Quick Answer

U.S. expats can claim the Additional Child Tax Credit only if they have a qualifying child, the required SSNs, at least $2,500 of earned income on Form 1040/1040-SR, and no Form 2555 attached. If refund access matters, compare FTC and FEIE before filing because using Form 2555 makes ACTC unavailable for that year.

A Global Professional's Playbook for the Additional Child Tax Credit (Form 8812)#

If you file from abroad, one practical question is cash flow. When can part of your child credit come back as a refund instead of only reducing tax on paper?

The Child Tax Credit (CTC) is nonrefundable. It can reduce your U.S. income tax to zero, but not below zero. If your tax is already zero, unused CTC does not automatically turn into a payout.

The Additional Child Tax Credit (ACTC) is the refundable part of the child-credit rules. Refundable means the credit can exceed your tax liability, so it may still produce a refund even when you do not owe income tax.

What "earned income" means in plain English#

For this credit, earned income generally means pay from work: wages, salary, tips, and net earnings from self-employment. It does not mean every dollar reported on your return. Unearned items like interest and dividends do not automatically count as earned income.

| Income item | Counts as earned income? | Article note |

|---|---|---|

| Wages | Generally yes | Pay from work |

| Salary | Generally yes | Pay from work |

| Tips | Generally yes | Pay from work |

| Net earnings from self-employment | Generally yes | Support with self-employment books showing net earnings |

| Interest | Does not automatically count | Unearned item |

| Dividends | Does not automatically count | Unearned item |

A practical check is to tie that assumption to records showing work-based income, such as wage records or self-employment books with net earnings. If you cannot support it as pay from work, do not treat it as earned income for this calculation.

The basic math on Schedule 8812#

At a high level, the formula is:

Potential ACTC refund = [current statutory percentage after verification] x (earned income above [current earned-income trigger after verification]), capped at [current per-child refundable cap after verification].

Treat each bracketed value as a live filing-year input. Before you rely on any calculator or prior-year article, verify current numbers and updates at IRS.gov/Schedule8812.

| Scenario | Earned income input | Formula result | Practical outcome |

|---|---|---|---|

| Below trigger | Less than or equal to [current earned-income trigger after verification] | No excess above trigger | No refundable amount under this formula |

| Above trigger, below cap | [trigger + moderate earned income amount] | [current statutory percentage] x excess earnings | Partial refundable amount, if other eligibility rules are met |

| High enough to hit cap | [earned income amount large enough to exceed cap] | Formula output exceeds [current per-child refundable cap] | Refund limited to the per-child cap |

Schedule 8812 is where this gets computed, so input quality matters more than spreadsheet math. Plan cash flow conservatively. This is a claimed credit, not guaranteed immediate cash, and IRS refund timing rules can delay issuance for returns that properly claim ACTC.

That is the calculation. The next question is whether you can actually use it. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

The Three Eligibility Hurdles for Global Professionals#

Start here before you compare FEIE and FTC. In practice, three things decide whether ACTC is even on the table for you: your child must meet the qualifying-child rules, your documentation must satisfy the SSN requirement, and your return must show eligible earned income.

A qualifying child is not just your child by relationship. For this credit, the child must meet IRS qualifying-child conditions, including age and dependency tests. The child also must meet residency, support, and U.S. status requirements. In practice, you are checking whether the child lived with you for more than half the tax year, is claimed as your dependent, did not provide more than half of their own support, and meets the U.S. status test.

A valid SSN for this credit means an SSN valid for U.S. employment and issued by the return due date, including extensions. An ITIN is an individual taxpayer identification number, but it does not replace the child SSN requirement for this credit. A CRBA documents citizenship at birth, but it is not a birth certificate and it is not a substitute for the required SSN. On a joint return, only one filer must have a valid SSN; the other filer may have an SSN or ITIN.

Earned income here means taxable pay from work or business activity. For the Schedule 8812 ACTC computation, include only earned income reported on Form 1040/1040-SR. If you file Form 2555, you cannot claim ACTC. Use $2,500 as your minimum check, and verify current-year updates at IRS.gov/Schedule8812.

| Hurdle | Pass if you can confirm | Pitfall to avoid | Corrective action |

|---|---|---|---|

| Qualifying child | Age/dependency conditions plus residency, support, and U.S. status tests are met | Assuming "living abroad" is an automatic fail | Recheck each IRS test with your year-specific family records |

| Valid SSN and documents | Child has a valid SSN issued by the filing due date | Using a CRBA or child ITIN as a substitute | Complete SSN issuance first and keep issuance timing records |

| Earned income on the return | At least $2,500 of earned income is reported on Form 1040/1040-SR | Counting income excluded through Form 2555 | Validate return line inputs before estimating any refundable amount |

If you clear all three hurdles, you have established eligibility only. You still need to apply the rest of the return rules before expecting an ACTC refund. Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

The Core Strategic Decision: FEIE vs. FTC#

This is the decision point that changes the outcome. Under current Schedule 8812 Part II-A form text, if you file Form 2555 (FEIE), you cannot claim the refundable Additional Child Tax Credit.

Mechanically, the difference is straightforward. FEIE is claimed on Form 2555 to exclude qualifying foreign earned income and, where eligible, housing exclusion or deduction amounts. FTC is generally claimed on Form 1116 and reduces U.S. income tax dollar for dollar for eligible foreign taxes paid or accrued.

Why this decision changes your refund outcome#

The key distinction is whether your return excludes income or reports it and claims foreign taxes against it.

Excluded income is income removed from U.S. taxation under FEIE. Even though IRS guidance notes that excluded foreign income is still reported on the return, that does not override the Schedule 8812 rule: if Form 2555 is filed, you cannot claim ACTC.

Reported earned income for Schedule 8812 is earned income reported on Form 1040/1040-SR. ACTC eligibility also requires at least $2,500 of earned income. If refund access is part of your goal, the first checkpoint is simple: no Form 2555 attached.

Compare the paths side by side#

| Path | Usually better to model first when... | ACTC consequence | Documentation burden | Common mistake to avoid |

|---|---|---|---|---|

| FEIE on Form 2555 | You want to exclude qualifying foreign earned income and, if eligible, housing amounts | Filing Form 2555 blocks ACTC | FEIE qualification support, foreign earned income records, housing records if used | Assuming excluded income can still support ACTC because it appears on the return |

| FTC on Form 1116 | You want to claim eligible foreign taxes as a credit instead of excluding income | Does not trigger the Form 2555 ACTC bar, but other ACTC tests still apply | Foreign tax payment or accrual records, withholding or tax statements, Form 1116 support | Claiming FTC on taxes tied to excluded income |

| Mixed FEIE/FTC profile | Your facts require careful separation of excluded income and creditable foreign taxes | Easy to misread ACTC impact if Form 2555 is included | Highest; requires clean allocation between excluded income and creditable taxes | Mixing methods without tracing tax-to-income linkage |

A practical rule#

If refund potential matters most, model FTC first because filing Form 2555 makes ACTC unavailable under current Schedule 8812 form text. Then model FEIE and compare total U.S. tax against the lost ACTC.

Do not treat FEIE as a casual toggle. Once chosen, it continues unless revoked. Revocation generally blocks re-choosing FEIE for the next 5 tax years without IRS approval.

Model both scenarios before filing#

When the answer is not obvious, run both returns before you decide:

- Return with Form 2555.

- Return with Form 1116.

- Compare total U.S. tax, ACTC result, and whether excess foreign taxes may be carried back or carried over under FTC rules.

Get professional review before finalizing if your facts are complex, especially when allocation between excluded income and creditable taxes is not straightforward. You might also find this useful: A Guide to the Child Tax Credit for US Expats. Before you choose FEIE or FTC, document your travel days and tax-home facts in one place with the Tax Residency Tracker.

Your Executive Playbook: Making the Final Call#

The cleanest way to make this choice is to work in order: verify eligibility evidence, classify your tax environment, then choose FEIE or FTC.

Step 1. Confirm eligibility first#

Confirm eligibility first, because if your Schedule 8812 support is weak, path modeling is wasted effort.

| Checklist item | What it confirms | Article detail |

|---|---|---|

| Child SSN record | Timely SSN issuance | Valid work-authorized U.S. SSN issued before the return due date, including extensions |

| Support records | Child did not provide over half of their own support | Use before filing to confirm the support test |

| Residency evidence | Child lived with you more than half the year | Examples include school, medical, daycare, or social-service records |

| Draft return | Child is claimed as a dependent | Check dependency treatment before filing |

| Current dependency criteria after verification | Year-specific dependency rules | Confirm any current dependency criteria before filing |

A qualifying child generally must be under 17 at year-end. You also need to show the child lived with you more than half the year, did not provide more than half of their own support, is claimed as your dependent, and has a valid work-authorized U.S. SSN issued before the return due date, including extensions.

Documents to confirm before filing include:

- Child SSN record showing timely issuance

- Support records showing the child did not provide over half of their own support

- Residency evidence, such as school, medical, daycare, or social-service records

- Draft return showing the child is claimed as a dependent

- Any current dependency criteria after verification

If you cannot assemble SSN proof and basic residency or support evidence quickly, pause and fix that before filing.

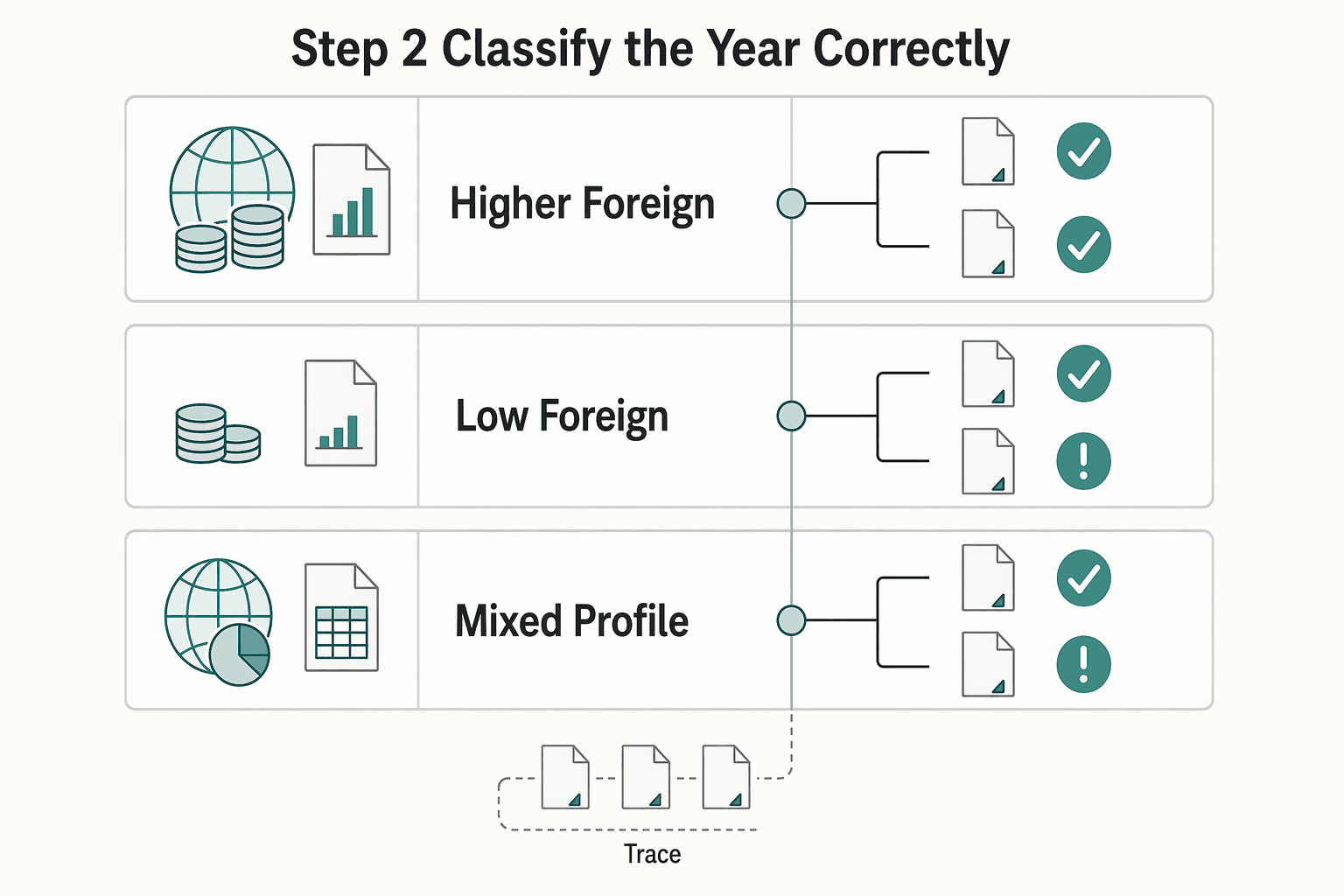

Step 2. Classify the year correctly#

Classify the year by how your income and foreign taxes line up, not by the country label. A simple matrix helps:

| Profile | Fact pattern | Start by modeling |

|---|---|---|

| Higher-foreign-tax profile | You paid meaningful foreign income tax on foreign-source income you will report on Form 1040 | FTC first |

| Low-foreign-tax profile | You have little creditable foreign income tax | FEIE first |

| Mixed profile | You have blended facts | Do not make a country-level shortcut decision |

Use the matrix as a starting point, not a shortcut:

- Higher-foreign-tax profile: Model FTC first.

- Low-foreign-tax profile: Model FEIE first.

- Mixed profile: Do not make a country-level shortcut decision.

Before you choose, pressure-test your facts for common trouble spots:

- Mixed-income household: Confirm which spouse has earned income and whether one or both spouses would file Form 2555. Separate Form 2555 is used for each spouse claiming FEIE or housing benefits.

- Self-employment plus wages: Do not assume one method fits all income types.

- Multi-country year: Trace taxes to the related income carefully. Do not claim FTC on taxes tied to excluded income, because one or both FEIE or housing elections may be considered revoked.

Step 3. Choose the filing path#

Choose the filing path only after Steps 1 and 2 are documented.

| Path | Choose this path if | Avoid this path if | Forms to prepare | Main risk |

|---|---|---|---|---|

| FTC route | You can document creditable foreign taxes on income reported on Form 1040 and you want to keep the ACTC path open if other tests are met, including the $2,500 earned-income minimum. | Foreign taxes are minimal, unclear, or mostly tied to income you plan to exclude. | Form 1040, Form 1116, Schedule 8812 | Weak tax-to-income tracing or claiming credit on excluded income |

| FEIE route | Excluding eligible foreign earned income tests better in your model. | ACTC refund access is material to your outcome, because filing Form 2555 blocks ACTC for that year. | Form 1040, Form 2555 | Losing ACTC eligibility for the year |

| Pause and model both | Facts are mixed, such as spouse-income asymmetry, self-employment, multi-country year, or midyear changes. | You are relying on last year's setup or assumptions. | Two draft returns: FEIE version and FTC version | Filing the wrong method, then dealing with FEIE revocation or re-election complexity, including the 5-tax-year re-election restriction without IRS approval |

Use these guardrails:

- Model both paths when the result is not clearly better on paper.

- Pause filing if FEIE qualification timing is incomplete and Form 2350 may be needed.

- Involve a qualified cross-border tax professional before submission when FEIE revocation or re-election decisions are in play, especially if your facts are mixed across countries or income types.

For a step-by-step walkthrough, see A Deep Dive into the Foreign Tax Credit (Form 1116). If your case includes multiple countries or mixed income types, use contact to sanity-check your filing path before you submit.

Frequently Asked Questions

What is the difference between CTC and ACTC?

The CTC is nonrefundable, so it can reduce your U.S. tax to zero but not below zero. The ACTC is the refundable part of the child credit rules, so it may still produce a refund even when you owe no income tax. Both are calculated on Schedule 8812 with Form 1040.

How do FEIE, FTC, and earned income change your additional child tax credit result?

Filing Form 2555 through FEIE blocks ACTC for that year. FTC, generally claimed on Form 1116, does not automatically block ACTC, but you still must qualify and have at least $2,500 of earned income reported on Form 1040/1040-SR. You also cannot claim FTC on income you excluded under FEIE.

Do you need Social Security numbers to claim this credit?

Yes. The child must have a valid SSN for U.S. employment issued by the return due date, including extensions, and a child ITIN or CRBA does not replace that requirement. Beginning in tax year 2025, IRS instructions also state you must have a valid SSN to claim the CTC or ACTC. On a joint return, one filer must have a valid SSN, while the other may have an SSN or ITIN.

Do income limits still matter if you otherwise qualify?

Yes. The credit can still phase down even if you meet the other eligibility tests. In IRS materials for tax year 2025, the phaseout thresholds are $200,000 for most filing statuses and $400,000 for joint filers. Verify the exact thresholds in the Schedule 8812 instructions for the year you are filing.

When should you bring in a tax professional?

Bring in a qualified tax professional before filing if you have mixed income types, a partial exclusion setup, unclear filing status, or a mixed FEIE and FTC profile. These facts can make the interaction between Form 2555, Form 1116, and Schedule 8812 harder to review. Share a draft return, child SSN records, your income breakdown, and foreign tax documents tied to income reported on Form 1040.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Child Tax Credit for U.S. Expats: Eligibility, FEIE, and Filing Checks

Claiming the Child Tax Credit from abroad is manageable when you treat filing as a sequence of gates, not a refund chase. Prove eligibility first, build support documents second, file third, and escalate as soon as one gate is unclear.