Quick Answer

Start by treating cognitive dissonance for freelancers as a workflow alert: map your last three projects from client yes to payment, then fix the first missing link in action, document, owner, or status. Use one repeatable handoff order for contract, kickoff, and invoice, and label unconfirmed legal or tax requirements for follow-up instead of guessing. This turns stress into concrete operational fixes and reduces payment friction.

Why 'Mindset Hacks' Fail the Modern Business-of-One#

If the same stress keeps returning, treat it as an operations signal first, not a personality flaw. The tension is usually simple: you see yourself as reliable and established, but your business still runs on memory, inbox search, and last-minute improvising.

That gap usually shows up in ordinary places. A client says yes, but the proposal does not hand off cleanly to contract, kickoff, and invoice. You rewrite scope because the original assumptions were never captured. Billing slips a week because nobody owns the admin step, even if "nobody" is still you. Payment friction is common in small businesses, and late payment can strain liquidity. In U.S. federal contracting, FAR 32.905 ties payment to a "proper invoice," and a noncompliant invoice must be returned within 7 days. Your client work may not follow that rule, but the lesson still applies: incomplete documents slow cash.

| Response | Repeatability | Client experience | Risk of recurrence |

|---|---|---|---|

| Mindset-only coping | Low if each job needs fresh self-talk | Can feel uneven when follow-up depends on your mood | High because the stressor stays in place |

| Process redesign | Higher because steps are written, owned, and checkable | More consistent handoff after approval | Lower because you changed the source of friction |

| Stress-driven overwork | Looks productive, but depends on unsustainable effort | Fast at first, then delayed or sloppy when fatigue hits | Very high; chronic stress and sustained 55+ hour weeks are associated with higher health risk |

Use this checkpoint the next time an opportunity appears:

- Documented: Is the next step written down, including the exact document or template you will use?

- Owned: Is it clear who sends it, when, and what "done" looks like?

- Executable: Could you complete it today without inventing terms, hunting files, or asking for basics twice?

If any answer is no, do not call the tension a mindset problem yet. You have found the signal. The next step is to locate where the chain actually breaks.

If you want a deeper dive, read A freelancer's guide to Thinking.

Diagnosing Your 'Identity vs. Reality' Gap#

If stress keeps returning after a client says yes, treat it as a workflow signal first. For freelancers, that discomfort usually means your stated standard and your actual process are out of sync, and avoidance can hide the exact step that is breaking.

Audit the path from yes to paid#

Use your last three projects and trace each one from approval to payment. At each step, log only: repeatable action, document, owner, and status (working, missing, Current requirement pending verification).

| Step | What to capture (4 fields) | Output |

|---|---|---|

| Approval | How you record client yes, approval record, owner of next action, status | Friction log entry when scope/terms changed after yes |

| Contract + kickoff | Contract, kickoff checklist, required inputs, owner, status | Missing-document list with one named owner per gap |

| Invoice + tax setup | Invoice template, requested tax form response, owner, status | Exact gap list (for example: missing W-9, W-8 BEN, or payment term field) |

| Payment follow-up | Payment date rule/mechanism, reminder owner, payment confirmation, status | Next fix with date (for example: update contract payment clause or reminder timing) |

If it is not written, saved, and owned, mark it missing. If a requirement may apply but is unconfirmed, mark Current requirement pending verification so you do not guess.

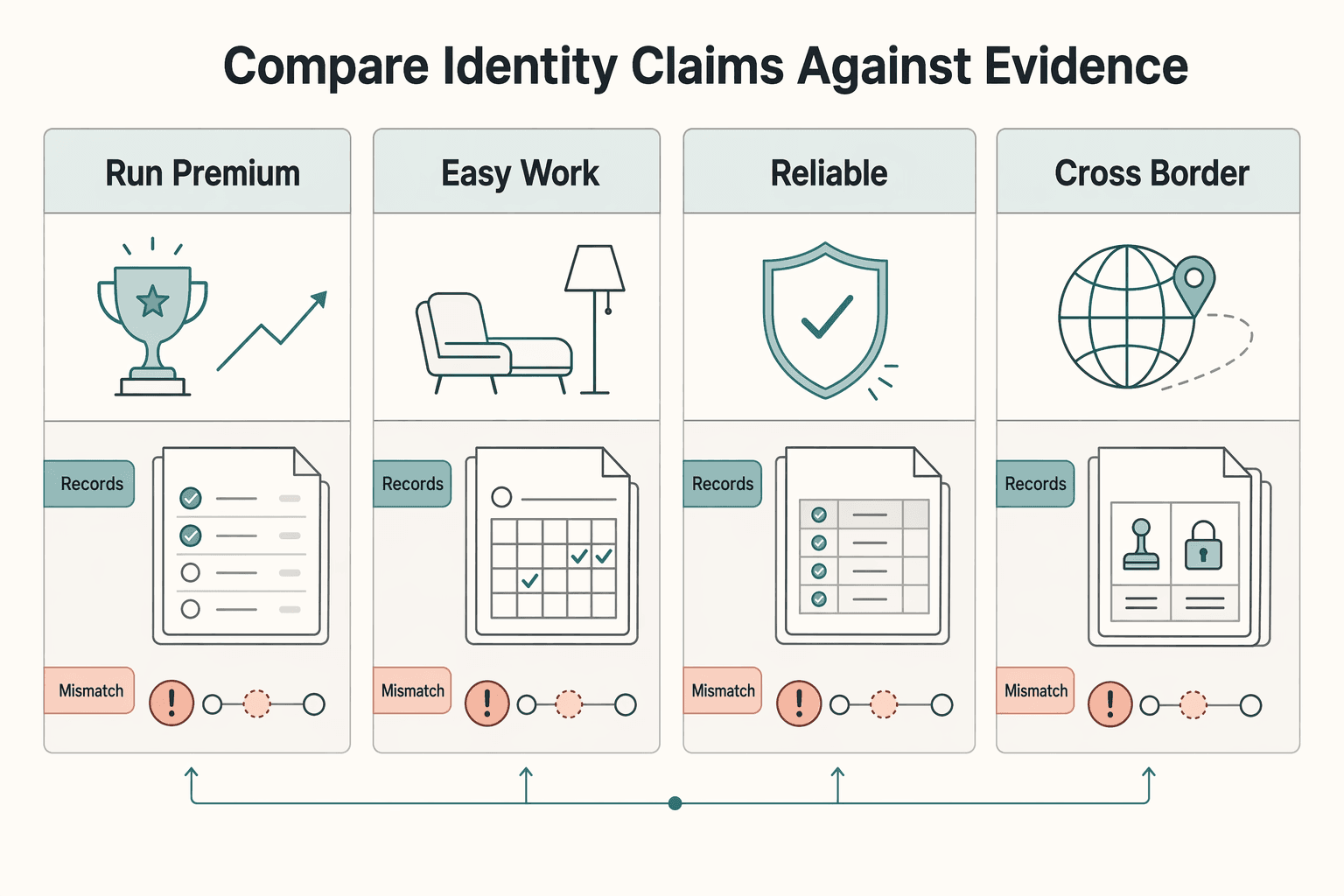

Compare identity claims against evidence#

| Identity claim | Evidence you can verify now | Business consequence when missing | Immediate correction |

|---|---|---|---|

| "I run a premium service." | Invoice and payment terms are ready before delivery starts | Payment friction and correction loops | Finalize invoice + payment terms in your standard pre-work packet |

| "I am easy to work with." | Same handoff order every time: contract, kickoff details, timeline, first invoice | Uneven client experience and avoidable follow-up | Lock one handoff sequence and reuse it |

| "I am reliable." | Scope, dates, and changes are retrievable from current records | Rework, disputes, and slower approvals | Store project decisions in one consistent location |

| "I am cross-border ready." | Correct tax form path and VAT handling are documented or flagged for verification | Withholding, invoicing delays, and compliance risk | Confirm payer request and document path before invoicing |

Two mismatch patterns to fix first#

The payment-experience gap is usually the fastest win. Late payment can harm liquidity, so if terms or invoice details are still being assembled after work starts, fix that sequence first. If New York Article 44-A applies to the engagement, verify the written contract includes a payment date or a mechanism to determine it; if timing is not specified, payment is due no later than 30 days after completion.

| Scenario | Article note |

|---|---|

| New York Article 44-A timing | Verify the written contract includes a payment date or a mechanism to determine it; if timing is not specified, payment is due no later than 30 days after completion. |

| Form W-9 | If a payer requests it, use Form W-9 to provide the correct TIN. |

| Form W-8 BEN | Foreign payees asked by a payer or withholding agent should submit Form W-8 BEN. |

| Backup withholding | If required TIN details are not provided correctly, backup withholding can apply at 24%, including payments reported on Form 1099-NEC. |

| EU B2B VAT | For many EU B2B service cases, the customer accounts for VAT through reverse charge, but confirm before invoicing. |

The cross-border-readiness gap is next. Keep an evidence pack ready: client legal name, country, business/public-authority status, requested tax form, and VAT note to verify. If a payer requests it, use Form W-9 to provide the correct TIN; foreign payees asked by a payer or withholding agent should submit Form W-8 BEN. If required TIN details are not provided correctly, backup withholding can apply at 24%, including payments reported on Form 1099-NEC. For many EU B2B service cases, the customer accounts for VAT through reverse charge, but confirm before invoicing.

Mini-audit before you move to fixes#

- Trace three recent projects from yes to paid.

- Mark each step with

action,document,owner,status. - Save one proof pack: approval record, contract, invoice, tax form response, payment confirmation.

- Tag each gap as

operating standard,pricing/payment chain, orrisk/compliance control.

If you are tightening risk controls too, see The Best Antivirus and Malware Protection for Freelancers.

Your 3-Pillar Framework for Aligning Reality with Identity#

After your audit, fix the gap by making your business easier to prove than to explain. Use three pillars: a written operating standard, one linked pricing-to-payment chain, and risk controls managed as rules plus repeatable habits.

| Pillar | Core idea | What the section says to do |

|---|---|---|

| Written operating standard | Standardize what happens after a client says yes | Document scope, boundaries, ownership, document location, and unresolved requirement notes. |

| One linked pricing-to-payment chain | Treat pricing, invoicing, and compliance as one chain | Tie pricing to written scope, use a standard invoice template, and collect payer entity details, tax-form requests, and jurisdiction notes at intake. |

| Risk controls managed as rules plus repeatable habits | Separate policy from procedure | Set review cadence, attach one habit per rule, and verify evidence exists. |

Pillar 1#

Standardize what happens after a client says yes. Recordkeeping is a core business obligation, and it only works if your system clearly shows income, expenses, and supporting documents.

Use this operating-standard checklist:

- Scope: document deliverables, assumptions, exclusions, and change-request handling before work starts.

- Boundaries: define response times, revision limits, dependencies, and pause conditions.

- Ownership: name who sends the contract, kickoff, invoice, and tax or billing responses.

- Document location: keep the current proposal, signed agreement, kickoff notes, invoice template, and client-specific requirements in one searchable location.

- Unresolved requirements: if a requirement depends on jurisdiction, payer status, or tax treatment, mark it

Current requirement pending payer, official, or counsel verification.

In cross-border work, this prevents guesswork. If a U.S. payer requests Form W-9, the purpose is to provide the correct TIN for information reporting. If payment involves a foreign person, the documentation path can differ, and nonemployee compensation paid to nonresident aliens can be reported on Form 1042-S.

Pillar 2#

Treat pricing, invoicing, and compliance as one chain. That is how your client experiences it.

| Trigger | Failure mode | Corrected process | Immediate client-facing result |

|---|---|---|---|

| Scope shifts after approval | Repricing happens in scattered email threads, so the invoice no longer matches approved terms | Tie pricing to written scope, assumptions, and change handling before delivery starts | The client sees one consistent line from approval to invoice |

| Work is delivered before invoice details are ready | Invoice is assembled from memory, required fields are missed, or sending is delayed | Use a standard template with business details, client billing details, terms, and a unique identification number where required | Faster invoice turnaround with fewer clarification emails |

| Tax or jurisdiction details are requested late | Payment pauses while you gather TIN details, W-9 data, or VAT treatment | Collect payer entity details, tax-form requests, and jurisdiction notes at intake; mark unknowns as Current requirement pending payer, official, or counsel verification | Faster, clearer compliance responses and fewer last-minute holds |

If these steps are split across disconnected tools or moments, pressure returns. One concrete risk: backup withholding at 24% on reportable nonemployee compensation when required TIN conditions are not met.

Pillar 3#

Separate policy from procedure. Policy is the rule you commit to. Procedure is how you execute it. When a control is weak, check which part failed first: the rule, the habit, or the evidence.

| Jurisdiction example | Retention or limitation note |

|---|---|

| U.S. / IRS Topic 305 | General 3-year assessment limitation. |

| UK self-employed | Keep records for at least 5 years after the 31 January submission deadline. |

| Canada | Generally requires six years. |

Start here:

- Write the rule: set review cadence for cash visibility, invoice follow-up, estimated-tax checks, record retention, and coverage decisions.

- Attach one habit per rule: for example, a weekly money-in versus money-out review, a monthly estimated-tax check if you expect to owe $1,000 or more, and saved copies of approvals, invoices, and payment confirmations.

- Verify evidence exists: supporting documents should be available for purchases, sales, and other business transactions; if a document is missing, treat that control as weak.

Do not treat jurisdiction examples as universal rules. IRS Topic 305 notes a general 3-year assessment limitation; the UK requires self-employed records for at least 5 years after the 31 January submission deadline; Canada generally requires six years. Apply the rule that fits your jurisdiction, label it clearly, and review it on schedule.

Once you identify your weakest pillar, use the FAQ next to decide implementation order and review cadence. You might also find this useful: The Best Calendar and Scheduling Apps for Freelancers.

Conclusion: Stop Managing Dissonance. Start Engineering Certainty.#

Treat cognitive dissonance for freelancers as an operations signal, not a personality verdict. If the same stress keeps showing up around pricing, invoicing, or compliance, stop interpreting it and start checking the business artifacts that should already exist. Your next move should be concrete, and different for each pillar:

- Standardize the handoff. On your next signed job, make sure the same four items are easy to find without digging through old email: signed terms, current scope, invoice draft, and payer details. If one is missing, fix that step before you change your offer or your rates.

- Close each job with an assumption log. Mark each item as confirmed, unresolved, or verified and dated. Use

Current threshold pending official or counsel verificationanywhere a numeric legal or tax trigger is still unknown instead of guessing or leaving the field blank. - Keep a real evidence pack. Save the documents that support what you billed, earned, paid, or deducted. If you work in the US, IRS record rules are one reason this matters: standard cases often point to 3 years, while employment tax records require at least 4 years, and retention varies by scenario.

Before you change a price, delay an invoice, or ignore a compliance task, ask one question: what observable evidence says this is the right move? If the answer is not in recent project records, your current template, or a verified requirement, you are probably reacting to discomfort, not facts. Strong intent is not enough. An if-then plan often works better: if a requirement is unclear, tag it, verify it, date it, then proceed.

Keep the cadence simple: weekly, clear unsent invoices and unresolved tags; monthly, update templates and review risk items like tax set-asides; at project close, file the full record. If your unresolved list includes EU client data handling, see GDPR for Freelancers: A Step-by-Step Compliance Checklist for EU Clients.

For stress-management support alongside this workflow, see The Best Meditation and Mindfulness Apps for Freelancers.

Frequently Asked Questions

What should you fix first when everything feels misaligned?

Start by acknowledging the disconnect instead of denying it, then fix the first step where you keep improvising after a client says yes. If your core workflow does not happen in a consistent order each time, tighten that process before you touch anything else. Your check is simple: can you find the current agreement, scope, and next payment step without digging through old email?

Is cognitive dissonance for freelancers really just low confidence?

Usually not. If you are the owner-operator, a useful test is whether you are reasoning about business profit or only about getting the work done. When working right now feels dissonant, treat that as an operating signal first, then decide which part of the business needs attention. | Symptom | Immediate operational move | Follow-up check | Verification note | | --- | --- | --- | --- | | Your schedule keeps slipping | Add larger time buffers and rescheduling flexibility for yourself and clients | Check whether your current timelines and pause points are written down clearly | Current requirement pending verification | | Working less is reducing income | Decide now whether you are cutting costs, sharing costs, or drawing on savings | Check whether your near-term cash and payment plan is written down, not held in memory | Current requirement pending verification | | You cannot sustain the current pace | Reduce commitments before accepting more work | Check whether you can pause new starts cleanly without confusion | Current requirement pending verification |

How do you handle pricing without turning it into a confidence test?

Start with capacity and cash, not self-belief. If reduced workload means reduced earnings, make that tradeoff explicit before you change pricing or commitments. Then align your written scope and billing steps so your plan stays consistent from agreement to payment.

What if invoicing is the step you keep avoiding?

Shrink the next action until it is mechanical. Open your invoice workflow, complete the key details you already have, and send the draft the same day. If you keep delaying because required information is unclear, that points to an upstream process gap, not just an invoicing gap.

How much compliance work do you need to do upfront?

Do enough upfront to avoid preventable payment delays, and label unknowns instead of guessing. Collect required payer details early, confirm unclear requirements before finalizing, and keep Current requirement pending payer, official, or counsel verification where the answer is still uncertain.

What do you do when stress makes all of this harder to keep up with?

Protect capacity and fix one bottleneck at the same time. Add more buffer than feels necessary, because chaotic periods usually need more rescheduling room than you expect. Then choose one process to stabilize this week and run it consistently.

Do you need to take time off, or should you push through and stay billable?

Do not answer that from panic. Review your cash position, open commitments, and available flexibility first, then check whether you can access leave or whether you need to rely on savings. Leave availability depends on your work setup and options, so verify what applies before you act.

How often should you review this so it actually sticks?

Use a cadence you can keep even during a rough month. Review the same few items each time: current commitments, cash pressure, unsent invoices, and any note marked Current requirement pending verification. This week, pick one weak pillar, update one document, and run it on the next client from start to payment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- dol.ny.gov/freelance-isnt-free-acttrusted

- irs.gov/businesses/small-businesses-self-employed/es...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- nysenate.gov/legislation/laws/GBS/1412trusted

- nysenate.gov/legislation/laws/GBS/1411trusted

- psnet.ahrq.gov/primer/checkliststrusted

- sba.gov/business-guide/manage-your-business/manage-y...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

GDPR Compliance Checklist for Freelancers Working With EU Clients

Start by separating the decisions you are actually making. For a workable **GDPR setup**, run three distinct tracks and record each one in writing before the first invoice goes out: VAT treatment, GDPR scope and role, and daily privacy operations.

Thinking, Fast and Slow for Freelancers Who Want Better Clients

Treat thought leadership as risk control for your business, not just a visibility tactic. The real shift is from fast, reactive client chasing to slower, deliberate asset building. You publish to reduce risk before the next dry month, pricing call, or bad-fit project shows up.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.