Quick Answer

Start by assuming form 8621 pfic reporting may apply whenever you directly or indirectly own a PFIC, then prove any exception with current IRS instructions. Make the filing decision before doing calculations: confirm trigger categories, map each ownership path, and verify Part I fields like share class, acquisition date, year-end shares, and value support. If election history or indirect data is incomplete, escalate before submission.

Three variables that control your Form 8621 filing decision#

Form 8621 is hard because filing can turn on three moving parts at once: your ownership status, your election posture, and what happened during the year, even if you did not sell. If you treat this as only a sale-or-no-sale question, you can miss a real filing trigger.

The IRS describes Form 8621 as the information return for shareholders of a PFIC or QEF. In practice, triggers can include certain direct or indirect distributions, gain on disposition, reporting tied to a QEF or section 1296 mark-to-market election, and the section 1298(f) annual report requirement.

Use this sequence rather than a one-shot form approach:

- Decide whether you likely need to file this year based on ownership and the IRS trigger categories.

- Decide which reporting path fits your facts, including whether Part II elections are relevant.

- Decide whether your records are strong enough to self-prepare or whether uncertainty is high enough to escalate.

Start with current IRS materials, not memory. The IRS About Form 8621 page was last reviewed on 19-Mar-2026 and the current form is Form 8621 (Rev. December 2025), so confirm that you are using the current form and current instructions.

Also separate filing duty from calculation difficulty. Filing duty is usually a fact-pattern decision. Calculation quality depends on records. For each holding, verify the class of shares, acquisition date, year-end share count, year-end value, and whether shares were jointly owned with a spouse.

Finally, do not guess on elections. Form 8621 includes Part II elections, and practitioner commentary warns that missing an available election can be expensive. Late-election cleanup can also be difficult. For related planning, see A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues.

What PFIC means and why Form 8621 exists#

A PFIC is a foreign investment company category that can trigger U.S. shareholder reporting, and Form 8621 is the IRS information return for a shareholder of a PFIC or Qualified Electing Fund.

This is not just a sale form. A direct or indirect PFIC shareholder may need to file if you:

- receive certain direct or indirect PFIC distributions

- recognize gain on a direct or indirect disposition of PFIC stock

- report information for a QEF or section 1296 mark-to-market election

- make an election reportable in Part II

- are required to file an annual report under section 1298(f)

So the real question is not just, "Did I sell?" It is, "Did I hold a PFIC in a way that created a reporting event or annual reporting duty?"

The form also captures core reporting details. Part I asks for each class of shares, whether shares were jointly owned with a spouse, and the number of shares held at year end. If value is more than $200,000, you list the value. If you cannot support share class, year-end share count, and value, treat that as a verification gap before deciding that no filing is required.

One early red flag matters here. Former PFIC status can stay sticky. IRS materials note that a former PFIC or section 1297(e) PFIC shareholder continues under section 1291 treatment unless a purging election is made. That means classification, ownership path, and election history need to be checked together. For more background, see A Deep Dive into PFIC Rules for US Expats Investing Abroad.

Decide if you likely need to file this year#

If you are a U.S. person with direct or indirect PFIC share ownership, start from a conservative position. Treat Form 8621 as likely required unless the current Instructions for Form 8621 clearly support a documentable exception.

Test your facts against IRS triggers#

A filing duty can arise if your facts match any of these IRS trigger categories:

| Trigger category | What the section says | Article note |

|---|---|---|

| Certain PFIC distributions | Received certain direct or indirect PFIC distributions | A filing duty can arise |

| Disposition gain | Recognized gain on a direct or indirect disposition of PFIC stock | A filing duty can arise |

| QEF or section 1296 reporting | Reporting information with respect to a QEF or a section 1296 mark-to-market election | A filing duty can arise |

| Part II election | Making a Part II election | Listed as a filing trigger |

| Section 1298(f) annual report | Required to file an annual report under section 1298(f) | Listed as a filing trigger |

That is why no sale or distribution does not automatically mean no filing. Absent an exception, practitioner guidance describes Form 8621 exposure as generally per PFIC, per year, including years with no distributions or sales.

Use Part I as a readiness check. Before deciding you are out, confirm that you can support each PFIC record Form 8621 asks for in Part I: class of shares, number of shares held at year end, and year-end value category support. The form's value bands include $50,001-100,000, $100,001-150,000, $150,001-200,000, and more than $200,000.

If exceptions are unclear, pause and verify#

Incomplete PFIC information does not remove your responsibility to determine filing requirements and possible elections. If thresholds or exceptions are unclear in your case, stop and verify against the current IRS instructions before filing. If you cannot clearly document why an exception applies, treat filing as required until you can.

For another reporting comparison, see A Deep Dive into Form 3520 (Annual Return To Report Transactions With Foreign Trusts).

Map your ownership chain before touching the form#

Map the ownership chain first. Form 8621 can apply to both direct and indirect PFIC shareholders, and filing is determined PFIC by PFIC when filing circumstances apply. If you cannot trace a clear path from you to each PFIC, pause before preparing the form.

Build a PFIC-by-PFIC ownership map#

For each potential PFIC, document one complete path from you to the asset:

- direct personal account

- indirect ownership through a pass-through entity

- indirect ownership through a foreign corporation in the chain

For each row in your map, capture:

- the immediate owner of the asset

- the entity type, such as Partnership, LLC taxed as a partnership, S corporation, or foreign holding company

- whether your path is direct or indirect

- the document trail supporting that path, such as account statements, entity records, or any K-1 materials you have

The checkpoint is simple: each PFIC should tie to one clear ownership path and a document trail back to you.

Tag PFIC references to the issuing entity. Review your records for PFIC-related references, including Schedule K-1 attachments or footnotes when they are provided. When a PFIC item appears, tag it to the entity that issued that record before you move forward. Keep entity records separate so items do not get mixed across entities. If you cannot match a PFIC reference to one entity and one ownership path, stay in fact-finding mode.

Flag foreign-corporation legs in the chain. If your path runs through a foreign corporation, document that leg clearly instead of leaving it as a generic indirect note. The instructions include indirect-shareholder treatment for a 50%-or-more shareholder of a foreign corporation that is not a PFIC. They also require filing for each PFIC in a PFIC chain.

Before you draft anything, make sure you can trace each PFIC to a clean endpoint and determine form count on a PFIC-by-PFIC basis. If that chain is still unclear, escalate early.

Build the evidence pack before preparation starts#

Build one evidence pack per PFIC before you start on Form 8621. That keeps Part I entries and any Part II election positions tied to records you can actually produce later.

Create one packet per PFIC#

Keep each PFIC in its own file, even if multiple holdings sit in one account. The goal is straightforward: enough support for Part I annual information and any election history you plan to rely on.

| Evidence item | What it supports | Check before moving on |

|---|---|---|

| Year-end account statement | Year-end shares, year-end value support, share class description | Statement date matches tax year-end; holding name matches your ownership map |

| Acquisition record or trade confirmation | Acquisition date and lot details | Date and quantity reconcile to the position held or later sold |

| Disposition record (if sold) | Disposition gain event support and timeline | Sale date and quantity reconcile to prior holdings |

| PFIC Annual Information Statement (if available) | Potential QEF-related reporting support | Entity name and tax year match the PFIC and filing year |

| Prior-year Form 8621 copies | Part II election history | Election ties to the same PFIC, not just the same broker or fund family |

These are working records, not a universal IRS-required checklist for every case. If something is missing, tag the gap now instead of guessing during preparation.

Pull the Part I fields up front. Part I asks for the description of each class of shares held and includes annual fields such as acquisition date, year-end shares, and year-end value. Build those fields into the packet first, with a source note for each field.

If you report value, keep the exact support you used. The form includes value listing when the amount is more than $200,000, so this is not a cosmetic field. Also check ownership status before drafting. Part I includes a checkbox for shares jointly owned with spouse. If records conflict on joint versus sole ownership, resolve that first.

Prove election history before you rely on it#

If you are reporting information with respect to a QEF or section 1296 mark-to-market election, or making a Part II election, prior filings are part of your current-year evidence. Pull the prior Form 8621 records that show the election history before you draft around it.

For QEF treatment, the form directs completion of Part III lines 6a through 7c. If prior records mention an election to extend time for payment of QEF tax, keep that history visible too. The form notes limits tied to some section 951 inclusions and refers to termination events for that election.

Use a no-doc, no-claim rule. If an acquisition date is uncertain, mark it uncertain. If year-end shares or value cannot be tied to support, flag it. If election history cannot be produced, do not treat it as settled.

The point is not to force one regime by default. The point is to label unresolved items early and escalate before filing when gaps affect election treatment, annual reporting, or gain reporting.

Before you lock your PFIC packet, review any separate reporting obligations in your broader workflow, including the FBAR calculator if relevant.

Complete Part I with fewer rework loops#

Treat Part I as a record-mapping step, not a memory test. If each line cannot be traced to your PFIC packet, stop and fix the packet before filing.

Map records directly into Part I fields#

Use your packet to fill Part I exactly as requested for all PFIC shares held by the shareholder: class-of-shares description, joint-ownership checkbox if applicable, acquisition date if applicable, year-end share count, and year-end share value.

| Part I item | What to pull from records | Verification note |

|---|---|---|

| Class-of-shares description | Description for all PFIC shares held by the shareholder | Use the clearest supportable entry if records use different labels |

| Joint-ownership checkbox | Checkbox if applicable | Confirm it matches your records for that filing |

| Acquisition date | Acquisition date if applicable | Reconcile to trade records, including multiple lots or partial sales |

| Year-end share count | Year-end share count | Reconcile to the year-end statement for that PFIC and share class |

| Year-end share value | Year-end share value or exact listed value if more than $200,000 | Tie to the retained year-end record or calculation |

Do not smooth over record conflicts. If statements and trade records use different labels or timelines, use the clearest supportable entry and keep a note with it.

For value, keep the support you used for the Part I bands ($50,001-100,000, $100,001-150,000, $150,001-200,000). If the amount is more than $200,000, keep the exact listed value support.

Match the regime label to documented status. Put amounts under the correct Part I label only when your records support it: Section 1291, Section 1293 (Qualified Electing Fund), or Section 1296 (Mark to Market).

If prior files mention a QEF tax-deferral election, do a direct check before relying on it. The form states you cannot make that election when any portion of line 6a or line 7a of Part III is includible under section 951, and related rules describe termination events.

Run one verification pass before submission. Verify in this order:

- Share counts reconcile to the year-end statement for that PFIC and share class.

- Acquisition chronology reconciles to trade records, including multiple lots or partial sales.

- Value support ties to the retained year-end record or calculation.

Then confirm the Part I joint-ownership checkbox matches your records for that filing.

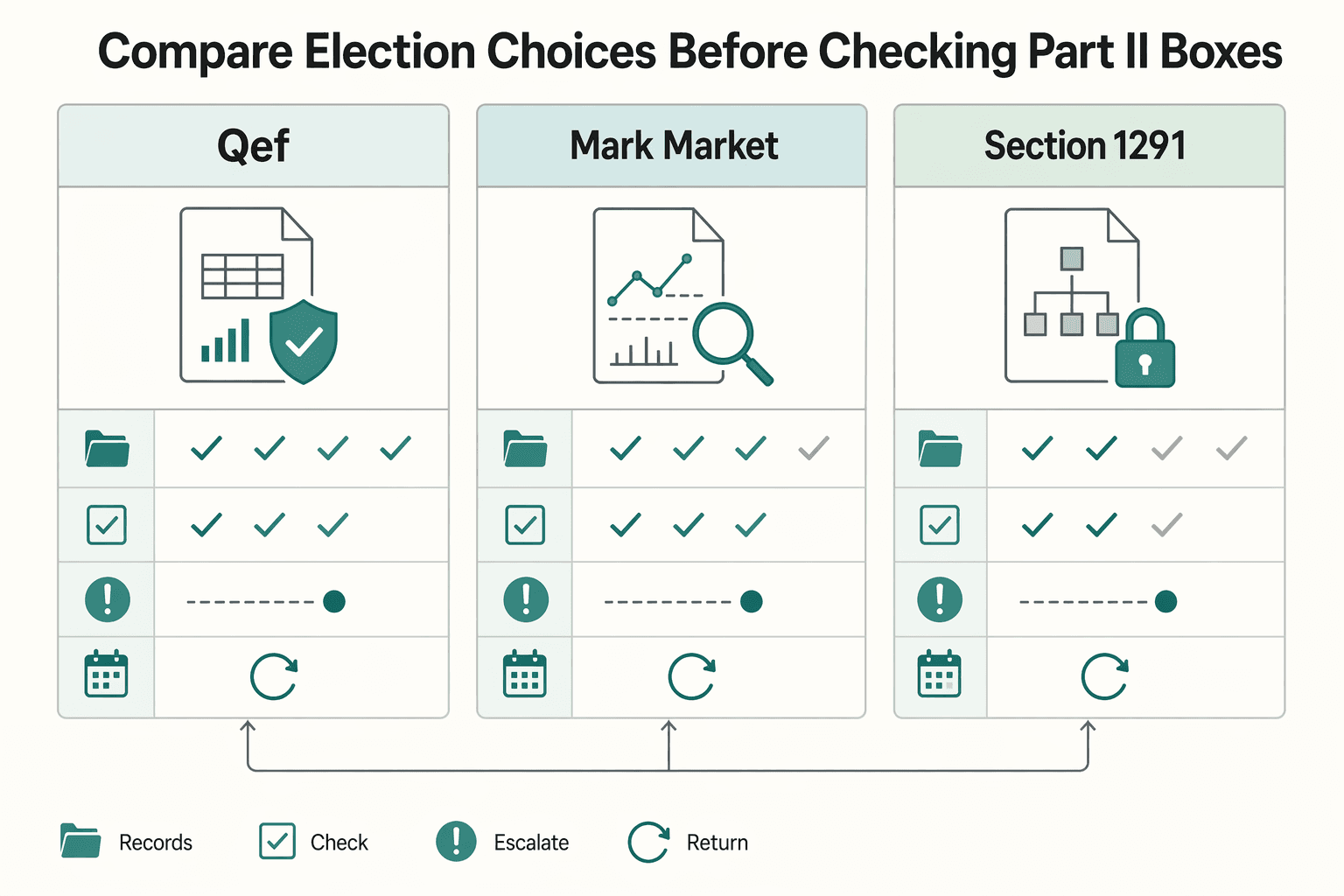

Compare election choices before checking Part II boxes#

Before you check Part II boxes, choose the path you can support with records every year. If QEF inputs are not reliable, do not force a QEF position.

The IRS instructions treat Qualified Electing Fund (QEF) Election, Section 1291 Fund, and Mark-to-Market Election as separate topics. They also include tax-consequence sections for QEF and mark-to-market, plus coordination guidance between mark-to-market and section 1291. This is a real reporting decision, not cosmetic labeling.

| Path | First checkpoint | Ongoing record burden | Practical posture |

|---|---|---|---|

| QEF | Do you have a reliable Annual Information Statement for your holding? | High: retain annual information support year after year | Election path with recurring annual support requirements |

| Mark-to-market election | Does the holding meet the Marketable stock checkpoint in the IRS instructions? | Moderate to high: retain consistent value support each year | Election path tied to recurring value support |

| Section 1291 regime | Are you intentionally choosing the no-election path? | Different burden profile, but still a defined regime | Explicit no-election posture |

QEF is hardest to defend when annual information is not dependable. The practitioner comparison flags this directly as "The Critical Limitation: Annual Information Statement." If that statement is not dependable for your file, use a different path you can defend.

Treat mark-to-market qualification as a gate. For mark-to-market, "Marketable stock" is a specific checkpoint in the IRS instructions. Do not assume qualification. Keep your qualification basis and year-end value support together, and use a consistent method across years.

Section 1291 is still a decision. No election is not neutral drift. Section 1291 Fund is a separate regime, and the practitioner comparison also treats no-election as its own branch. If this is your path, document why it is the most supportable option with your current records.

Escalate transition elections early. If you are considering Deemed Sale Election or Deemed Dividend Election, escalate before filing. This section does not establish their detailed prerequisites or consequences.

Pick the option your documentation can sustain year after year: dependable annual inputs, reproducible numbers, and consistent treatment. For a step-by-step walkthrough, see What is a Qualified Electing Fund (QEF) for PFICs?.

Handle K-1 and indirect PFIC cases without guesswork#

Treat any Schedule K-1 PFIC mention as a verification trigger, not a filing conclusion. The IRS materials state that indirect ownership through a pass-through entity can make you an indirect PFIC shareholder. They also state that a separate Form 8621 is filed for each PFIC held directly or indirectly.

Before elections or box-checking, run one reconciliation. List each PFIC shown in your ownership chain and match it to an expected Form 8621. If the counts do not match, stop and resolve that gap first.

Use a rebuttable-assumption workflow. A K-1 note is enough to investigate, but not enough to finalize your filing position. Map the ownership path, confirm whether a filing trigger applies, and assign each key data point to one source so the same PFIC is not omitted or duplicated.

- Source entity: where the PFIC note came from

- Ownership path: how you connect as a direct or indirect shareholder

- PFIC list: whether each PFIC is new, recurring, or a duplicate reference

- Current-year trigger activity: whether there were direct or indirect distributions, dispositions, or another trigger

- Prior-year filings: whether earlier Form 8621 filings exist and should be reviewed for consistency

Escalate incomplete K-1 data before elections. If K-1 support is incomplete, request clarification first, then involve a tax professional before making election decisions. Document what you requested, what you received, and what remains uncertain so your filing judgment is defensible when pass-through data is still incomplete.

Coordinate Form 8621 with other expat reporting#

Run these as separate checks: Form 8621, Form 8938, and FBAR may overlap on the same assets, and each has its own filing test.

| Filing | What to test | Article note |

|---|---|---|

| Form 8621 | Direct or indirect PFIC shareholding | A separate Form 8621 is filed for each PFIC |

| Form 8938 | Specified foreign financial assets when the filing threshold is met | Attached to the annual return by that return's due date, including extensions |

| FBAR (FinCEN Form 114) | Whether FBAR review is required | Filing Form 8938 does not remove a separate FBAR duty when FBAR is otherwise required |

Form 8621 is tied to direct or indirect PFIC shareholding, and a separate Form 8621 is filed for each PFIC. Form 8938 is for specified foreign financial assets when the filing threshold is met, and it is attached to your annual return by that return's due date, including extensions. If one foreign holding appears in both analyses, run both analyses.

Use one cross-form tracker for each holding so nothing gets dropped. For each foreign account, fund, or entity interest, record:

- the exact asset name and account or custodian

- whether a separate Form 8621 is expected for any PFIC in the ownership chain

- whether Form 8938 review is required

- whether FBAR review with FinCEN is required

- which statement or K-1 supports each conclusion

Keep the FBAR check independent. Filing Form 8938 does not remove a separate FinCEN Form 114 duty when FBAR is otherwise required, so treat FBAR as a fresh yes-or-no decision for each relevant holding.

For related international filing context, see A Deep Dive into Form 5472 for Foreign-Owned US LLCs.

The filing mistakes that create the most expensive cleanup#

Costly cleanup usually starts with one of three preventable errors: missing a PFIC holding, making a Part II election without support, or treating indirect ownership as optional to verify.

Reconcile every suspected PFIC before you finalize#

A common failure point is omission rather than math. Keep one line for every suspected PFIC, even if your final result is no filing for that item.

For each line, record:

- holding name and whether ownership appears direct or indirect

- the record that surfaced it, such as account or entity records

- which IRS trigger you are testing: distribution, disposition gain, QEF or section 1296 reporting, a Part II election, or section 1298(f) annual report requirement

- filing decision status and why

Before sign-off, tie each finalized holding to Part I checkpoints: class description, acquisition date if applicable, year-end shares, and year-end value. If you cannot support the Part I value bracket you choose, the reconciliation is not complete.

Do not choose Part II elections first and hunt for support later. Choose Part II elections only after you confirm documentation and year-to-year consistency. Part II includes the QEF election and the section 1296 mark-to-market election, and the form notes that some QEF tax-deferral elections may be unavailable or can terminate under listed events.

Use this consistency check before filing:

- prior-year Form 8621 treatment

- current-year records supporting the same treatment or a documented reason for change

- election support documents kept with the filing packet

Indirect ownership is not a side note. IRS Form 8621 guidance covers direct or indirect shareholders, and the instructions include sections for indirect shareholders and pass-through entity interest holders. If records indicate PFIC exposure through an entity, trace the chain far enough to make a clear filing decision. Do not leave indirect exposure in a "we will sort it out later" bucket.

When the exception analysis is fuzzy, stop guessing. If you cannot clearly determine whether an IRS trigger applies, treat that as unresolved, not exempt. That includes distributions, disposition gain, QEF or section 1296 reporting, Part II elections, and section 1298(f) annual report situations.

Document what is unknown, what records are still needed, and where the decision is blocked, then get professional guidance before filing.

When to bring in a tax professional#

If your reconciliation still has unresolved judgment calls, escalate before filing. Bring in a specialist when the work shifts from straightforward data capture to decisions about indirect ownership, Part II election eligibility, or prior-year filing history.

Escalate when ownership structure is still unclear#

Multi-entity ownership or PFIC-in-PFIC ownership can be a practical handoff point. Form 8621 rules can apply to direct and indirect shareholders, and a separate Form 8621 is filed for each PFIC, including each PFIC in a chain. If you cannot trace each holding from you to the PFIC and label it direct or indirect, pause and escalate before you finalize Part I or choose reporting treatment.

Escalate when Part II or reporting treatment is uncertain. If you are unsure whether a Part II election is available on your facts, do not guess under deadline. Making a Part II election is itself a listed filing trigger, and the form indicates that some elections are not allowed in certain section 951 inclusion cases. If your records are not clear enough to support your reporting treatment for the current year, escalate before filing.

Bring a tight packet, not a vague problem. Bring the records behind your filing position so a specialist can evaluate the facts. Include:

- an ownership map with each PFIC marked as direct or indirect

- the Form 8621 filings and election details you already have

- any entity statements you are relying on for PFIC reporting

- a short list of unresolved questions

Before the meeting, check current IRS Form 8621 updates so your present-year decisions are based on the latest guidance, not just an older saved PDF.

Final takeaways and your next steps#

Use a strict sequence and do not improvise: confirm filing duty, map ownership, assemble your evidence pack, then decide elections.

-

Confirm filing duty first. Form 8621 applies when a U.S. person is a direct or indirect PFIC shareholder and a listed trigger applies, including certain distributions, recognized gain on disposition, QEF or section 1296 mark-to-market reporting, a Part II election, or a section 1298(f) annual report requirement. If you cannot tie your facts to the current Form 8621 instructions, pause and verify before filing.

-

Map ownership before making election decisions. Trace each PFIC position as direct or indirect and make sure every holding has a clear ownership chain. If any part of that chain is unclear, do not fill gaps with assumptions about exceptions or election eligibility.

-

Build the evidence pack before preparing forms. Keep records that support what you owned, when you owned it, any disposition activity, and year-to-year treatment consistency. For election-related positions, keep prior Form 8621 support. If your records do not support a QEF, section 1296 mark-to-market, or other Part II path, do not force it.

Before filing, run a final checklist:

- PFIC inventory reconciled to expected filings, with no omissions, duplicates, or unexplained positions

- election treatment consistent with prior-year filings and supporting records

- supporting documents retained, not just completed forms

- cross-form alignment checked across Form 8938 and FBAR lists

Keep your Form 8621 trigger analysis separate from your Form 8938/FBAR review. Form 8938 is attached to your annual return and filed by that return's due date, including extensions, and it does not remove a separate FBAR filing obligation when FBAR applies.

If you use compliance tooling, keep exports, logs, calculation outputs, and source files organized by tax year and PFIC position so your process is repeatable. If records are thin or current IRS details are unclear, verify first or escalate with a focused packet: ownership map, trigger notes, prior election history, and unresolved gaps.

If you want this process to be repeatable next year, keep your checklist and supporting workflows in one place with Tools.

Frequently Asked Questions

Who must file Form 8621 for PFIC reporting?

Use the current IRS Instructions for Form 8621, starting with the “Who Must File” section. The instructions explicitly address indirect shareholders and interest holders of pass-through entities. A practical default is to map each PFIC position as direct or indirect before deciding that you do not need to file.

Do I still file Form 8621 if I had no PFIC distributions or sales this year?

You cannot rely on "no sale, no distribution" as a standalone filing rule. Check your filing position against the current “Who Must File” instructions and your own reporting history. If anything is unclear, treat that as a review point before filing.

How many Form 8621 filings do I need if I own multiple PFICs?

Do not estimate from memory when you hold multiple foreign investments. Build a complete PFIC inventory first, then check the current instructions against that list, including any indirect or pass-through holdings. Avoid assuming a fixed filing count until that review is complete.

What documents do I need before preparing Form 8621?

There is no single document checklist confirmed in this grounding pack. Start with organized ownership and prior-year filing records, then verify what support you need under the current instructions for your facts. If your records do not clearly support your position, pause and resolve the gaps first.

What is the difference between QEF, mark-to-market, and the default PFIC regime?

The IRS instructions treat QEF, Section 1291, and mark-to-market as separate reporting frameworks. Beyond that, use the current instructions to determine which path applies to your facts. If your documentation does not cleanly support a path, do not force an election just to simplify this year.

How does Form 8621 relate to FBAR, FATCA, and Form 8938?

Form 8938 and FBAR are separate filings, and they are not substitutes for one another. Form 8938 is attached to your annual return and filed by that return’s due date, including extensions, and filing Form 8938 does not remove a separate FBAR obligation when FBAR otherwise applies. A useful check is to compare your PFIC list with the foreign-asset list you use for Form 8938.

When should a U.S. expat stop self-preparing and hire a specialist?

Consider escalating when your result depends on unresolved ownership chains, unclear indirect holdings, or uncertainty about which reporting framework applies. Also consider escalating when prior-year consistency is uncertain and you cannot document your position with confidence. The handoff is cleaner when you bring a concise decision packet and specific unresolved questions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- federalregister.gov/documents/2019/07/11/2019-12030/guidance-on-...trusted

- irs.gov/forms-pubs/about-form-8621trusted

- irs.gov/instructions/i8621trusted

- reginfo.gov/public/do/DownloadDocumenttrusted

- sec.gov/Archives/edgar/data/2025416/0001193125251950...trusted

- sec.gov/Archives/edgar/data/1939965/0001213900250444...trusted

- greenbacktaxservices.com/knowledge-center/form-8621external

- hcvt.com/alertarticle-PFIC-Reporting-for-Direct-and-I...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

PFIC Rules for US Expats Investing Abroad

Start with compliance, not optimization. Screen PFIC risk before you buy, rebalance, or add cash. A common costly mistake is buying a familiar local fund first and checking PFIC classification later.

A Guide to Index Fund Investing for Freelancers

If you run a business-of-one, you're not here for vibes; you're here for a repeatable system you can run.