Quick Answer

Yes: the tcja impact on freelancers in 2026 is meaningful, but the biggest risk is filing from outdated assumptions. Public Law 119-21 changed the old sunset baseline, so your return should use current checks for Section 199A, Form 8995 guidance, and SALT treatment. If you work abroad, test FEIE and FTC on the same dataset and choose one documented method instead of mixing rules by habit.

Your Executive Briefing: The Key TCJA Provisions Set to Expire in 2025#

Do not plan around the old assumption that many individual TCJA rules would simply expire after 2025. Public Law 119-21, enacted July 4, 2025, changed that baseline. For your next filing cycle, the job is not predicting one cliff. It is separating what was extended, what was modified, and what still needs filing-year verification.

Quick status table#

| Provision | Prior baseline | Current status | Freelancer impact | What to check now |

|---|---|---|---|---|

| QBI deduction (Section 199A) | Treated as scheduled to expire after 2025 | Later law extended or modified the regime, but published summary text conflicts on 20% vs 23% | Still a major pass-through lever, but the exact benefit can materially change your estimate | Confirm filing-year law, IRS guidance, and Form 8995 or 8995-A instructions before filing |

| SSTB limits | Expected to sunset with QBI under older framing | Still relevant where QBI applies; thresholds and phase-ins are filing-year sensitive | Service professionals can still move between full, partial, or no QBI benefit based on taxable income | Use current-year thresholds; do not reuse 2025 numbers for 2026 |

| Standard deduction | Increased amount expected to revert after 2025 | IRS 2026 withholding guidance says the increased standard deduction was permanently extended | This can keep the standard deduction as your default and reduce the value of itemizing in some cases | Verify your filing-status amount, for example, IRS lists $32,200 for MFJ in 2026 |

| SALT cap | Old rule was $10,000 ($5,000 MFS) | Modified, not simply removed; IRS shows $40,000/$20,000 for 2025, and Congress summary text shows $40,400/$20,200 for 2026 with later reversion language | High-tax-state itemizers may see different outcomes year to year | Check the filing-year cap, filing status, and whether itemizing beats the standard deduction |

| Business entertainment vs meals | Entertainment disallowance already in place | Entertainment is generally nondeductible; meals remain under separate rules, including a 50% limit in current IRS guidance | Client entertainment is still generally not deductible just because business was discussed | Separate entertainment from meals and apply current substantiation and deduction rules |

The practical takeaway is that this is now less about a single sunset cliff and more about filing-year accuracy. Use current IRS forms and annual updates for the return year you are filing, and treat older planning numbers as placeholders until you verify them. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Your 2-Year Windfall Strategy: Maximizing Advantage Before the Sunset#

For freelancers, tax-year boundaries matter more than headlines. If a move depends on current rules, use your 2025 return, filed in early 2026, as the main checkpoint. For tax years beginning January 1, 2026, plan conservatively as if there may be no major transition grace period.

The order matters. First settle structure, then timing, then retirement funding. That keeps you from optimizing one piece around assumptions that change once the bigger decision is made.

Entity check#

Start with structure before you optimize timing or retirement funding. This is a fit-and-execution decision with your preparer, not a label upgrade.

| Structure | Admin burden | Payroll complexity | QBI interaction | Usually worth modeling when |

|---|---|---|---|---|

| Sole proprietorship or LLC taxed as sole proprietor | Often lower | Often limited at owner level | Potentially relevant to pass-through deduction analysis; filing-year rules drive outcomes | You want simpler operations and do not want ongoing payroll overhead |

| S-corp election | Often higher | Often includes ongoing payroll process and compliance workload | Potentially changes how income is characterized for pass-through deduction analysis; filing-year rules drive outcomes | Your projected savings may justify added compliance, so a side-by-side model is worth it |

Model an S-corp only if you can handle the compliance cleanly all year. A common failure mode is chasing projected savings while underestimating the payroll, bookkeeping, and documentation load. If payroll would be improvised or your books are already lagging, the paper benefit can look better than the real-world result.

Timing check#

Once structure is settled, optimize timing only within real business activity and actual contract terms. The goal is compliant timing, not paper-only reshuffling.

Focus here when you have variable billing timing, planned business purchases, or contracts with clear invoicing windows. The common failure mode is simple: your records do not match what actually happened. If you cannot trace the sequence from contract to cash, do not treat it as a timing strategy.

Use these guardrails:

- Align contract terms, work completion, invoicing, and payment timing.

- Only book expenses you can clearly support with business records.

- Keep one evidence set per move: contract, invoice, payment proof, receipt, and a short business-purpose note.

- Use conservative judgment, because tax rules can be revised in response to taxpayer behavior.

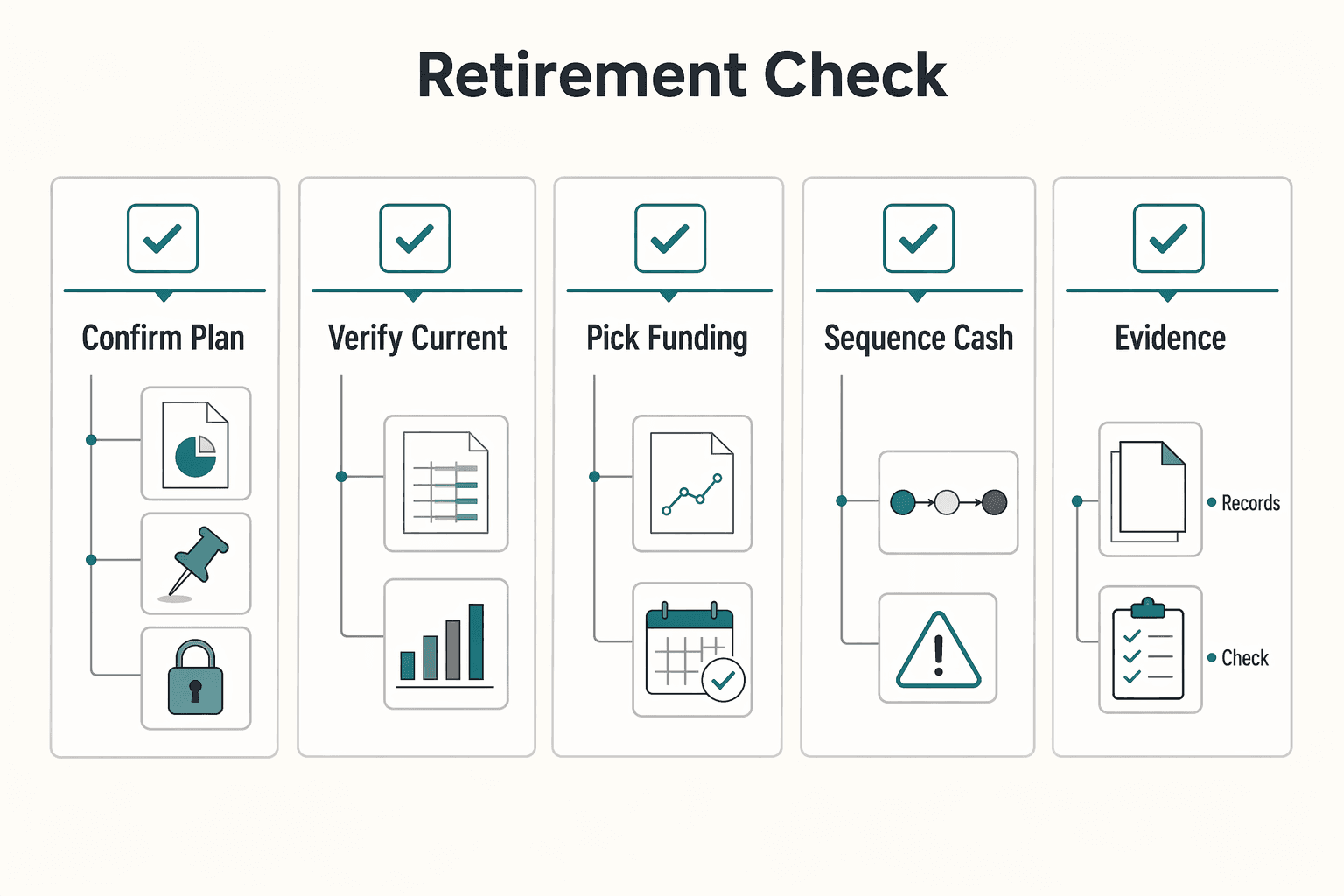

Retirement check#

Retirement funding usually works best as an execution step, not a year-end scramble. If you wait until filing season pressure hits, timing, setup, and cash-flow constraints can narrow your options.

This matters most when you have consistent positive cash flow and a plan to fund contributions without disrupting tax payments. A common miss is waiting too long and then running into setup, cash-flow, or deadline constraints. A good plan is one you can fund on schedule without cannibalizing your tax payments.

Mini checklist:

- Confirm plan eligibility with your preparer and provider.

- Verify current contribution limits and timing rules before acting.

- Pick a funding rhythm now, periodic or lump-sum, and calendar it.

- Sequence cash flow deliberately: estimated taxes, retirement funding, then owner draws.

- Keep plan documents and contribution records in your tax folder.

If you do one thing this quarter, run one integrated model that covers entity setup, projected 2025 taxable outcome, and retirement funding capacity. Build it with uncertainty in mind, since even rules described as permanent can change when Congress revisits them. For a step-by-step walkthrough, see A Deep Dive into the UAE's Corporate Tax for Freelancers and LLCs.

The Global Professional's Edge: Coordinating QBI with FEIE and FTC#

If you live and work abroad, do not default to FEIE or FTC out of habit. The better path depends on your qualifying facts, whether your foreign taxes are actually creditable, and how your income is sourced, including any treaty position.

For most globally mobile freelancers, run both methods on the same facts before filing. Keep Section 199A in that model, because your taxable-income profile can shift depending on which method you use. The wrong default can change both your tax result and your documentation burden.

Choose by tax profile, not preference#

Model FEIE when you clearly qualify, especially if foreign income tax is low or zero. The FEIE cap is $132,900 per qualifying person for 2026 and $130,000 for 2025. If you claim FEIE, attach Form 2555 and complete it carefully, including visa details and qualifying-period travel dates.

Treat FEIE as a multi-year decision, not just a one-year shortcut. Once elected, it generally continues for later years unless revoked.

Model FTC when you pay meaningful foreign income tax and your income is foreign source. FTC is designed to reduce double taxation, but it only offsets U.S. tax on foreign source income, not U.S. source income. In practice, this is where sourcing and treaty analysis start to matter.

Decision table#

| Method | What it does | Main tradeoff | Best-fit scenario | What to verify |

|---|---|---|---|---|

| FEIE-focused | Excludes qualifying foreign earned income from U.S. taxation, then applies the required worksheet method for nonexcluded income. | You cannot claim FTC or a deduction for foreign taxes on excluded income; election generally continues unless revoked. | You qualify for FEIE and your foreign income tax is light. | Form 2555 eligibility and data quality, travel and visa support, housing facts if used, and the confirmed current-year exclusion amount |

| FTC-focused | Claims a credit for qualifying foreign income taxes against U.S. tax on foreign source income. | More sourcing and limitation complexity, especially when treaty re-sourcing is involved. | You pay substantial foreign income tax and expect taxes to meet FTC rules. | Form 1116 category, qualifying tax type tests, source characterization, treaty effects, and confirmed current-year limitation rules |

| Foreign tax deduction (instead of credit) | Deducts qualifying foreign income taxes from taxable income, not dollar-for-dollar tax liability reduction. | Different relief mechanics than FTC; still requires year-specific modeling. | A year where deduction computes better for your facts. | Deductibility of taxes, side-by-side result versus FTC, and consistency across qualified foreign taxes for that tax year |

If a treaty position is part of your plan, verify the exact treaty article, sourcing result, and disclosure requirements before filing. The cleanest filings come from one evidence pack built around the method you actually choose.

Compliance guardrails that reduce filing risk#

| Area | What to retain |

|---|---|

| Foreign tax records | Documentation of assessment, payment, and who had legal liability for the tax |

| Income characterization | Client-level summary of income type and sourcing logic, including treaty effects if any |

| Carryover tracking | If you use FTC, retain Schedule B (Form 1116) support year to year |

| Preparer handoff notes | Residency test used, Form 2555 qualifying dates if applicable, attached forms, and whether Form 8833 is required |

Treaty-based FTC positions need extra care. Certain treaty re-sourced income can require separate FTC limitation handling and separate Form 1116 treatment. If required treaty disclosure is missed, a $1,000 penalty may apply.

The mechanical difference matters. A credit reduces tax liability, while a deduction reduces taxable income.

For more detail, see A Guide to the Qualified Business Income (QBI) Deduction for Freelancers. Before you lock in FEIE versus FTC, test your own assumptions in the FEIE calculator.

The 2026 Resilience Plan: Bulletproofing Your Business for the Post-TCJA World#

Turn your tax model into an operating plan now so 2026 is managed, not reactive. In practice, that means three projections, one clear entity decision, tighter records, and escalation triggers set before filing deadlines force rushed choices.

Run a three-case projection workflow#

Use one file, and hold your income assumptions constant across all cases so the differences are easy to explain.

| Projection | What to include | What to verify before relying on it |

|---|---|---|

| Baseline projection | Current income mix, current structure, and current payment or compensation pattern | Use the current-year rates, thresholds, and IRS inflation adjustments that apply to the return you are modeling. |

| Likely-change projection | Keep operations realistic, but remove temporary benefits you do not expect to continue into 2026 | Confirm which rule changes actually apply to your return instead of assuming every headline applies |

| Stress-case projection | Revenue softness, slower collections, and a worse tax outcome than expected | Test whether cash reserves and payment planning still work if your refund shrinks or you owe more |

Even if the seven bracket rates are still shown as 10%, 12%, 22%, 24%, 32%, 35%, and 37%, your outcome can still move. Re-run this workflow when updated IRS figures are released and again when your income pattern changes. If you cannot explain why the three cases differ, you do not have a planning file you can trust yet.

Re-test your entity structure with a decision checklist#

Keep your current setup only if it still works operationally and financially under your 2026 projections. If any cross-border point is unclear, pause major structure changes until both sides of the filing picture are reviewed.

| Decision point | Keep current structure if... | Revisit structure if... |

|---|---|---|

| Admin load | Ongoing filings and bookkeeping are consistent and manageable | Compliance work causes recurring delays or errors |

| Payroll obligations | Payroll is timely, documented, and controlled | Payroll is inconsistent, late, or hard to support |

| Net tax effect | Projected benefit still clearly exceeds overhead | Projected benefit narrows or disappears |

| Cross-border complexity | Structure fits your residency, sourcing, and filing reality | Structure creates avoidable foreign reporting or coordination friction |

Build a compliance-first records system#

Good records are not a side task here. They are what let you defend the return without reconstructing the year after the fact.

| Record area | What to maintain |

|---|---|

| Expenses | Maintain monthly expense categories with receipt copies and payment proof |

| High-risk expenses | Add a short business-purpose note to unusual or high-risk expenses |

| Home office and travel | Keep a home-office file and a travel log with dates and business purpose, where applicable |

| Client income summaries | Keep client-level income summaries where sourcing or cross-border treatment needs support |

| Year-end handoff | Prepare a year-end handoff package for your preparer: financial summaries, account summaries, payroll reports if applicable, prior return, and estimated-payment history |

Convert projected tax change into operating actions#

If your likely-change case comes in higher than baseline, translate the gap into operating moves immediately.

- Review rates for new work and renewals so margin pressure is not discovered late.

- Set or increase a tax reserve target tied to your projection gap.

- Review estimated-payment timing during the year, and check withholding settings where relevant.

Escalate to a tax pro when any of these apply:

- Your baseline and likely-change outcomes diverge and you cannot explain why.

- You are considering an entity change.

- The same income is affected by both U.S. and foreign filing positions.

- Your support for home office, travel, payroll, or foreign tax items is incomplete.

- Your cash plan depends on a refund that may not materialize.

That is resilience in practice: verified inputs, one clear structure decision, clean records, and cash planning that can absorb a rougher year. Related: How to Choose the Right Business Structure for Your Freelance Business.

From Anxiety to Action: Securing Your Financial Future#

Treat this as a filing checklist, not a guessing exercise. Confirm what you can verify now and file from documented facts.

Start with the inputs this article cannot finalize for you. Before filing, verify the current-year rules that affect your return. If those are not confirmed, do not carry forward last year's assumptions.

Decision checkpoints#

First, tie your FEIE or FTC position to your records. For FEIE, confirm you have foreign earned income, a foreign tax home, and a qualifying status test. If you use the physical presence test, the gate is 330 full days in a 12 consecutive month period. Each counted day must be a full 24 hours (midnight to midnight). This test is based on time abroad, and if you miss that threshold, the test fails.

| Checkpoint | Requirement or note |

|---|---|

| FEIE qualification | Confirm you have foreign earned income, a foreign tax home, and a qualifying status test. |

| Physical presence test | The gate is 330 full days in a 12 consecutive month period. |

| Counted day | Each counted day must be a full 24 hours (midnight to midnight). |

| Form 1116 | Form 1116 is category-based, and multi-country taxes require separate country lines or columns. |

| Foreign housing exclusion | If you also claim the foreign housing exclusion, compute it first because it reduces income available for FEIE. |

Second, prepare form-level support before you file. Excluded foreign earned income is still reported on your U.S. return. If you use FTC mechanics, Form 1116 is category-based, and multi-country taxes require separate country lines or columns. If you also claim the foreign housing exclusion, compute it first because it reduces income available for FEIE.

Confirm, Decide, Document, Review#

- Confirm: the current-year filing rules relevant to your return.

- Decide: your FEIE versus FTC filing position based on qualification tests and your actual records.

- Document: day counts, foreign-earned income support, and foreign-tax records by country and category.

- Review: return consistency across day counts, exclusions, and Form 1116 category and country breakdowns.

| Choice | Compliance risk | Planning flexibility | Workload |

|---|---|---|---|

| Act now | Can be lower, because errors are easier to catch before filing | Higher, because you can still adjust positions | Higher upfront |

| Wait | Can be higher, because issues surface late | Lower, because fewer options remain | Lower now, heavier later |

Talk to a pro if your cross-border facts point to more than one plausible treatment, your 330-day count is close, or your Form 1116 category or country allocation is unclear.

For a treaty-specific example, see A Deep Dive into the US-Israel Tax Treaty for Tech Freelancers. If you want a calmer filing workflow, track your residency evidence and deadlines in the tax residency tracker.

Frequently Asked Questions

When does the 20% QBI deduction expire?

Treat the post-2025 status as something to verify, not something to guess. As of 2026, IRS materials still include language tied to tax years ending on or before December 31, 2025, while Form 8995 instructions also tell you to check for later legislative changes, and Public Law 119-21 was signed on July 4, 2025. The practical move is to confirm current Section 199A and Form 8995 guidance before you assume the deduction is gone, extended, or changed for your return.

Do consultants and other service professionals get the QBI deduction?

Yes, but your taxable-income range is the key gate if your work is an SSTB, such as consulting. For 2025, Form 8995 instructions show $394,600 for MFJ and $197,300 for all other returns as key thresholds, with SSTB phase-in bands running to $494,600 for MFJ and $247,300 for all other returns. Before you make timing moves, verify both your business classification and the current-year thresholds.

Is it better to be an S corp or sole proprietor under the tcja impact on freelancers?

Neither is automatically better for you. If you elect S corp status, you must pay reasonable compensation for shareholder-employee services, and the IRS can reclassify non-wage distributions when compensation is set too low. Weigh any potential benefit against added payroll and admin burden, then review the election with a pro before filing.

How does the tcja impact on freelancers who live abroad?

Your main decision is usually FEIE versus FTC, not both on the same excluded income. FEIE can reduce regular income tax but does not reduce self-employment tax, and the physical presence route requires 330 full days in 12 consecutive months; the FEIE maximum is $132,900 per qualifying person for 2026. The practical move is to run both methods when the same income is taxed abroad and in the U.S., then escalate if Section 199A or entity choices are also in play. | Option | Best fit | Main tradeoff | |---|---|---| | FEIE | You qualify abroad and want exclusion treatment up to the annual cap | It does not reduce self-employment tax, and you cannot claim FTC on the same excluded income | | FTC | You paid foreign tax on income also taxed by the U.S. | Relief depends on paid foreign tax and credit mechanics, so modeling is less straightforward | | S corp election | You can support reasonable compensation with real payroll records | More filings and payroll compliance, plus reclassification risk if compensation is set too low | | Stay sole proprietor | You want operational simplicity and no payroll setup | Simpler operations, but you may miss scenarios where S corp treatment helps |

Will my taxes go up after the TCJA rules change?

Plan for a higher bill as a realistic case, not a certainty. Your taxes can rise if Section 199A is unavailable to you or if current individual rules are less favorable than your prior assumptions. The right move is to rerun your 2026 projection with verified IRS inputs instead of reusing last year’s model.

What happens to the SALT deduction cap in 2026?

Do not file based on old SALT headlines. Confirm current SALT cap treatment in current IRS instructions and applicable law updates before you file. If you pay meaningful state or local tax, have your preparer compare the standard deduction against itemizing both ways.

When should you stop DIY-ing this and call a pro?

Escalate when your filing outcome changes based on FEIE versus FTC, SSTB threshold position, or an S corp case that depends on tight payroll assumptions. Also call a pro if your records cannot clearly support day counts abroad, payroll reasonableness, or the inputs feeding Form 8995. That is the point where this shifts from tax planning to filing-risk management.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Choose the Right Business Structure for Your Freelance Business

Most freelancers end up in a business structure by default rather than by design, but that accidental choice shapes taxes, personal liability, and payment operations in ways that compound over time. This guide walks independent professionals through four entity types — Sole Proprietorship, Single-Member LLC, S-Corp election, and Corporation — covering the tax treatment, liability exposure, and operational overhead of each. Rather than prescribing a single best answer, it provides a trigger-based framework: start with the structure that fits today, then upgrade when specific signals — indemnification clauses, enterprise KYB requirements, a first hire, or material net profit — make the switch worthwhile. The result is a deliberate, revisable foundation that keeps records clean, reduces onboarding friction, and avoids the expensive mismatches that come from letting structure lag behind business growth.

A Guide to the Qualified Business Income (QBI) Deduction for Freelancers

**You can classify your Section 199A path in one focused session, then move with confidence instead of guessing.** Treat this as an operating manual for the QBI deduction if you freelance. Classify first, optimize second. That order matters even more when you work across borders, where documentation and residency rules can vary by jurisdiction.