Quick Answer

Yes - if you sell qualifying B2B services from outside France to a VAT-identified French business, tva in france is usually handled by autoliquidation, so you generally issue the invoice without charging VAT. Confirm the client VAT ID in VIES, ensure contract and billing entities match, and use approved reverse-charge wording on the invoice. If any classification point is uncertain, pause before sending and confirm treatment.

The Autoliquidation Strategy: Why You (Probably) Don't Need to Register for French VAT#

If you are non-resident and provide qualifying B2B services to a client that is VAT-identified in France, start with autoliquidation, not French VAT registration. In that default case, you generally do not charge French VAT on the invoice. The client reverse-charges it.

French guidance describes this as the general rule when the conditions are met. A foreign company not based in France is generally not liable for French VAT if the customer is identified for VAT in France and that customer accounts for the VAT. This also aligns with the EU Article 44 B2B framework. Under that framework, VAT is payable by the recipient when the supplier is not established there.

Quick self-screen#

This default works only if all three points are true. If any one is unclear, do not assume reverse charge.

| Check | Requirement |

|---|---|

| Permanent establishment | You do not have a permanent establishment in France. |

| Client VAT status | Your client is a taxable business and is identified for VAT in France. |

| Service rule | Your service falls under the general B2B place-of-supply rule and not a derogatory exception. |

Default path and exception path#

| Path | When it fits | What it usually means |

|---|---|---|

| Default path | Non-established supplier, no French permanent establishment, client VAT-identified in France, qualifying B2B service | Client reverse-charges VAT; you generally do not register for French VAT for that transaction. |

| Exception path | Buyer is an individual, entity, or business not identified for VAT in France for a French-taxable transaction | You may need French VAT registration and CA3 VAT returns. |

| Confirm-with-a-pro path | You have a French permanent establishment, or the service may fall under a derogatory place-of-taxation rule | Confirm treatment before invoicing. |

What to verify before invoicing#

Before you rely on autoliquidation, check three things in order.

| Order | What to verify | Section detail |

|---|---|---|

| First | Client's VAT number in VIES | If the VAT ID does not validate, pause before issuing a no-VAT invoice. |

| Second | Transaction type | Some services follow derogatory place-of-taxation rules, so cross-border B2B status alone is not enough. |

| Third | Invoice wording | Make sure your invoice includes the required reverse-charge statements for intra-Community services, and use wording that matches the transaction. |

Check them in that order: validate the client's VAT number in VIES, confirm the service does not fall into a derogatory place-of-taxation category, and make sure the invoice wording matches the transaction rather than a generic template.

Once you are in the default path, focus on verifying client status and issuing a compliant invoice rather than collecting French VAT for that transaction. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

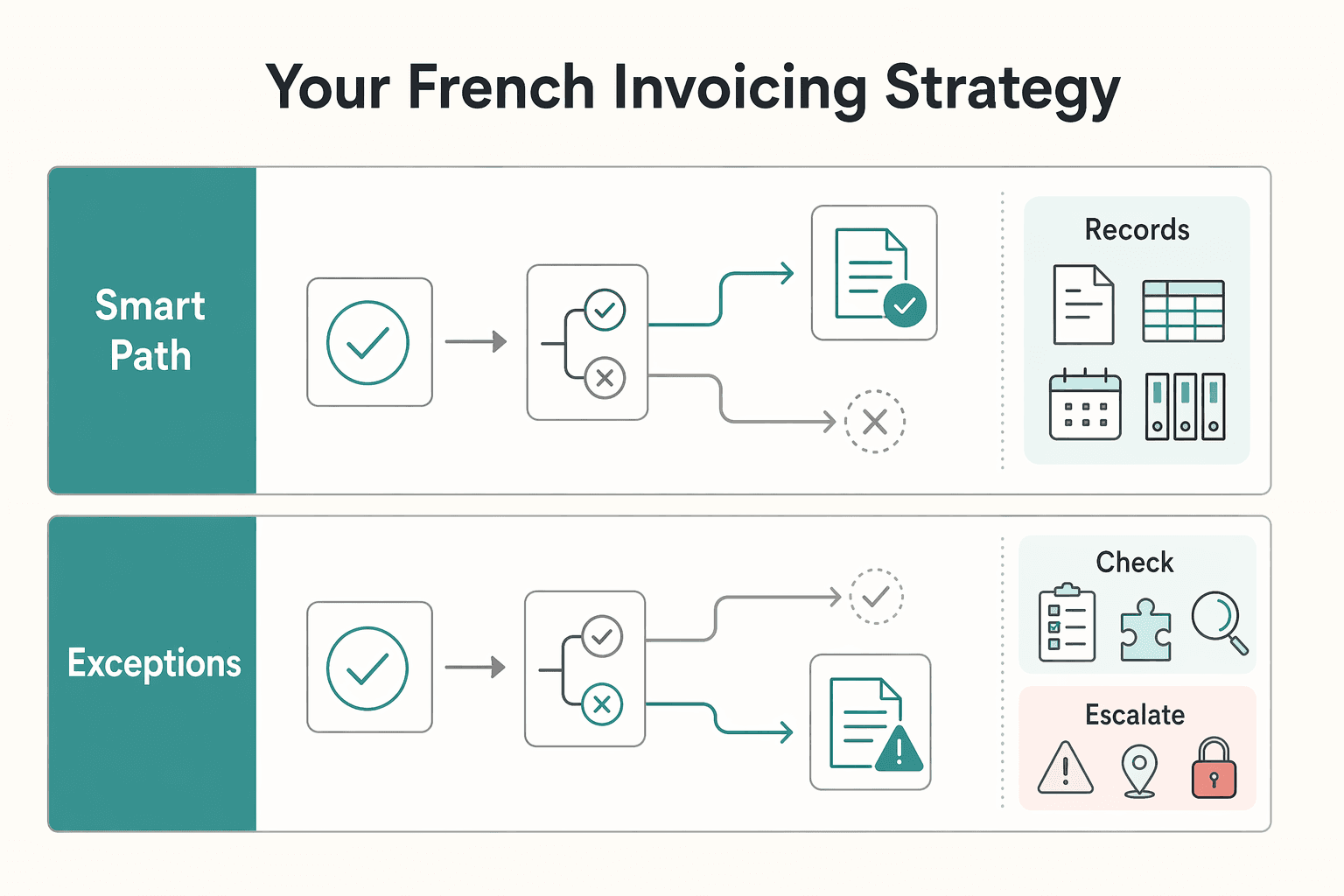

The Smart Path vs. The Hard Path: Your French Invoicing Strategy#

Make the VAT call first. Then ask whether France's domestic reform changes how the invoice has to move. Use a two-lane decision: keep your normal invoicing process unless this transaction is actually in scope for France's domestic reform. Match the process to the facts of this deal, not to every France-related rule in circulation.

| Path | Required actions | Ongoing obligations | Error exposure | Admin load | When this path is actually appropriate |

|---|---|---|---|---|---|

| Smart path | Confirm client and transaction facts, apply the VAT treatment you already validated for this deal, and keep supporting records | Re-check when client status, service type, or transaction pattern changes | Medium if classification is wrong; low when facts are clear and documented | Low | Cross-border invoicing that is not in scope for France's domestic B2B e-invoicing flow |

| Hard path (exception lane 1) | Confirm whether you are in scope for domestic B2B e-invoicing in France and set up accredited-platform routing (often labeled PA or PDP) | Receive and exchange in-scope domestic B2B invoices electronically; receiving obligations are described as starting in September 2026 | High if you prepare late or route outside the accredited network | Medium to high | Domestic B2B between VAT-registered entities established in France |

| Hard path (exception lane 2) | Confirm whether the transaction is in France's e-reporting scope and set up transaction/payment data handling | Continue reporting required data for in-scope flows | Medium to high if e-reporting is confused with e-invoicing or payment data is missed | Medium | B2C and certain cross-border transactions that fall into French e-reporting scope |

What usually matters most#

The key question is scope: does the invoice belong in France's domestic reform at all? This reform is an operating-model change through accredited platforms, not just a file-format update. Once you are in scope, routing, platform setup, and data handling become the core compliance work.

A practical check helps. If both parties are VAT-registered and established in France for a domestic B2B invoice, assess the e-invoicing lane. If the flow is B2C or an in-scope cross-border case, assess e-reporting instead.

Keep an evidence pack, not just an invoice#

Keep a short file showing why you chose this lane: client identifiers, contract or SOW, issued invoice, and your classification note. If a client asks about PA or PDP connectivity, keep that exchange too, because market materials still use both labels.

Late setup is a common failure mode. Current reform summaries flag ERP, data, and partner-process risk when teams delay preparation. If you can, run a pilot phase to test real workflows before go-live and reduce disruption.

Decision checkpoint#

Pause before you invoice if any core fact is unclear: client status, transaction type, or service classification. If those facts are not solid, get local tax advice before you lock in the invoicing lane.

Related: Can Digital Nomads Claim the Home Office Deduction?.

Why French VAT Thresholds Are a Distraction#

Once you separate the reverse-charge question from domestic-threshold noise, threshold hunting is usually a distraction. If you are a non-resident supplying B2B services to a French VAT-registered company, domestic French turnover thresholds are usually not the main decision point.

The practical question is whether this deal fits the reverse-charge lane, where your client handles VAT, or whether your facts have shifted into a case that needs deeper registration analysis.

Threshold hunting often pushes people into the wrong admin stack. If you assume registration too early, you can end up charging French VAT, filing regular Déclaration de TVA returns, and potentially dealing with fiscal-representative exposure, even when reverse charge was the intended path.

Quick scope check#

Before you focus on TVA thresholds, classify the deal on four facts:

- Are you a non-resident supplying services from outside France?

- Is this B2B or B2C?

- Is the client VAT-registered or not?

- Is this a straightforward B2B service case, or a fact pattern that needs deeper registration analysis?

If your answers are non-resident, B2B, and VAT-registered client, your default lens is reverse-charge eligibility, not domestic small-business thresholds.

| Signals that point to reverse-charge workflow | Signals that trigger deeper registration analysis |

|---|---|

| You supply services from outside France | The facts do not clearly match a non-resident B2B service case |

| Your client is a French business acting as a VAT-registered customer | Your client is not VAT-registered, or the deal is not clearly B2B |

| The transaction is a straightforward B2B service sale | The transaction mix is changing, or you have mixed B2B and B2C flows |

| Your invoice can include reverse-charge wording and show no VAT charged | You are considering charging French VAT (including a 20% hard-path approach) |

Practical checkpoint: if you stay in the reverse-charge lane, your invoice should include reverse-charge wording and should not charge VAT. Keep a short internal note on why the client qualified as VAT-registered and why the transaction fit that lane.

If your case does not clearly fit this pattern, verify any current threshold before you use it and confirm the treatment with a French VAT adviser. You might also find this useful: A Deep Dive into France's 'Crédit d'Impôt Recherche' (CIR) Tax Credit.

Your Bulletproof Checklist for Invoicing a French Client#

For the standard non-resident B2B service case, simpler is safer: issue a reverse-charge invoice under autoliquidation de la TVA and do not charge VAT. Use this checklist to confirm that treatment before you send.

| Step | Focus | Key action |

|---|---|---|

| 1 | Confirm the transaction still fits the reverse-charge lane | Write a short internal note explaining why you are treating this invoice under reverse charge. |

| 2 | Confirm client business details and keep a record | Confirm the client legal entity details and VAT number used for invoicing, then keep a dated record of the checks you ran in your workflow. |

| 3 | Build the invoice from a field checklist | Build the invoice field by field and review it before sending. |

| 4 | Check reverse-charge consistency | Confirm the tax statement, service scope, and totals all point to the same treatment. |

| 5 | Use an exceptions stop-sign, then run final QC | If client status or transaction scope is still unclear, do not issue the invoice. Get VAT advice first. |

1. Confirm the transaction still fits the reverse-charge lane#

Start with the classification, not the template. Check that you are supplying services from outside France, that the client is a French business, and that the engagement is clearly B2B and service-based.

Action: Write a short internal note explaining why you are treating this invoice under reverse charge. If anything is mixed or unclear, pause and clarify before drafting.

2. Confirm client business details and keep a record#

Do not treat client details as a formality. Clear records support a consistent no-VAT invoice process.

Action: Confirm the client legal entity details and VAT number used for invoicing, then keep a dated record of the checks you ran in your workflow.

Output: Keep the record with the invoice file. If client details are inconsistent, stop and resolve them first.

3. Build the invoice from a field checklist#

Once the classification and client details are confirmed, build the invoice field by field and review it before sending.

| Field group | Include | Double-check before sending |

|---|---|---|

| Supplier identity | Your business name and address | Matches contract, bank details, and prior invoices |

| Client identity | Client legal name, address, and VAT number used for invoicing | Legal entity matches your contract counterparty and internal records |

| Service detail | Specific services and period or milestone covered | Clear enough for accounts payable approval |

| Tax treatment label | Approved reverse-charge statement, inserted after legal review | Wording is current and approved, not copied from memory |

| Totals | Net amount due, VAT not charged, final amount payable | No VAT added by template or software defaults |

The goal is a complete invoice with no internal mismatches.

4. Check reverse-charge consistency#

This is the last content check before the invoice leaves your hands.

Action: Confirm the tax statement, service scope, and totals all point to the same treatment. If reverse charge is stated, VAT is not charged, collected, or remitted by you, and the invoice reflects that consistently.

Any contradiction, such as reverse-charge text plus VAT in totals, should be fixed before sending.

5. Use an exceptions stop-sign, then run final QC#

A short final review catches most avoidable errors.

Action: Ask one final question: is client status or transaction scope still unclear? If yes, do not issue the invoice. Get VAT advice first.

Output: Run a two-minute pre-send review for legal entity match, clear service description, reverse-charge statement inserted, VAT not charged, and accurate totals. This final pass helps reduce avoidable rejections and payment delays.

For a step-by-step walkthrough, see A Deep Dive into the US-France Tax Treaty for Freelance Performers.

Before you send your next invoice, run the client VAT ID through Gruv's VAT number validator and keep the result in your records.

Three Hidden Risks to Avoid#

Use this as a pre-send risk check: a clean invoice matters, but formatting will not rescue a transaction that is sitting in the wrong VAT lane.

Risk 1#

Eligibility is the first gate, and it is where many mistakes start. Before you assume autoliquidation applies, confirm the transaction facts and counterparties through official records and your contract documents.

Verify these points before invoicing:

- Confirm the client tax-status details using your normal official validation route.

- Match the legal name and entity details to the contract counterparty and billing entity.

- Keep dated proof of the check in your compliance file.

If those elements do not line up, pause and resolve the mismatch before issuing the invoice.

Risk 2#

Entity setup changes the reporting picture, so do not borrow assumptions from the wrong structure. Invoicing France from a non-EU entity can be treated differently from invoicing through an EU entity, even when the commercial work looks identical.

| Setup | Who reports what | Where it is reported |

|---|---|---|

| Non-EU entity invoices French client directly | Confirm facts, document your VAT treatment, and avoid importing EU filing assumptions by analogy | Keep a clear internal record; any France-side treatment depends on confirmed transaction facts |

| EU entity invoices French client | Check that entity's VAT reporting obligations; use a CBR path if the case is complex | In the participating EU country where that entity is VAT-registered (CBR requests are filed there) |

| EU small enterprise using the cross-border SME scheme | Confirm eligibility, file prior notification, obtain EX number before exemption, then file ongoing turnover reporting | In the Member State of establishment (MSEST), including one quarterly report covering turnover in all 27 Member States |

For SME cross-border scheme use, keep the hard limits and sequence intact. Union turnover must not exceed EUR 100 000. Exemption starts only after the EX number is granted and confirmed for the selected Member State. The process target is up to 35 working days, with possible delay when extra anti-evasion checks are needed.

Also keep two boundaries clear. OSS references here are for cross-border B2C e-commerce, including the 1 July 2021 change and EUR 10 000 EU-wide threshold. CBR is the route for complex cross-border VAT treatment questions. If multiple companies are involved in a CBR request, one company files on behalf of the others, and France is listed among participating countries.

Risk 3#

Poor invoice detail creates friction even when the tax treatment is right. Vague descriptions slow payment and weaken your audit trail.

| Weak description | Strong description |

|---|---|

| Consulting services | Market-entry advisory for France, covering discovery workshop, pricing memo, and final action plan tied to the agreed period |

| Software development | Delivery of milestone-based integration work under the signed SOW, with versioned handoff and client acceptance noted |

| Design work | Campaign asset package delivered under the approved PO, listing deliverables and delivery period |

Strong descriptions do three jobs: they help accounts payable approve faster, tie the invoice to the contract, SOW, or PO, and leave a record you can defend later. Keep the wording practical: period, deliverable, milestone, or acceptance point.

Escalate to a tax professional instead of relying on defaults if your setup is mixed, you changed entities mid-engagement, or the client VAT status is unclear. Do the same if bundled cross-border services create unclear sourcing or reporting consequences.

We covered this in detail in Health Insurance for Freelancers in France During Your First Year.

From Compliance Anxiety to Professional Control#

The goal is not to memorize every French VAT rule. It is to run the same checks every time before you issue an invoice. In this context, that means confirming the client is a taxable business, applying reverse-charge wording for qualifying cases, and sending only a complete invoice.

For qualifying Article 196-type services, VAT is due by the customer. French rules align with that when a non-established supplier invoices a taxable customer in France.

Use VIES as a yes-or-no status check for the client entity. The VAT information is either valid or invalid. If the VAT number, contract entity, and invoiced entity do not match, stop and resolve that before sending.

| Reactive habit | Professional control |

|---|---|

| No pre-send checks | Run a pre-send checklist: confirm the client is an assujetti à la TVA, validate the VAT number in VIES, and match that VAT identity to the legal entity on the contract and invoice |

| Generic invoice text | Use your approved reverse-charge template and include the required mention "Autoliquidation" for qualifying cases |

| No records | Keep the VIES check result you relied on (when available) and the final invoice copy in your compliance file |

| Informal fixes after a client or AP flag | Follow a formal correction path: issue a facture rectificative first, and if a French VAT return was already filed for that period, submit a déclaration rectificative |

Use this control loop each time:

- Pre-invoice checks: validate VAT status in VIES, confirm seller and client identification details, and confirm you are not dealing with a private-individual or employee fact pattern.

- Invoice issue: apply reverse-charge wording where eligible and complete mandatory invoice fields before sending.

- Records retention: retain customer and supplier invoice records for 10 years from the close of the financial year.

- Correction protocol: if an error is flagged, correct it formally, because VAT invoiced in error can remain due by the invoice issuer until regularized.

If client status is unclear, facts are mixed between B2B and B2C, or multiple legal entities appear across contract, billing, and payment, escalate to your local tax administration before issuing the invoice.

This pairs well with our guide on A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

If you want a cleaner workflow for preparing cross-border invoices, start with Gruv's free invoice generator.

Frequently Asked Questions

Do I charge French VAT to a French company?

Applies to non-resident B2B. Do not decide from location alone. First confirm the buyer is a VAT-registered business, then use the invoice treatment your accountant or approved template assigns to that fact pattern. If that classification is still unclear, hold the invoice and confirm before sending.

How do I quickly check whether the buyer looks VAT-registered?

Applies to non-resident B2B. A French VAT number should follow FR + 2 check digits + 9-digit SIREN. Match that ID to the same legal entity named in your contract and invoice, and keep dated proof in your file. Treat an entity mismatch as a stop signal, not a formatting issue. | Scenario | Use reverse-charge | Expected invoice treatment | |---|---|---| | Non-resident seller, French business buyer, buyer VAT ID confirmed, and your advisor or template confirms reverse-charge for this service | Only if confirmed | Use your approved reverse-charge template, record the buyer VAT ID, and keep proof of business status | | French private individual or household buyer | Do not assume | Treat this as a separate VAT lane and confirm the correct treatment before invoicing | | French business buyer with no VAT number provided | Do not assume | Do not assume B2B reverse charge; confirm whether registration or another treatment is required | | France-based micro-entrepreneur invoicing under domestic rules | Out of scope | Use domestic France regime rules and format, not this non-resident B2B lane |

What if my client is an individual or a business without a VAT number?

Does not apply to B2B with a confirmed buyer VAT ID. Treat this as a different VAT lane, not a minor admin gap. Foreign companies are listed as needing French VAT registration in cases including sales to private individuals and to businesses without a VAT number in France. Pause and classify correctly before you issue the invoice.

What should be on my invoice if reverse-charge treatment is confirmed for my case?

Applies to non-resident B2B with confirmed reverse-charge treatment. Use wording from your approved accountant or tax-adviser template, not copied language from another seller. Keep buyer details exact, include the French VAT ID you validated, and make the service description specific to the contract, period, milestone, or acceptance point. That gives accounts payable and your compliance file the same clear record.

What VAT rate should I use for services in France?

Applies only if French VAT is actually due. Do not choose a rate until you confirm French VAT must be charged for this supply. Guide figures commonly listed are 20%, 10%, 5.5%, 2.1%, and 0%, but verify the current rate before you use one on a final invoice.

Do French VAT thresholds answer this for me?

Different rules for resident businesses and registration-required cases. Not by themselves. Guide figures such as EUR 85,800 (goods) and EUR 34,400 (services) should be verified before use. Start with classification first: who the customer is and which VAT treatment applies to your supply.

I am based in France or I use the micro-entrepreneur regime. Does this FAQ apply?

Different rules for France-based micro-entrepreneur. Usually no. This section is for non-resident cross-border invoicing, so France-based activity should follow domestic regime rules. Start here: A Guide to France's Micro-Entrepreneur Regime for Freelancers.

What happens if I get the VAT treatment wrong or file late?

Applies whenever French VAT is due or French reporting is triggered. The bigger risk is tax exposure. Reported late filing or payment penalties can reach 40% to 80% of VAT due, plus monthly interest. Fix classification before sending the invoice, not after.

When should I stop and ask a tax professional before issuing the invoice?

Applies to any unclear case. Pause if the buyer will not provide a VAT number, if contract, billing, and paying entities do not match, if you changed legal entity mid-project, or if bundled services make treatment unclear. Also pause if registration may be required, especially for non-EU companies that may need to confirm fiscal representative requirements. Waiting for confirmation is usually cheaper than reissuing invoices and correcting avoidable VAT errors.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- europa.eu/youreurope/business/taxation/vat/index_en.htmtrusted

- taxation-customs.ec.europa.eu/system/files/2022-12/VAT%20in%20the%20Digita...trusted

- taxation-customs.ec.europa.eu/system/files/2024-01/guidelines-vat-committe...trusted

- entreprendre.service-public.gouv.fr/vosdroits/F37527external

- gruv.ai/blog/a-deep-dive-into-the-tva-value-added-ta...external

- impots.gouv.fr/do-foreign-companies-have-register-vatexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

How Freelancers Can Decide on France’s Micro-Entrepreneur Regime

Low-stress compliance starts with one question: does the Micro-entrepreneur regime match your real setup right now? It is often presented as a simplified option for lower-revenue activity, so use it as a fit test, not a shortcut.