Quick Answer

Use the Firewall Principle: keep your Personal/Business Pocket and Retirement Pocket separate in every deal. A solo 401k prohibited transactions problem starts when value, services, or credit flows to you or another disqualified person instead of the plan. Before signing, complete party-status, benefit, and exemption checks. If a violation appears, document the facts, unwind or neutralize the transaction, restore the plan financially, and then complete Form 5330 steps with specialist review.

To use a Solo 401(k) well, you do not need to memorize dense IRS code. You need one clear mental model: the Firewall Principle. It creates a hard legal and financial boundary between two separate worlds: your Personal/Business Pocket and your Retirement Pocket.

A solo 401(k) prohibited transaction is any action that breaks that firewall by letting value, services, or benefits flow the wrong way between those two pockets. Once you internalize that, the rules become much easier to apply in real deals.

The Foundation: Defining Your Firewall#

Start every deal with one rule: do not let plan assets provide a current benefit to you or any disqualified person. When you screen for prohibited transactions, ask first: who benefits right now? If the answer is anyone other than the plan, pause before money moves.

A one-participant 401(k) follows the same core rules as any other 401(k). Under IRC §4975, a prohibited transaction is a direct or indirect transaction between the plan and a disqualified person, including self-dealing by a fiduciary. That includes direct or indirect sale, exchange, lease, lending, extension of credit, furnishing of goods, services, or facilities, or transfer or use of plan assets for a disqualified person's benefit.

In practice, potential violations often show up in ordinary documents: the counterparty, the ownership structure, and the service terms.

| Party | Disqualified status | Why it matters for your decision |

|---|---|---|

| You, as plan fiduciary | Yes | You cannot deal with plan assets in your own interest or for your own account. |

| Your spouse | Yes | A spouse is explicitly included in the family disqualified-person list. |

| Your ancestors | Yes | Ancestors are explicitly included. |

| Your lineal descendants and any spouse of a lineal descendant | Yes | This group is explicitly included. |

| A person providing services to the plan | Yes | Service relationships can create prohibited transactions if the deal benefits a disqualified person. |

| An entity connected by ownership/control to you or another disqualified person | Often yes, fact-dependent | IRC §4975 includes 50%+ ownership tests and some 10%+ officer/shareholder/partner tests; confirm the current test that applies before acting. |

Foundation rules

- Ask first: who gets the current benefit?

- Identify every party on both sides of the transaction.

- Check family and service-provider status early.

- Verify entity ownership and control percentages in writing.

- If status is unclear, stop and resolve it before proceeding.

Your Strategic Toolkit: The Pre-Transaction Compliance Checklist#

Most problems surface before closing, not after. The safest approach is to run the same four checks before every transaction and not move money until each one is clear.

Four questions to ask before you sign or fund anything#

- Have you verified every party's status and relationship to the plan?

If all parties are identified and documented well enough to test party-in-interest risk, Proceed. If a party appears to be a party in interest and you have not resolved how the transaction is permitted, Pause. If ownership, control, or role is unclear, Escalate.

- Is this action clearly within fiduciary responsibility, rather than mainly a business decision?

If the action is clearly documented as a fiduciary decision for the plan, Proceed. If the purpose or role is mixed, Pause. If it is unclear whether ERISA fiduciary obligations apply, Escalate.

- Is exemption status clear before execution?

If the transaction is clearly permitted without an exemption, or any required exemption is identified and documented, Proceed. If exemption status is unresolved, Pause. If someone says an exemption applies, Escalate and verify the exact exemption against the official Federal Register edition/PDF before execution.

- Does anyone outside the plan get a current benefit from this transaction?

If the benefit stays with the plan and no current side benefit is created, Proceed. If a current personal or insider benefit appears in the structure, Pause. If benefit flow is arguable or indirect, Escalate.

As of February 2025, EBSA guidance still frames prohibited-transaction enforcement under ERISA Section 406, focusing on party-in-interest status and whether an exemption applies. Your pre-close file should answer both points before execution.

| Risk signal | Why it is risky | What compliant handling looks like |

|---|---|---|

| Counterparty status is unclear | You cannot complete a party-in-interest test without clear facts | Confirm role, ownership, and control in writing before signing |

| Fiduciary role vs. business decision is unclear | ERISA fiduciary obligations may depend on that distinction | Document decision purpose and escalate when classification is unclear |

| Exemption basis is unclear | Investigators test whether a statutory or regulatory exemption applies | Stop and verify the exemption basis before closing |

| Current benefit flows to an insider | Fiduciary standards focus on acting solely for participants/beneficiaries | Remove current side benefit or do not proceed |

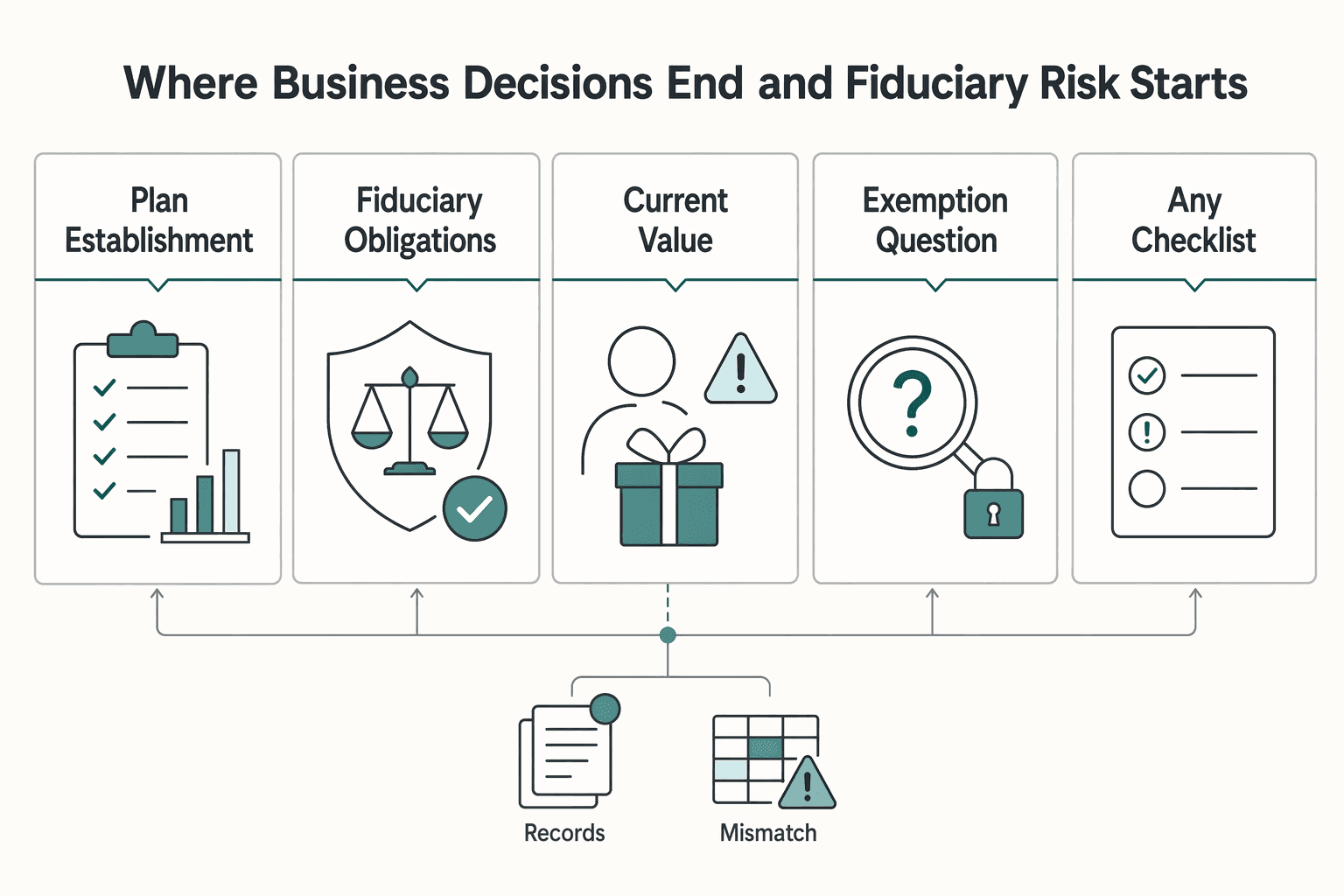

Where business decisions end and fiduciary risk starts#

This is a practical risk checkpoint. GAO notes that some plan-establishment decisions are mainly business decisions and may seldom involve ERISA fiduciary obligations. But when fiduciary obligations do apply, the standard is prudent action solely in participants' and beneficiaries' interests.

| Trigger | Article guidance | Next step |

|---|---|---|

| Plan-establishment decisions | Some are mainly business decisions and may seldom involve ERISA fiduciary obligations | Use this line as a practical risk checkpoint |

| Fiduciary obligations apply | The standard is prudent action solely in participants' and beneficiaries' interests | Apply that standard |

| Current value appears to reach you or another insider | Treat that as a risk signal | Escalate |

| An exemption question is in play | Verify the legal text in the official Federal Register edition/PDF before execution | Verify before execution |

| Any checklist answer is not clean | Stop the transaction and document what you know and what you do not know | Get specialist review before execution |

If your actions appear to create current value for you or another insider, treat that as a risk signal and escalate.

If any checklist answer is not clean, stop the transaction, document what you know and what you do not know, and get specialist review before execution.

Related: How to Structure Your Solo 401(k) to Make Alternative Investments (Real Estate).

Before you execute a borderline transaction, document the business side separately and keep a clean client paper trail using the Free Invoice Generator.

Reinforcing the Firewall: Navigating Sophisticated "Gray Areas"#

Gray-area deals are where mistakes often happen. The structure may look normal, but the prohibited-transaction rules still apply to both direct and indirect benefit flows. In a one-participant plan, the key question is not just whether the plan can invest. It is who gets current value from the deal.

| Scenario | Likely compliant pattern | Likely prohibited pattern | What to verify before acting |

|---|---|---|---|

| You are a licensed agent or advisor on a plan purchase | An independent third party performs transaction services; you stay in plan administration | You or your firm provides deal or asset services, whether compensated or not | Engagement letters, invoices, role split, actual service provider |

| You and the plan invest in the same offering | Same timing, same economics, same core documents, proportional treatment | Side letters, better terms for one side, or personal consideration tied to plan participation | Subscription docs, cap table, side letters, fee disclosures, capital call/distribution terms |

| Your firm could improve or manage a plan asset | Independent vendor is retained and paid by the plan | Your personal labor, or services from an entity tied to you, furnish services to the asset | Vendor independence, ownership/control map, service agreement, payment records |

| Plan invests in a company tied to your network | Investment stands on its own; no current insider benefit | Structure is expected to create a current job, fee stream, liquidity relief, or similar insider benefit | Use of proceeds, compensation plans, related-party arrangements, benefit-flow memo |

Sweat equity#

This is one of the fastest ways a gray area becomes a real compliance problem. If you are a disqualified person, services by you to plan assets are a core risk pattern. Services from entities tied to you can raise similar risk and should be reviewed carefully. That is true even if you are only helping or not billing for the work.

Use a simple line: you can administer the plan, but you should not be the person whose labor changes asset value or deal economics. If you are the agent, contractor, advisor, or founder, treat role drift as a red flag and lock responsibilities in writing before closing.

Co-investing#

Co-investing is not automatically prohibited, but it does require a clean structure check before you commit. Shared ownership is not the issue by itself. The problem is using plan assets in your own interest or receiving personal consideration connected to the plan transaction.

Run four checks before you invest: aligned entry timing, aligned economics, proportional follow-on treatment, and arm's-length documentation. If you are also connected to the issuer, for example as founder, advisor, or board participant, tighten the review early. Conflicts can show up after signing through fees, compensation, or special rights.

Indirect benefits#

This is where substance matters more than labels. A deal can look clean on paper and still fail if the real effect is to route current value to you or another disqualified person.

| Gray area | Core risk | What to check |

|---|---|---|

| Sweat equity | Services by you to plan assets are a core risk pattern; services from entities tied to you can raise similar risk | Whether your labor changes asset value or deal economics; lock responsibilities in writing before closing |

| Co-investing | Using plan assets in your own interest or receiving personal consideration connected to the plan transaction | Aligned entry timing, aligned economics, proportional follow-on treatment, and arm's-length documentation |

| Indirect benefits | A deal can look clean on paper and still fail if the real effect is to route current value to you or another disqualified person | Intent and outcome; all counterparties and benefit flows |

Screen for both intent and outcome. Would you still do the deal if no related person received a current advantage? After funds move, who benefits first?

If the real effect is to deliver current value to you or another disqualified person, treat that as a stop signal. When the facts are ambiguous, pause, document all counterparties and benefit flows, and send the file for specialist review before closing.

You might also find this useful: Can I have both a SEP IRA and a Solo 401(k)?.

What Happens When the Firewall is Breached: A Correction Protocol#

If you identify a breach, switch to correction mode immediately. Your job is simple: stop further harm, correct the transaction, and show that the plan was restored so it is not financially worse off.

| Tier | What the article says |

|---|---|

| Initial excise exposure | 15% of the amount involved for each year, or part of a year, in the taxable period |

| Escalated exposure if uncorrected | An additional 100% of the amount involved if the transaction is uncorrected during the taxable period |

| Practical plan-level risk | This rises if your records, valuation support, or correction proof are weak |

Use those three consequence tiers to set urgency. Before you compute tax or file, verify the current IRS prohibited-transaction rules and current Form 5330 instructions.

Lock down the incident first#

Start with an incident record. Capture the transaction date, parties, money or property transferred, who benefited, and why you now view it as prohibited. The transaction date matters because the taxable period begins there.

Then pause related activity while you review the facts. Continuing under the same arrangement can complicate correction.

Consider involving ERISA or tax counsel if facts are disputed, valuation is unclear, or related-party boundaries are uncertain.

Undo or neutralize the transaction and restore the plan#

Your correction standard is straightforward: undo the transaction as much as possible and restore the plan so it is not financially worse off.

If money or property moved improperly, unwind the transfer if possible. If a full unwind is impossible, neutralize the ongoing benefit and document why your fix is the closest practical restoration.

The real completion checkpoint is not paperwork. It is completed correction plus financial restoration of the plan. Do not treat the matter as closed until both are done.

Build the filing file before Form 5330#

Form 5330 is the reporting return, but the support file comes first. Assemble it before you prepare the form, and if any part is thin, fix the file before you file:

| Assemble this | What it must show |

|---|---|

| Transaction facts memo | Date, parties, what moved, and why the transaction was prohibited |

| Valuation support | How you determined the amount involved, including money moved and fair market value support |

| Correction evidence | Unwind or repayment records, revised agreements, and proof the plan was restored |

| Preparer review | CPA or specialist check that the filing matches facts and correction actions |

File Form 5330 and confirm filing mechanics#

Once your facts and correction file are complete, file Form 5330 and pay the applicable excise tax amount. Also confirm which participating disqualified person is liable for the tax.

Check current filing mechanics before you submit. E-filing may be required in some cases, including when the filer must submit at least 10 returns of any type during the calendar year the form is due. If needed, review the Form 8868 extension path (up to 6 months), and remember that correction is completed when the transaction is actually corrected.

For a step-by-step walkthrough, see SEP IRA vs Solo 401(k) for Freelancers With Uneven Cash Flow.

Conclusion: Build Your Firewall, Invest with Confidence#

Your best protection is a repeatable process. Treat every decision as a plan-first decision, then document it. Confidence here comes from consistency, not from testing edge cases.

Keep your standard direct. In ERISA-plan discussion, fiduciary duty is framed as acting in the sole interest of plan participants when choosing advisors. Apply that same discipline to your own review: does this transaction clearly serve the plan, or is it also solving a personal or business need right now? Use this short loop before any move:

- Run the Two Pockets test. Confirm which pocket pays, which pocket owns, and which pocket benefits today.

- Run the Pre-Transaction Checklist before signing or funding. Verify parties, services, money flow, and whether any current benefit reaches you.

- Save a compact evidence pack. Keep a dated decision note, agreement, pricing or valuation support when relevant, invoices, and payment proof in the plan file.

Use one decision rule throughout: if a transaction does not clearly benefit the plan, pause and verify before proceeding.

A practical way to make this stick is a one-page written conduct standard for your plan. Regulated investment-management settings use written codes of ethics as a core compliance control, and the same write-it-down habit can make your own process easier to apply consistently. Keep it short, use it every time, and prioritize documentation over speed.

For a deeper walkthrough, see Set Up a Solo 401(k) for Crypto With Audit-Ready Controls.

If you want a tighter system around client terms, payment steps, and records so retirement and business funds are less likely to blur, build your baseline workflow with the Freelance Contract Generator.

Frequently Asked Questions

Can you do repairs or improvements on property your plan owns?

Treat your own labor on plan-owned property as a high-risk move. Prohibited transaction categories include furnishing services, so unpaid sweat equity can create a self-dealing risk even if no cash changes hands. Use independent contractors, pay from plan funds, and keep contracts, invoices, and payment records in the plan file.

Can your plan invest in a company a family member runs?

Maybe, but do not skip the disqualified-person analysis. IRS retirement guidance names core relationships such as spouse, ancestor, lineal descendant, and a lineal descendant’s spouse, so other relatives are not automatically disqualified based on that list alone. Before you proceed, test benefit, ownership, and control. If the structure could benefit or be controlled by a disqualified person, pause for specialist review.

Can you take a loan from your one-participant plan?

Do not assume a 401(k) loan is automatically available to you. Lending money or extending credit is a prohibited category unless an exemption applies, and loan treatment depends on statutory conditions plus loan terms written into your plan document. Confirm the borrower, terms, and administration against the plan document and get professional review before acting.

How is a prohibited transaction different from UBTI or UDFI?

These are different regimes, so the fix depends on which rule you triggered. Prohibited transactions focus on barred dealings with disqualified persons. UBTI and UDFI are income-tax rules that can apply even when an investment structure is otherwise permissible. | Issue | What it is | What triggers it | Why it matters | Your next step | | --- | --- | --- | --- | --- | | Prohibited transaction | A barred transaction between the plan and a disqualified person | Loan/credit, services/facilities, or similar prohibited dealing with a disqualified person | Can trigger a 15% excise tax, plus an additional 100% tax if not corrected in the taxable period | Stop the activity, document facts, correct the transaction, and review Form 5330 requirements | | UBTI | Income from an unrelated trade or business | Unrelated trade or business income inside the plan | Creates potential tax/reporting exposure; it is not the same regime as a prohibited transaction | Measure income and review Form 990-T reporting | | UDFI | Income linked to debt-financed property | Acquisition indebtedness on income-producing property | Can create tax/reporting exposure under debt-financed-property rules | Trace the debt-financed share and review Form 990-T reporting |

What should you do first if you think you triggered one of these rules?

Act immediately, because IRS guidance ties prompt correction to avoiding the additional 100% tax layer, and the taxable period starts on the transaction date. Use this sequence: document the issue, including date, parties, amounts, property, and the suspected prohibited element, unwind and restore the plan position as much as possible, confirm and complete required Form 5330 reporting and payment steps, and involve tax or benefits counsel when valuation, related-party status, or unwind feasibility is unclear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/ebsa/about-ebsa/our-activities/enfo...trusted

- dol.gov/general/topic/retirement/fiduciaryresptrusted

- federalregister.gov/documents/2020/12/18/2020-27825/prohibited-t...trusted

- federalregister.gov/documents/2015/04/20/2015-08832/proposed-bes...trusted

- gao.gov/assets/a278251.htmltrusted

- irs.gov/retirement-plans/plan-participant-employee/r...trusted

- irs.gov/retirement-plans/plan-participant-employee/r...trusted

- sec.gov/rules-regulations/2000/11/revision-commissio...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

How to Structure Your Solo 401(k) for Real Estate and Crypto Investing

Before you place an alternative-asset trade in a one-participant 401(k), you need a decision process, not more generic retirement education. This guide helps you confirm plan fit, choose how control and diligence will work, document operating safeguards, and put filing checkpoints on the calendar before you execute anything. It is not legal or tax advice, and it does not assume one custody or checkbook-control setup works for everyone.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.