Quick Answer

Yes - south africa section 10(1)(o)(ii) can apply only when your file shows employee remuneration for services rendered outside South Africa and both day thresholds are met in one 12-month period. File as a resident on worldwide income, disclose foreign earnings, and claim only the supported exempt portion. Keep a live travel log, contract and payslip evidence, and IRP5 alignment, then retain records for five years in case SARS requests support.

The Section 10(1)(o)(ii) Strategic Playbook: A Deep Dive#

Use this exemption only when three facts are true at the same time: you are a South African tax resident, you earn employment remuneration for services rendered outside South Africa on behalf of an employer, and you meet the days test. That first screen helps you avoid two common failures: treating contractor income as eligible, and assuming overseas work means no return is required.

This exemption is narrower than simply "working abroad." SARS frames it for an employee rendering services outside South Africa for an employer. It also excludes some public-sector categories, including employees of national, provincial, or local government and certain public entities.

The days test has two thresholds, and both must fall within the same 12-month period. You need more than 183 full days outside South Africa in aggregate and a continuous period of more than 60 full days outside South Africa. The capped regime took effect on 1 March 2020. SARS guidance references a cap of R1,25 million, and foreign employment income above that cap is subject to normal tax in South Africa. For planning and filing, verify the cap that applies for your filing year.

Your first eligibility screen#

Start with the employment question. If you are clearly an employee, this may apply. If you are an independent contractor, freelancer, or self-employed consultant billing in your own name, it does not. SARS explicitly excludes independent contractors from section 10(1)(o)(ii).

| Decision signal | Usually points to employee | Usually points to contractor |

|---|---|---|

| Who you render services for | You render services outside South Africa on behalf of an employer | You render services as an independent contractor |

| Income type | Employment remuneration | Contractor fees or similar non-employment income |

| SARS scope under section 10(1)(o)(ii) | Potentially in scope (if the days test is also met) | Excluded from scope |

Labels alone are not enough. If your facts are mixed, get advice before claiming the exemption.

What to do at filing time#

The key point at filing is simple: exempt does not mean invisible. South African tax residents are generally taxed on worldwide income, and SARS indicates that in most instances a resident working overseas will still need to submit a return.

| Item | Article detail |

|---|---|

| Foreign employment income | Reflect foreign employment income and claim the exemption only where the facts support it |

| Records you relied on for filing | Keep the records you relied on for filing, including documents related to income declared and deductions claimed |

| Supporting documents | Retain supporting documents for five years from the return submission date |

| Supporting documents with the return | Do not submit supporting documents with the return unless SARS requests them |

| Before filing | Confirm employee status, both day thresholds within one 12-month period, and the current filing-year cap |

Do not leave day counting to filing season. If this exemption is in play, the next job is execution: track days accurately throughout the year. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Part 1: Your Compliance Dashboard - Mastering "Day Counter Hell"#

If you want this position to hold up, keep an audit-ready log. It should prove where you were, whether you were rendering services abroad as an employee, and whether both day tests are met in the same 12-month window. When you keep this live, filing becomes a verification exercise instead of a memory exercise.

Build the tracker before you need it#

Your tracker should let you answer two questions at any time: do you still meet the day tests, and what remuneration ties to those periods?

A basic spreadsheet is enough if it stays clean and current. Use one row per trip or location change, with these fields:

- departure date from South Africa

- return date to South Africa

- country or countries worked from

- employer name

- employment status note if anything changed during the year

- whether services were rendered outside South Africa during that period

- whether remuneration was earned for that period

- links or file names for supporting evidence

- rolling 12-month total days outside South Africa

- longest continuous outside-South-Africa period in the tested window

- notes for unusual periods, for example unpaid leave, sick leave, or split duties

A few data hygiene rules matter more than people expect:

- update as travel happens, not weeks later

- keep one date format throughout

- never overwrite old entries; add correction notes

- tie each row to evidence you can retrieve later, such as travel records, calendar records, payroll records, and passport copies

One practical cadence is weekly reconciliation, plus a monthly check against payroll or payslips so your day log and remuneration record stay aligned.

Use a compact decision aid#

Borderline files go wrong because the legal frame is narrower than the travel pattern. This exemption applies to a South African tax resident who is an employee, renders services outside South Africa for an employer, and meets both day thresholds in the same 12-month period. Those thresholds are more than 183 days outside South Africa and a continuous period of more than 60 full days outside South Africa.

| Situation | Log treatment | Action |

|---|---|---|

| Outside South Africa, employed, and rendering services abroad for an employer | Count as potentially qualifying time | Keep travel and remuneration support together |

| Outside South Africa but no remuneration earned for that period | Do not treat it as qualifying under this section | Flag for review; Interpretation Note 16 indicates these periods fall outside the ambit |

| Employment with national, provincial, or local government, or certain public entities | Do not assume standard eligibility | Escalate early for specific advice |

| Entry or exit day, or other partial-day edge case | Do not guess | Confirm current criteria in the primary legal source before filing |

If you hit interpretation issues, use Interpretation Note 16 as your primary guide, not FAQ text alone.

Think in rolling windows, not tax years#

This is where good logs outperform good intentions. "Any 12-month period" means your result can change even when your past travel does not. On any date, you should be able to look back 12 months and test both thresholds inside that window.

A long foreign work stretch can satisfy the test in one month, then become tighter a few months later as early days drop out of the rolling window. A short return trip can also break the continuous-period test if your qualification depends on one uninterrupted block abroad.

Model trips before you book them#

Before you book a South Africa trip, test the effect before you commit. That matters most when you are close to either threshold or relying on one long continuous period abroad. Run this checklist:

- test proposed dates against rolling 12-month totals and your continuous outside-South-Africa period

- check whether you will render any services in South Africa during the broader remuneration period

- confirm the period you are counting is still paid employment time

- verify whether your employer category needs special treatment

- save draft itineraries in the same evidence structure you use for final records

Get professional advice before filing if you are close to either threshold. Do the same if you had unpaid periods abroad, received remuneration after the main work period with possible apportionment, moved between employee and contractor status, or may be deemed exclusively resident in another country under a treaty. Related: Malaysia's DE Rantau Nomad Pass: A Guide for Applicants.

Before you lock travel dates, map your rolling-window plan in one place so you can catch day-count risk early with the Tax Residency Tracker.

Part 2: Your Optimization Engine - From Compliance to Financial Strategy#

Optimization under section 10(1)(o)(ii) is mostly operational: keep the facts clean, keep the proof clean, and file a position you can defend. Once your day tracker is stable, your main levers are documentation quality, work-location planning, and payroll-to-return consistency.

You can meet the day tests and still create avoidable risk. The easiest years to defend usually have clear foreign-service evidence, clear leave-versus-work days in South Africa, and remuneration records that map to those facts.

Build an audit-ready documentation system#

Documentation quality often separates a clean file from a messy one. SARS requires records to be kept in original form, in an orderly way, and in a safe place, with a standard five-year retention period from return submission. Treat that as your minimum standard and run one evidence pack per tax year. Use these document groups:

| Document group | Include |

|---|---|

| Employment and status | Employment contract, amendments, assignment letters, role-change records, and anything showing services were rendered by way of employment |

| Travel and location | Your travel log plus supporting travel or location records that help prove where you were on specific dates |

| Work-location evidence | Calendar records, leave approvals, timesheets, or employer communications showing whether you were working abroad, on leave in South Africa, or working while physically in South Africa |

| Remuneration and payroll | Payslips, payroll summaries, salary receipts, annual tax certificates, and withholding correspondence, aligned to the same periods used in your travel and work log |

| Filing and SARS correspondence | Filed return, assessment outcomes, objections if any, and proof used for positions involving payroll directives or foreign tax credit claims |

If your employer is in government or certain public entities, escalate early because standard treatment may differ.

SARS record-keeping guidance focuses on keeping records, so set your own filename and version rules and keep them consistent. Do not overwrite material used for filing. Version your updates and keep prior copies.

Treat apportionment as a calculation framework, not a guess#

If any services are performed in South Africa during the remuneration period, do not assume the full amount qualifies. SARS guidance indicates the exemption can be subject to apportionment, and Interpretation Note 16 indicates periods outside South Africa with no remuneration earned fall outside scope. Plan the calculation in this order:

- total remuneration for the tested period

- the portion linked to qualifying foreign services, using the legally correct apportionment basis for your facts

- the applicable exemption cap for the filing year

SARS states the exemption is limited to R1.25 million, and notes that remuneration above that level can create double-tax exposure.

| Work pattern | Risk level | Likely implication |

|---|---|---|

| Services rendered abroad, South Africa visits are leave-only | Low | Easier to defend foreign-service treatment, still subject to the cap and day tests |

| Short South Africa trip with some work activity | Medium to high | Apportionment risk increases; full exemption is harder to defend |

| Material services physically performed in South Africa | High | A larger non-exempt portion is likely |

| Time outside South Africa with no remuneration earned | High | Those periods generally do not support exempt remuneration |

Align payroll handling with filing reality#

Payroll can help or hurt you here. If standard withholding does not match your cross-border facts, an employer may apply for an IRP3(q) directive for a different withholding basis. Final section 6quat foreign tax credit relief, however, is handled on assessment when you file and provide proof.

| Timing | Action |

|---|---|

| Before travel | Label each planned South Africa day as leave or work; if mixed, model the apportionment impact before booking |

| Before payroll year-end | Reconcile travel, work-location records, and remuneration period by period |

| Before filing | Lock the evidence pack, spot-test dates to supporting records, and re-check day-test and employee-status positions |

| Talk to a qualified tax adviser | If terms of employment changed, roles were mixed, income timing or structure is mixed across locations, the employer category may be restricted, or payroll withholding does not match your likely filing position |

You might also find this useful: How to Obtain an 'Individual Tax Number' (ITN) in South Africa.

Part 3: Your Risk Mitigation Protocol - The Contingency Plan#

When the facts change, stop optimizing and switch to contingency mode. Lock the current record set, note exactly what changed, and decide whether you are still executing the same response plan.

Use this trigger protocol:

- Day-count risk changed

Re-run the rolling 12-month totals and the continuous-period test before you rely on the exemption.

- Work pattern changed

Separate South Africa workdays from South Africa leave days and update any apportionment view.

- Status or employer category changed

Pause assumptions and confirm whether you are still within an employee fact pattern and whether your employer category needs special treatment.

- Payroll and filing no longer match

Reconcile payroll, remuneration periods, and work-location records before filing.

Keep a short annual risk log with the trigger, impact, owner, next action, and proof required. Review it regularly so your filing position does not drift away from the underlying facts.

When operational controls enter the picture#

If your file starts to get messy, separate the controls before you try to merge them into one answer. In practice, that means four tracks:

- a locked travel-day log

- work-location records showing whether South Africa days were leave or work

- remuneration records mapped to the same periods

- payroll and filing records that tell the same story

Problems usually appear when one track is updated and the others are not. A clean return position depends on those records lining up.

If you may have missed a required trigger condition#

Act immediately and run a controlled response:

- Re-run the day tests using the rolling 12-month window you are actually relying on.

- Recheck the work pattern to see whether any South Africa days involved services rather than leave.

- Reconcile remuneration to the periods that still qualify, and update any apportionment analysis.

- Lock the revised evidence pack and decide whether you still have a defensible exemption claim.

The main failure pattern is drift: the facts changed, but your filing logic did not.

If your response depends on paper-only controls#

Do not rely on a neat paper file if your travel records, calendar, payroll, or passport evidence point the other way. Use controls you can verify in practice: dated entries, consistent records, retrievable support, and a return position that matches what actually happened.

When to escalate#

Escalate early if you are close to either day threshold, had unpaid periods abroad, changed between employee and contractor status, may fall into a restricted employer category, performed services in South Africa during the remuneration period, or your payroll withholding does not match your likely filing position. If published guidance does not resolve the technical point, get advice before you file.

Conclusion: You Are the CEO of Your Compliance#

Your goal is not to force an exemption result. Your goal is to file a position you can defend, using consistent facts on residency, travel days, and where services were rendered.

- Track the right inputs: Maintain one rolling 12-month travel log and one work-location record. Use them to test the core thresholds: more than 183 days outside South Africa in a 12-month period, plus one continuous period exceeding 60 days, and whether your remuneration is from employment rather than independent contracting. This lowers the risk of failing eligibility late.

- Decide residency first: Because South Africa taxes residents on worldwide income, and has done so on a residence basis since 1 March 2001, confirm your tax-residency position before applying section 10(1)(o)(ii). This prevents weak downstream decisions when ordinary residence is unclear.

- Report in a way that reconciles: At filing time, make sure your IRP5 treatment and remuneration file clearly distinguish services rendered inside versus outside South Africa. This reduces mismatch risk across payroll, return data, and support records, and keeps the post-1 March 2020 capped exemption regime (up to R1,25m for qualifying cases) in view.

What to do next#

- Keep one evidence pack updated through the year: travel timeline, employment and remuneration records, payroll mapping, and work-location reconciliation.

- Review your travel and work pattern before the next filing cycle, not after year-end.

- Pre-check your assumptions against current SARS guidance on residency, employee status, and day-count interpretation.

- Confirm your IRP5 treatment aligns with where services were rendered.

If your facts are mixed, changed mid-year, or still uncertain, pause and confirm treatment with a qualified tax professional before filing. Default to defensible documentation and a repeatable process over aggressive tax positioning.

If your contracts, travel pattern, and filing obligations now span multiple countries, discuss a safer operational setup with Gruv.

Frequently Asked Questions

How do you know if south africa section 10(1)(o)(ii) is even in scope for you?

Start with scope, not calculation. Confirm that you are a South African tax resident, that you are acting in an employee capacity, and that the income relates to services rendered outside South Africa during qualifying periods. Then validate that against your contract, remuneration records, and payroll treatment. If those facts do not line up, pause this exemption path and review alternatives first.

How should you handle the day-count test?

Use a strict sequence so the file stays defensible. First confirm the current SARS thresholds and counting method, then lock a travel log for the relevant period, then test eligibility against that locked record. Keep a clear note to verify the current SARS interpretation before you file, because SARS states its FAQ is explanatory and may be updated.

Do weekends, leave days, and edge travel dates count?

Do not guess or recycle old assumptions. Check the latest SARS material, apply one counting method consistently across the full period, and keep source proof for edge dates. If an arrival or departure date is uncertain, keep both scenarios visible until you resolve the conflict.

What do you do if you worked partly in South Africa and partly abroad?

Work through it in order: confirm eligibility, assess how remuneration should be treated when services were rendered in different locations, then report from one reconciled workday-to-pay-period file. Keep the current exemption cap visible in your model and verify it before filing. SARS states the capped regime applies from 1 March 2020. Older guidance refers to R1,25 million, so confirm the current position for the filing year you are dealing with.

What if you are a contractor, freelancer, or somewhere in between?

Treat this as a facts-and-evidence decision, not a label decision. If your records support an employee fact pattern, this exemption may be in scope. If your records show invoice-based, self-billed work, do not assume that it is. Where status is mixed or changed mid-year, document the facts, pause the exemption position, and run an alternative-route review early.

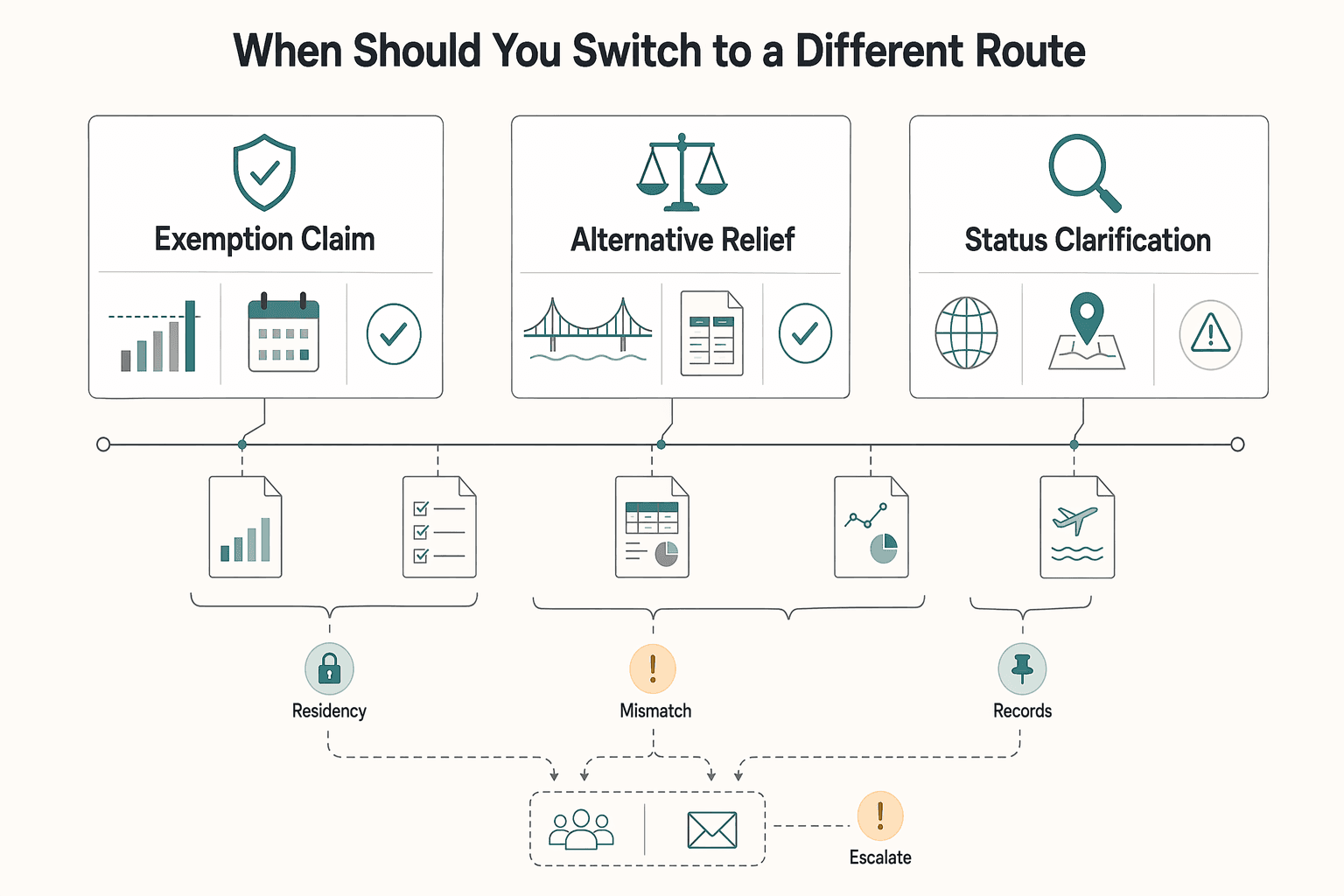

When should you switch to a different route?

Switch when your exemption position is capped, unclear, or not supported by your facts. Keep one timeline, one income bridge, and one evidence pack so every route is tested on the same facts. If published guidance does not resolve a technical issue, escalate to an adviser or send the question to [email protected]. | Route to review | Trigger | Primary dependency | Documentation burden | Fallback path | | --- | --- | --- | --- | --- | | Exemption claim | You appear to be a tax-resident employee with foreign services during qualifying periods | Current SARS interpretation plus coherent employee and travel facts | Moderate: contract, remuneration records, payroll mapping, travel log, travel proof | If capped, unclear, or unsupported, move to alternative relief review | | Alternative relief review | Exemption does not fully resolve your position, or exemption facts are weak | One consistent residence, income-period, and work-location fact pattern | High: full timeline, income mapping by period, contracts, supporting records | If route assumptions break, re-baseline facts and seek specialist review | | Status clarification first | Employee versus contractor position is unclear or changed mid-year | Actual legal and commercial facts in your file | High: contracts, invoices, payment trail, payroll records, engagement history | Once status is clear, reassess exemption scope or pivot routes |

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/119/crec/2025/12/16/171/212/CREC-2025-12-16.pdftrusted

- dhs.wisconsin.gov/familycare/mcos/pace-2026-contract.pdftrusted

- eeoc.gov/laws/guidance/enforcement-guidance-retaliati...trusted

- federalregister.gov/documents/2026/02/27/2026-03962/employee-or-...trusted

- fsa.usda.gov/Internet/FSA_File/1-flp_r01_a236.pdftrusted

- grants.nih.gov/grants/how-to-apply-application-guide/forms-...trusted

- sars.gov.za/individuals/tax-during-all-life-stages-and-e...trusted

- sars.gov.za/faq/faq-am-i-required-to-submit-an-income-ta...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Malaysia DE Rantau Nomad Pass Application Playbook

Low risk starts with one rule: separate what third-party and community sources say from what you have personally verified on the live official application path. This guide follows that rule so you can plan your move without treating summaries or walkthrough videos as policy.

How to Get or Retrieve a SARS Income Tax Reference Number in South Africa

---