Quick Answer

Yes. If you are tax resident in Country A and control a company in Country B, treat the associated enterprises tax treaty issue as active and test it before filing. Use Article 9.1 participation in management, control, or capital as your trigger, then build one file with a signed intercompany agreement, a comparability memo, invoice and work evidence, and a books-to-return tie-out. Escalate quickly if an adjustment notice appears or your records stop reconciling.

Does This Corporate Rule Even Apply to My 'Business-of-One'?#

Usually, yes. If you are tax resident in one country and directly or indirectly control an enterprise in another, assume associated-enterprises exposure is in scope until you test it.

In Article 9.1 terms, the test is participation in management, control, or capital, including common participation by the same persons. For a business-of-one, the practical signal is simple: if you can direct decisions and set terms between yourself and the company, this is likely your issue.

Does this apply to me?#

Use this quick check:

- You are tax resident in Country A.

- Your company is in Country B.

- You control how contracts or pricing are set between you and the company.

If all three are true, the treaty issue is live and needs review. Do not assume treaty wording is your only exposure. Domestic transfer-pricing rules can still apply. For example, U.S. section 482 applies to controlled businesses whether or not incorporated, and UK transfer-pricing rules do not require a treaty.

What transactions are in scope?#

Do not limit this to salary. Start with all commercial or financial relations between you and the company.

The pricing standard is the arm's length principle. Terms should match what independent parties would have agreed. That is where authorities focus, because non-arm's-length terms can shift profit between related parties.

What should be documented first?#

Before you try to optimize anything, build a basic evidence pack. Confirm residence and control facts, then map each related-party transaction and how its price was set. Keep proof tying each transaction to real activity.

If that chain is weak, your position is weak. From there, build a documentation file that explains the arrangement, supports the pricing, and connects payment to work performed.

For a step-by-step walkthrough, see A Deep Dive into the 'Royalties' Article of the US-UK Tax Treaty for Authors.

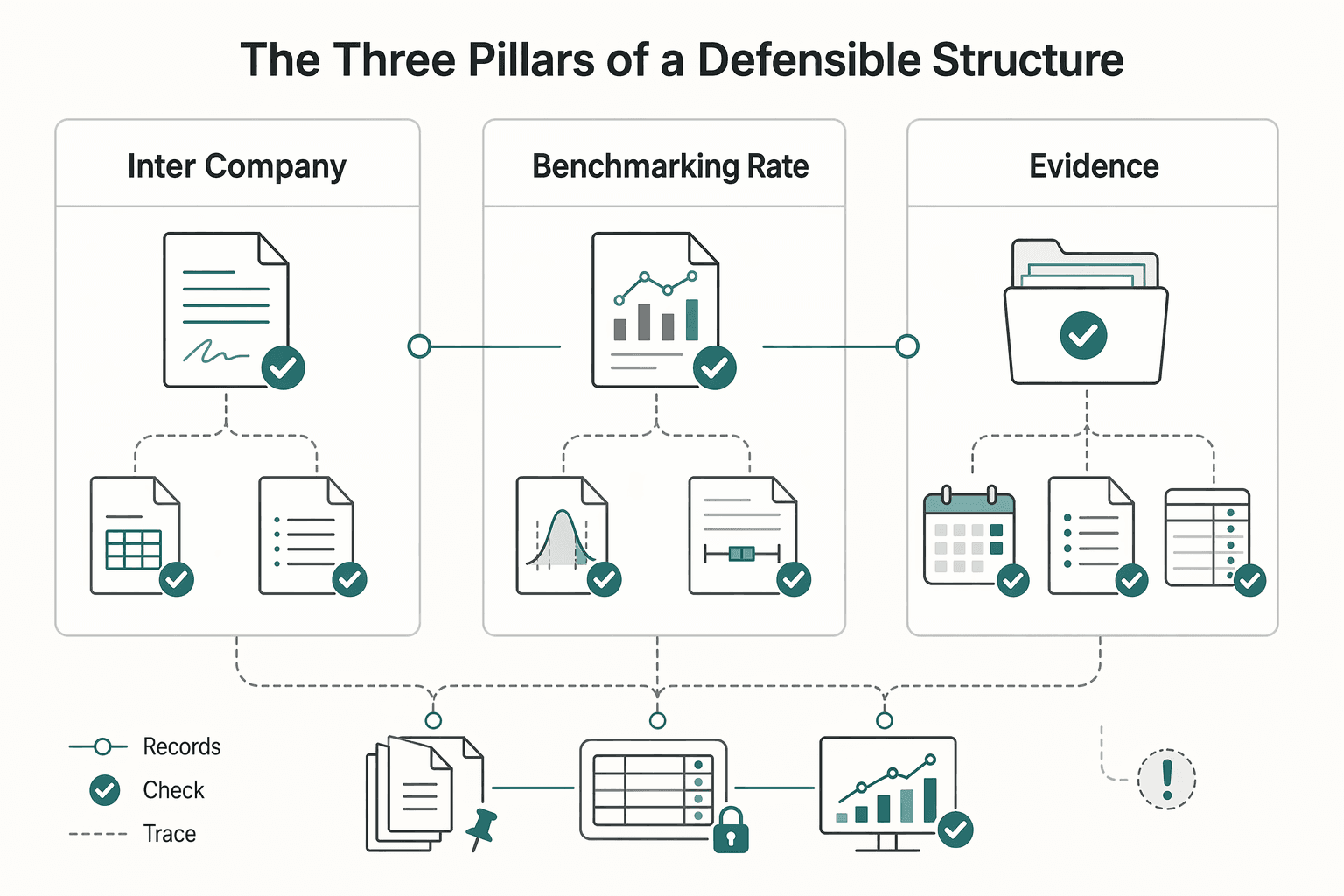

The Three Pillars of a Defensible Structure#

Your goal is one defensibility file that holds three things together: a written agreement, a pricing rationale, and records showing the work actually happened. If one pillar is weak, the others usually weaken with it. A practical audit-ready standard is a consistent line from your documents to your books to your reported income.

| Pillar | What good looks like | Common weak spot | What to store in your file |

|---|---|---|---|

| Inter-company service agreement | Clear services, pricing method, responsibilities, and payment terms | Generic language that does not match real work or actual payment pattern | Signed agreement, amendments, approval emails, version history |

| Benchmarking and rate support | Rate selected from comparable market evidence, with a short written rationale | Screenshots collected without a comparability explanation | Source screenshots/data, peer examples, comparability memo |

| Record-keeping and audit trail | Invoices, logs, deliverables, and payment records that tie back to agreement and pricing rationale | No clear link between work performed, amounts billed, and what hit the books | Invoices, activity logs, deliverables, payment proof, ledger tie-out |

Pillar one is your minimum viable agreement#

Keep this practical. You do not need a long contract, but you do need terms that clearly match how the work and payments actually happen. At minimum, include:

| Agreement element | What to include |

|---|---|

| Scope of services | what you actually do, not just a vague "consulting" label. |

| Pricing method | hourly, fixed monthly, per project, or another method you can apply consistently. |

| Responsibilities | who performs, approves, and manages the work. |

| Payment mechanics | invoice timing, due dates, currency, reimbursement handling, and payment documentation. |

A useful self-check is whether you can draft your invoice format directly from the agreement without guessing.

Pillar two is benchmarking the rate and explaining the fit#

Evidence without explanation is easy to challenge. You need a short memo that explains why your chosen rate fits your facts. Use this comparability frame as a practical consistency check, not a treaty-mandated checklist:

| Comparability factor | What to check |

|---|---|

| Role | same seniority and function. |

| Market | which geography drives pricing in your case. |

| Scope | similar breadth of work. |

| Delivery model | freelance, agency, employee, or retainer context. |

Store the evidence and your reasoning together. If pricing changes, add a dated update note instead of letting the logic drift.

Pillar three is keeping an audit trail that reconciles#

This is where otherwise reasonable files often break down. Your records should let someone trace each payment from agreement to return. IRS examination checkpoints explicitly include reconciling books and records to reported income and testing gross receipts, so your file should support that flow.

| Step | What the file should show |

|---|---|

| Agreement | current terms and pricing method. |

| Pricing memo | why the rate or fee is reasonable. |

| Invoices | service period and reference to governing terms. |

| Work evidence | logs, deliverables, briefs, or other dated proof of work. |

| Payment proof | bank or accounting record showing payment. |

| Books/return tie-out | summary that matches ledger amounts to reported income. |

Use that six-step chain each year. Stress test the file by picking one invoice and tracing it through all six steps in minutes, not hours.

When to escalate before problems compound#

Escalate early if the facts stop lining up. Common triggers include:

- Compensation logic changes without documentation.

- Agreement terms, invoice labels, and bookkeeping labels do not match.

- Core records are missing or scattered across systems.

- You cannot reconcile booked amounts with what you reported.

If any of these are present, the next question is not how to paper over the gap. It is what the exposure looks like and what recourse you still have.

If your cross-border setup also turns on where you work, Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025) covers the operating side.

Before you lock your defensibility file, run a draft through the freelance contract generator so your scope, responsibilities, and payment terms are documented in one place.

Understanding the Stakes: Risks and Recourse#

Once your file has gaps, the risk is straightforward. A tax authority can adjust profits, and you can end up managing double-taxation risk across two jurisdictions while facing heavier documentation pressure.

What non-compliance usually looks like in practice#

If the conditions between you and your company are not arm's length, a tax authority may adjust taxable profits by effectively rewriting the accounts for tax purposes. Consistent invoicing alone does not establish that pricing is arm's length.

That can leave the same underlying income taxed in different hands across jurisdictions. In practice, the burden can be both tax and process: additional tax exposure, possible domestic transfer-pricing penalties, more audit scrutiny, and broader document requests.

As soon as you receive an adjustment notice or proposed adjustment, log these five items in one place:

- Issuing authority

- Tax year(s)

- Entities involved

- Transaction type

- Response or notification deadline

That date tracking matters because some treaties tie notification periods to MAP access.

Your recourse if an adjustment creates double taxation#

Treaty relief is a primary path, but it is never automatic. It depends on the treaty text and the procedure available. If Article 9(2)-style language is present, a corresponding adjustment may be available. If not, MAP is often the main route.

Use this sequence immediately:

- Document the adjustment. Keep the notice, computation, tax years, legal basis cited, and proposed income increase in one memo.

- Align advisors across both jurisdictions. Work from one agreed fact pattern, one transaction map, and one pricing narrative.

- Prepare a MAP/corresponding-adjustment case file. Include your intercompany agreement, pricing memo, invoices, work evidence, payment proof, ledger tie-out, returns, and a dated timeline.

MAP is a bilateral competent-authority process that seeks treaty-consistent relief. Case quality matters early. MAP access can be denied for defective requests. If a U.S. exam is involved, transfer-pricing documentation may be requested within 30 days. MAP is a recourse path, not a guarantee of full relief or a fixed timeline.

When to involve a specialist#

Bring in a cross-border specialist promptly if any of these apply:

- You received a cross-border adjustment notice or proposed adjustment.

- The same income may be taxed in both jurisdictions.

- You cannot tell whether your treaty position is a clear Article 9(2) path, a MAP path, or both.

AE and PE are different problems, so defend them differently#

Do not blend these analyses. Associated-enterprise pricing and permanent establishment are separate tests. AE focuses on arm's-length pricing. PE focuses on taxable presence, including fixed-place and dependent-agent tests.

| Issue | Core question | What triggers scrutiny | What evidence helps your defense | What to do now |

|---|---|---|---|---|

| Associated enterprises pricing | Was pricing between related entities arm's length? | Conditions that appear non-arm's-length, or a cross-border adjustment to related-party pricing | Signed service agreement, pricing memo, invoices, dated work logs, payment proof, ledger tie-out, return reconciliation | Trace one invoice end to end and confirm your current pricing method still matches reality |

| PE through a fixed place | Is there a fixed place of business through which the enterprise's business is carried on? | Facts suggesting business is carried on through a fixed place | Occupancy/control facts, who uses the space, what business activity occurs there, records consistent with actual activity | Review your real operating facts as an examiner would, not just contract wording |

| PE through dependent-agent activity | Do you have authority to conclude contracts in the enterprise's name? | Facts indicating authority to conclude contracts in the enterprise's name | Delegations of authority, approval-chain records, board/director approvals, executed contracts showing approval flow | Map who negotiates, approves, and signs, then align records to that map |

A clean pricing file helps on AE, but it does not resolve PE if your facts show fixed-place activity or contract-concluding authority.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Quick Reference: Your Key Questions Answered#

Can my foreign company and I be treated as associated enterprises?#

Possibly. If you are tax resident in one country, your company is in another, and you control how terms are set between you and the company, treat the issue as live until you verify the treaty wording and domestic-law position for the tax year.

What to do next: Pull the relevant treaty, note the article wording, list the tax years, and map every payment flow between you and the company.

What does the arm's length principle mean in practice?#

It means the terms between you and your company should match what independent parties would have agreed. In practice, that means you need a clear explanation of the services, the pricing approach, and records showing the work actually happened.

What to do next: Write a one-page memo covering the services, pricing approach, and supporting records.

What is the difference between associated enterprises and permanent establishment risk?#

AE is a pricing question. PE is a taxable-presence question. Keep them separate and confirm each position against the specific treaty wording and domestic rules.

What to do next: Run two separate reviews and verify each position against the treaty wording before you file or respond.

What are the biggest risks if my pricing is not supportable?#

The main risks are an income adjustment, possible double taxation across two jurisdictions, and a more demanding audit process. Cross-border information requests can also escalate, and foreign-initiated requests can include summons procedures, proceedings to quash, and enforcement under IRM 4.60.1.2.2.4.

What to do next: As soon as an issue appears, log the issuing authority, tax years, entities, legal basis cited, and response deadline in one case memo.

How do I prove my pricing and treaty position?#

Build one evidence pack that ties the transaction from agreement to return: agreements, invoices, dated work evidence, payment proof, ledger tie-out, and return reconciliation. If you are taking a U.S. treaty-based position, review IRS Publication 901 (09/2024), including Application of Treaties, Personal Services Income, and Disclosure of a treaty-based position that reduces your tax.

What to do next: Test one invoice against your agreement, bank record, ledger entry, and return treatment from start to finish.

Do I need a full transfer pricing study for a one-person business?#

There is no bright-line rule stated here for when a full study is required. Start with a written file that explains your pricing and evidence, and get targeted advisor input when your facts are complex or unclear.

What to do next: Decide whether your file would make sense to an examiner seeing the transaction for the first time.

Is an intercompany service agreement really necessary?#

There is no universal rule stated here, but having a written agreement usually makes your position easier to explain if it matches your real invoicing and payment pattern.

What to do next: Check that the agreement date, parties, services, pricing terms, and signatures align with what happened in your books.

When should I talk to a cross-border tax advisor?#

Talk to one early if your treaty position is unclear, if you have received a cross-border adjustment notice, or if cross-border information requests are in play. IRS IRM 4.60.1 includes both United States-Initiated Specific Requests for Information and Foreign-Initiated Specific Requests for Information, and subsection 4.60.1.2.2.4 includes summons procedures, proceedings to quash, and enforcement.

What to do next: Send the advisor your notice, treaty article, tax years, transaction map, and core evidence pack before the first response deadline.

If foreign tax credits are part of the same fact pattern, we covered the mechanics in detail in A Deep Dive into the Foreign Tax Credit (Form 1116).

From Compliance Anxiety to CEO Confidence#

The practical way to use Article 9 is as a pricing-fairness rule for your own operation. Define your role, set arm's-length compensation logic, keep proof of delivery, and review it on a recurring schedule. Many problems come not from the structure alone, but from a mismatch between what you say happened and what your records show.

If your agreement says ongoing strategic services but invoices are vague, payment timing is inconsistent, and dated work evidence is thin, you leave key facts open to interpretation.

| Anxious / Reactive | CEO / Controlled |

|---|---|

| Behavior | Waits for a notice, then reconstructs facts |

| Documentation quality | Generic agreement, weak invoice detail, scattered files |

| Likely process impact | Can lead to more follow-up requests and credibility pressure |

Your safe-default workflow#

The safest default is simple: document the arrangement before you file, keep evidence as you work, and test whether the whole file reconciles.

- Use an intercompany agreement that matches reality: parties, services, pricing method, invoice timing, and signatures.

- Write a one-page pricing memo with your comparability logic, showing how your controlled terms align with independent-party conditions.

- Keep delivery evidence as you work: invoices, timesheets or time logs, dated outputs, and payment proof.

- Test one invoice end to end against the agreement, bank record, ledger entry, and return treatment.

- Review and refresh the file annually. For in-scope UK transfer-pricing records, HMRC guidance says the Master File and Local File should be reviewed and updated annually. IRS FAQ says U.S. documentation generally should exist when the return is filed and be provided within 30 days if requested.

A strong file does not guarantee zero penalties or an easy examination, but it gives you a defensible starting point.

Escalate early to a qualified advisor if you receive an adjustment notice, face potential double taxation, cannot confirm whether your treaty includes a corresponding adjustment path, or have material U.S. Section 482 exposure. That is also the right point to discuss MAP and, for complex U.S. transfer-pricing matters, whether the APA program is practical. For deeper pricing mechanics, see the transfer pricing guide.

For another treaty-article walkthrough, you might also find useful A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

If your setup spans multiple countries or related entities, use contact to pressure-test your compliance workflow before your next filing cycle. ---

Frequently Asked Questions

Does this apply to me?

Use this quick check: You are tax resident in Country A. Your company is in Country B. You control how contracts or pricing are set between you and the company. If all three are true, the treaty issue is live and needs review. Do not assume treaty wording is your only exposure. Domestic transfer-pricing rules can still apply. For example, U.S. section 482 applies to controlled businesses whether or not incorporated, and UK transfer-pricing rules do not require a treaty.

What transactions are in scope?

Do not limit this to salary. Start with all commercial or financial relations between you and the company. The pricing standard is the arm's length principle. Terms should match what independent parties would have agreed. That is where authorities focus, because non-arm's-length terms can shift profit between related parties.

What should be documented first?

Before you try to optimize anything, build a basic evidence pack. Confirm residence and control facts, then map each related-party transaction and how its price was set. Keep proof tying each transaction to real activity. If that chain is weak, your position is weak. From there, build a documentation file that explains the arrangement, supports the pricing, and connects payment to work performed. For a step-by-step walkthrough, see A Deep Dive into the 'Royalties' Article of the US-UK Tax Treaty for Authors.

Can my foreign company and I be treated as associated enterprises?

Possibly. If you are tax resident in one country, your company is in another, and you control how terms are set between you and the company, treat the issue as live until you verify the treaty wording and domestic-law position for the tax year. What to do next: Pull the relevant treaty, note the article wording, list the tax years, and map every payment flow between you and the company.

What does the arm's length principle mean in practice?

It means the terms between you and your company should match what independent parties would have agreed. In practice, that means you need a clear explanation of the services, the pricing approach, and records showing the work actually happened. What to do next: Write a one-page memo covering the services, pricing approach, and supporting records.

What is the difference between associated enterprises and permanent establishment risk?

AE is a pricing question. PE is a taxable-presence question. Keep them separate and confirm each position against the specific treaty wording and domestic rules. What to do next: Run two separate reviews and verify each position against the treaty wording before you file or respond.

What are the biggest risks if my pricing is not supportable?

The main risks are an income adjustment, possible double taxation across two jurisdictions, and a more demanding audit process. Cross-border information requests can also escalate, and foreign-initiated requests can include summons procedures, proceedings to quash, and enforcement under IRM 4.60.1.2.2.4. What to do next: As soon as an issue appears, log the issuing authority, tax years, entities, legal basis cited, and response deadline in one case memo.

How do I prove my pricing and treaty position?

Build one evidence pack that ties the transaction from agreement to return: agreements, invoices, dated work evidence, payment proof, ledger tie-out, and return reconciliation. If you are taking a U.S. treaty-based position, review IRS Publication 901 (09/2024), including Application of Treaties, Personal Services Income, and Disclosure of a treaty-based position that reduces your tax. What to do next: Test one invoice against your agreement, bank record, ledger entry, and return treatment from start to finish.

Do I need a full transfer pricing study for a one-person business?

There is no bright-line rule stated here for when a full study is required. Start with a written file that explains your pricing and evidence, and get targeted advisor input when your facts are complex or unclear. What to do next: Decide whether your file would make sense to an examiner seeing the transaction for the first time.

Is an intercompany service agreement really necessary?

There is no universal rule stated here, but having a written agreement usually makes your position easier to explain if it matches your real invoicing and payment pattern. What to do next: Check that the agreement date, parties, services, pricing terms, and signatures align with what happened in your books.

When should I talk to a cross-border tax advisor?

Talk to one early if your treaty position is unclear, if you have received a cross-border adjustment notice, or if cross-border information requests are in play. IRS IRM 4.60.1 includes both United States-Initiated Specific Requests for Information and Foreign-Initiated Specific Requests for Information, and subsection 4.60.1.2.2.4 includes summons procedures, proceedings to quash, and enforcement. What to do next: Send the advisor your notice, treaty article, tax years, transaction map, and core evidence pack before the first response deadline. If foreign tax credits are part of the same fact pattern, we covered the mechanics in detail in A Deep Dive into the Foreign Tax Credit (Form 1116).

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/international-businesses/transfer...trusted

- irs.gov/businesses/international-businesses/transfer...trusted

- law.cornell.edu/uscode/text/26/482trusted

- oecd.org/en/topics/transfer-pricing.htmltrusted

- gov.uk/hmrc-internal-manuals/international-manual/i...external

- gov.uk/hmrc-internal-manuals/international-manual/i...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Transfer Pricing for Small International Businesses with Related Entities

For a business of one operating across related entities, transfer pricing is mostly about execution. Document each related-party charge when it happens, choose the most reliable method you can actually support, and have the file ready before you file your return. If you wait until year-end, the evidence can be harder to rebuild and your method support can be easier to challenge.