projects without at least a 30% advance. That is not a universal standard. The useful lesson is to replace hope with a checkpoint you can verify.

Use that same mindset anywhere terms vary by jurisdiction, client location, or platform. Do not guess. Mark unclear thresholds as pending official-source, advisor, or platform-record verification, then note the date checked once confirmed. Keep your evidence pack outside your inbox memory: dated brief, approval trail, invoice, and payment record.

The rest of the article follows that logic. Tier 1 covers the gates to verify and document before work moves. Tier 2 covers profit protection through pricing, payment discipline, and scope control. Tier 3 covers delivery stability through repeatable admin and execution habits.

For deeper implementation on one common Tier 1 area, see GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients. Next action: read Tier 1 and pick one gate you will stop improvising this week. If you want a deeper dive, read Digital Nomad Health Insurance: A Comparison of Top Providers.

Tier 1: The Compliance Foundation - Your Shield Against Catastrophic Risk#

Treat compliance as a weekly operating discipline, not a year-end scramble. Your biggest risks are often routine: missed presence tracking, incorrect invoice treatment, and records you cannot produce when asked. Run four controls every week so small misses do not turn into expensive surprises:

| Control | Reactive behavior | Controlled behavior |

|---|---|---|

| Presence log | Rebuilds travel/work days from memory later | Updates dates, location, and countable status weekly; flags jurisdiction checks early |

| Trigger register | Discovers filing exposure at tax time | Maintains a live list of foreign accounts, countries, platforms, and rule-dependent items |

| Invoicing | Reuses old wording and assumes it still applies | Sends only after client details, treatment, and required checks are confirmed |

| Document retention | Leaves approvals, invoices, and receipts scattered | Stores contracts, invoices, receipts, payment proof, and review notes in one retrievable structure |

Your presence log is a control, not a diary. For U.S. tax purposes, substantial presence uses a current-year plus weighted 3-year test. It includes 31 days in the current year and 183 days over the 3-year period. Some days are excluded, so classification matters. UK guidance also includes an 183-day automatic residence trigger. That is why you should not treat "183 days" as a universal global rule.

Cross-border invoicing before you hit send#

Use a pre-send check that separates confirmed items from unresolved ones:

| Status | Item |

|---|---|

| Confirmed before sending | Client legal name and billing country |

| Confirmed before sending | Your registered business details |

| Confirmed before sending | B2B/B2C status |

| Confirmed before sending | Whether an invoice is required for that transaction type |

| Confirmed before sending | VAT-number status where relevant, including VIES checks for EU cross-border VAT numbers |

| Confirmed before sending | Supporting contract or scope on file |

| Pending until verified | Current VAT wording, pending confirmation from an advisor or the official source |

| Pending until verified | Member-state invoice field requirement, pending confirmation from the official source |

| Pending until verified | Local tax treatment pending advisor review |

Keep that separation strict. EU rules provide a common invoicing baseline, but member-state differences still exist. If a requirement is unresolved, pause and verify instead of guessing.

Ownership, evidence, and escalation#

Every control needs three things: an owner, an evidence location, and an escalation rule.

- Owner: you run weekly updates and first-pass checks.

- Evidence location: one system for presence logs, trigger register, invoices, contracts, receipts, deposit records, and payment confirmations.

- Escalation rule: escalate when a change could affect treatment, filing, or wording and you cannot verify it from a current primary source.

For U.S. persons, include FBAR in your trigger register. If foreign accounts exceed $10,000 in aggregate at any point in the year, track it. The due date is April 15, with an automatic extension to October 15.

Minimum viable setup for week one#

Start small, but make each control usable right away:

| Setup | Done means |

|---|---|

| Create a presence log and trigger register | Both have current entries, dates, and a clear confirmed versus pending verification field |

| Build one base invoice template and one pre-send checklist | Each invoice maps to a client record, scope document, and payment terms before send |

| Set up one evidence folder structure | For any active client, you can quickly retrieve the brief, approval trail, invoice, receipt, and payment record |

If you can do those three things this week, Tier 1 is live.

Once those controls are in place, use the same discipline to protect margin instead of just reducing risk. If you serve EU clients, the next practical step is tightening data handling and retention, since GDPR scope can apply even when your business is outside the EU when processing relates to offering goods or services to people in the EU. Use this implementation guide: GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients. Related: The Best Travel Insurance with Electronics Coverage.

Turn this compliance tier into a weekly habit by tracking where you worked and what needs verification in the Tax Residency Tracker.

Tier 2: The Profit Engine - From Defense to Offense#

Clean records should change your money decisions, not just tidy up your books. If you cannot see delivery cost, payment timing, and which clients absorb extra effort, your quotes, terms, and client mix may still be set more by pressure than evidence.

This is the midpoint of the system. Tier 1 reduced avoidable risk. Tier 2 uses the same discipline to improve commercial outcomes before you send a proposal or accept new work.

| Profit lever | Reactive behavior | Controlled behavior |

|---|---|---|

| Banking separation | Business and personal spending blur, so profit is guessed later | Business banking stays separate, and costs are attributable before profitability review |

| Record quality | Receipts, approvals, and costs are reconstructed after the fact | Revenue and cost records are detailed enough to trace what each project required |

| Receivables visibility | Late payment is noticed only when cash gets tight | Open invoices are reviewed regularly, so slow payers affect terms before the next quote |

| Project-level profitability | You remember whether work felt busy, not whether it paid well | Recent projects are reviewed for effort, revisions, expenses, and payment timing before repricing similar work |

The data that should change your decisions#

Good records matter only when they change a real choice. The most consequential choices are often what to quote, how to structure payment terms, and whether a client belongs in your core mix.

Before pricing, pull one comparable project and verify four items from records, not memory: original scope, scope changes after kickoff, effort or external cost to complete, and actual payment date. If you cannot retrieve those quickly, your quote may be anchored to urgency or client budget pressure.

A common failure mode is false confidence. Invoice value can look strong while revisions, admin drag, delayed payment, or unbilled extras reduce actual return. Good records expose that early.

Price from evidence, not nerves#

"Raise your prices" is incomplete unless you know what must be priced in. Use the same four-input test each time:

| Input | What to include |

|---|---|

| Cost to deliver | Your labor, subcontracting, software, travel, research, and likely revision time |

| Value delivered | The concrete result the client is buying |

| Scope-change risk | Brief clarity, stakeholder count, and feedback structure |

| Payment timing | Whether cash arrives in stages or long after delivery |

You do not need a perfect model. You need one that makes tradeoffs visible before proposal send. If scope risk is high, tighten scope or add change control. If payment timing is weak, change the structure, not just the fee. Urgency plus uncertain scope plus delayed payment is a compound risk.

| Pricing posture | Pressure-led | Evidence-led |

|---|---|---|

| Quote basis | Follows budget pressure or fear of losing the deal | Uses recent delivery cost, expected value, scope risk, and payment timing |

| Scope promise | Broad promises to speed approval | Specific deliverables, limits, assumptions, and change handling before signoff |

| Payment terms | Accepts vague or slow terms to avoid friction | Uses deposit, milestones, or due dates aligned to risk and cash exposure |

| Benchmark use | Forces proposals to fit generic market numbers | Uses your own recent data; external benchmark pending verification if needed |

External benchmarks can help, but they should not override your own records. If you use one, mark it as pending until verified.

Client mix is a profit decision too#

Client mix is a profit control, not just a marketing metric. If too much work comes from one platform, intermediary, or referral channel, convenience can hide weak terms.

A seven-year qualitative study in the ride-hailing sector found that many workers reported liking and finding choice under algorithmic management. The same abstract describes two tactic sets (engagement and deviance) and warns that "choice-based consent" can mask structurally problematic elements of work. Different sector, but a useful warning: easy access to work can make weak economics feel acceptable.

Review channels the same way you review pricing. If one source repeatedly brings rushed briefs, weak term control, or delayed payment, treat that as a profit warning, not just a full pipeline.

A short cadence before you quote#

A simple weekly cadence can be enough: reconcile income and expenses, review unpaid invoices, and compare recent completed projects against expected effort. Before you quote or accept new work, produce these three outputs without cleanup:

- Current unpaid-invoice view.

- Credible read on what similar work actually took to deliver.

- Short note on any client or channel with repeat friction.

If one is missing, pause. The proposal is not ready because the decision is not ready. That is how Tier 2 shifts from defense to offense: profit is designed at quote, terms, and client-selection time.

You might also find this useful: How to Build a Predictable Content Strategy for Your Agency.

Tier 3: The Automation Blueprint - Reclaiming Your Time and Autonomy#

At this stage, automation is about control. When records are fragmented across tools, cleanup work starts managing your time and decisions.

Tier 2 depends on this. Better pricing and terms do not hold if fragmented data, duplicate records, and unresolved exceptions keep pulling you back into admin.

Start with one source of truth#

Pick a primary business ledger as your final financial record. Every other tool should feed it instead of creating parallel records. A practical handoff pattern to audit on live projects:

- Intake: capture approved client and billing details once.

- Invoice: reuse those details and link the invoice to the agreed work.

- Payment: capture a usable payment reference.

- Ledger: match payment to the correct invoice and client.

If a recurring handoff depends on copy-paste from inboxes, chat, or memory, drift has usually started.

What controlled automation looks like#

| System behavior | Leakage pattern | Controlled rule | Expected outcome you can verify |

|---|---|---|---|

| Client and billing data capture | Same client details are re-entered across tools | Capture once in an approved record; reuse everywhere | Fewer record inconsistencies and less retyping |

| Invoice generation | Scope or terms rebuilt manually each time | Pull invoice details from the same approved work record | Billed work stays aligned with agreed work |

| Payment matching | Receipts identified by memory or inbox search | Match by invoice reference, amount, date, and payer details | Fewer unmatched payments |

| Reconciliation timing | Matching delayed until month-end cleanup | Update ledger as payments clear; review open items on a regular cadence | Earlier detection of gaps |

| Exception handling | Short, partial, or unclear payments pushed to "later" | Tag exceptions immediately and resolve against a named invoice or client | Exceptions stop compounding into close-period confusion |

Use a blunt replacement rule: if a tool repeatedly forces duplicate entry for client, invoice, or payment data in a recurring process, replace it, integrate it, or narrow its role.

Run cash handling in fixed order#

Cash handling is easier to control when the order stays consistent:

- Identify incoming payment.

- Match it to an invoice, or log it as an exception immediately.

- Update the ledger.

- Only then move funds between accounts, if you use separate balances.

When money lands, resolve it promptly or assign it as an exception with an owner and note. If payment is partial, short, missing reference details, or from an unexpected payer name, do not force-match. Tag it and resolve it against the invoice evidence in your next control cycle.

Protect reclaimed time with a regular checkpoint#

Reclaimed time disappears fast unless you defend it. Use a regular operating review (weekly is common) to keep control:

- Review open invoices and unmatched payments.

- Clear or tag every exception.

- Check for duplicate client records and invoices without project linkage.

- Confirm ledger entries match what actually cleared.

- Close admin and return to delivery.

If you use a tool-performance benchmark, verify the current figure from the official source before relying on it. This is the practical line between real automation and prettier chaos.

For a step-by-step walkthrough, see The 'Barbell Strategy' for a freelance career.

Your Business is a System, Not a To-Do List#

If your week keeps getting hijacked, the fix is not a better to-do app. The fix is a small system: diagnose one or two real challenges, set a guiding rule for each, and run a weekly action agenda that answers, "How are you going to do that?"

Start with observable signals from this week. Did client delivery push marketing off your calendar again? Did non-client work consume your best hours? Did unplanned requests keep pulling you off plan? Treat these as operating signals, not random bad days.

Keep the diagnosis concrete. Review your calendar, invoices, chat threads, and project notes. Name exactly where execution broke down, and capture one or two examples so you are not relying on memory or mood.

| If this happens this week | Reactive response | System response |

|---|---|---|

| Delivery crowds out marketing | Pause outreach until things calm down | Keep one small recurring marketing action on your calendar and review it weekly |

| The plan gets too complex | Add more tactics and hope one works | Simplify to a few repeatable actions you can execute consistently |

| Priorities turn into a wish list | Try to do everything at once | Focus on one or two key challenges and define coherent actions for each |

| Pipeline feels dry | Scramble for leads only when cash pressure spikes | Use a simple weekly checkpoint and repeat what consistently brings your best, easiest money |

The tradeoff is simple: complexity feels ambitious, but it usually breaks consistency. If you want a checkpoint, use a short review exercise and a few clear questions to test which actions are actually producing your best, easiest money. Use this weekly operating checklist:

- Name the one or two challenges that actually showed up.

- Write one guiding rule for each challenge.

- Turn each rule into clear actions for next week.

- Check those actions against your calendar, contract notes, and client messages before the week starts.

For related context, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

When you are ready to run this system in one operational flow, review Merchant of Record for Freelancers to confirm fit for your market and program.

Frequently Asked Questions

What is a good financial strategy for a freelancer?

A good financial strategy starts with one or two financial challenges you can actually address, then a clear action agenda for how you will execute. Pick your biggest pressure and write the few weekly actions that directly address it instead of adding more goals. Verify your pricing inputs, invoice process, and any filing triggers from official sources, advisor guidance, or platform records before you act.

How do you manage international tax compliance without living in spreadsheets?

Use a small operating record instead of a giant workbook. Maintain a dated presence log, a compliance tracker for where you invoice, and an invoice and contract checklist with consistent client and billing details. If relevant, keep a separate checklist for client-data requirements, such as GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients. Verify that each record includes a date and marks unconfirmed local thresholds as pending official-source or advisor verification.

What is the difference between freelancer tactics and business strategy?

Tactics are individual moves. Strategy is the design that combines policy and action to solve a high-stakes challenge. Rewrite any goal-only plan so it explicitly answers, “How are you going to do that?” Then verify that your weekly actions map to one or two key challenges instead of a wish list.

How do you avoid burnout without just telling yourself to work less?

Simplify your routine so it can stay consistent even when work is busy. Keep one repeatable marketing action running each week so you do not stop completely and then scramble for work later. Verify that your weekly plan is simple enough to maintain during delivery-heavy periods.

What is the most critical risk when you work across borders?

A common risk is letting your records fall out of sync with how you are actually working across locations. Before a trip, long stay, or new foreign client, update your presence log, review your compliance tracker, and check invoice and contract details for location and payor consistency. Verify that unclear local triggers are marked pending verification before work starts.

How should you think about pricing?

Start with analysis, then apply judgment. Calculate production cost, check market pricing, and ask enough questions to understand budget context. Then present the proposal live before sending it so scope questions can be handled in real time. Verify that your written proposal captures scope, assumptions, and a clear process for scope changes so questions can be handled quickly.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- europa.eu/youreurope/business/taxation/vat/index_en.htmtrusted

- grants-neubauercollegium.uchicago.edu/data/uploaded-files/default.aspx/youtube_aut...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC7282833trusted

- success.uark.edu/academic-initiatives/writing-guides.phptrusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-businesses/invoicing_entrusted

- consultingquest.com/insights/manage-tail-spend-in-consultingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Digital Nomad Health Insurance Comparison for Long-Stay Moves

Use focused time now to avoid expensive mistakes later. Start with a practical `digital nomad health insurance comparison`, then map your route in [Gruv's visa planner](/tools/visa-for-digital-nomads) so we anchor policy checks to your real plan before pricing pages pull you off course.

The Best Travel Insurance with Electronics Coverage for Remote Workers

Electronics coverage problems often start before the trip, not only after damage happens. Many trace back to purchase-stage choices: broad labels read as guarantees, eligibility details entered too quickly, or exclusions ignored until a claim is active. If a denied claim would interrupt your income, choose clarity over price from day one.