Quick Answer

Start by confirming residency status and temporary-resident treatment before you classify any income line. For australia temporary resident tax, the article’s core rule is to file from status first, then test each payment against source evidence and payer records. It highlights concrete checks: foreign residents cannot claim the tax-free threshold, foreign residents can claim Medicare levy exemption, and some withholding cases on Australian-sourced interest, dividends, or royalties change declaration handling. When facts shift mid-year, re-test before lodging.

Start with residency status before classifying any income line — the ATO treats temporary and foreign residents under different rules#

Start with status, not income lines. For australia temporary resident tax, the Australian Taxation Office frames filing around one first decision: what you must declare depends on your residency status and whether you are also a temporary resident. Use this sequence:

- Identify the status you need to test first.

- Sort each income item by source and type.

- Apply the ATO declaration rule for that status before you lodge.

That order matters because a status mistake carries through everything that follows. It affects what goes on the return, when withholding changes reporting, and when HELP, AASL, or VSL debt can still pull worldwide income into the picture.

Keep source classification concrete. In the ATO examples, Australian-sourced income includes employment income, rental income, Australian pensions and annuities, and capital gains on Australian assets. Even in an international year, one Australian-sourced line can change what you need to file or review.

Also, do not collapse foreign resident and temporary resident outcomes into one generic rule. The ATO separates "Foreign resident income" and "Temporary resident income," so treat them as distinct checks when you set your filing position.

Before you finalize the return, verify which ATO section you relied on and whether any Australian interest, dividends, or royalties were already subject to withholding by the payer. For foreign residents, the ATO says those amounts are not declared only when withholding has already been applied by the Australian payer and your foreign-resident details have been provided.

A practical way to avoid last-minute errors is to lock the status decision in your working papers before you populate the return. Then test each income line against that status, rather than changing status assumptions halfway through the draft because one item looks inconvenient or unfamiliar.

Use ATO wording as your primary authority when secondary summaries conflict or skip detail, and keep a record of the page version you relied on. Related reading: A Deep Dive into the US-Canada 'Tie-Breaker' Rules for Tax Residency.

Start with the three-part temporary resident test#

For this issue, the first job is to separate migration status from tax status, then check whether your facts changed during the year. The ATO says it does not use the same rules as Home Affairs, so your visa outcome alone is not enough for filing decisions. Use this check before you classify income:

| Step | Action | Detail |

|---|---|---|

| Migration records | Confirm your migration-status records are current | The ATO does not use the same rules as Home Affairs, so visa outcome alone is not enough |

| Tax residency analysis | Run the ATO tax residency analysis on its own terms | Use the resides test as the primary test and do not treat any single factor as decisive |

| Mid-year review | Re-check your position for any mid-year status change before lodging | If the year includes more than one factual pattern, document each period separately |

- confirm your migration-status records are current

- run the ATO tax residency analysis on its own terms, with the resides test as the primary test and no single factor treated as decisive

- re-check your position for any mid-year status change before lodging

Treat this as a gate, not a rough indicator. ATO guidance also treats temporary resident status as distinct from whether you are an Australian resident or foreign resident for tax purposes, so do not merge those checks.

If your facts are mixed, pause before you assume a particular tax outcome. Keep your visa evidence and residency analysis side by side, weigh your domestic and economic affairs, and use the ATO residency tool as a first pass before filing.

If the year includes more than one factual pattern, document each period separately. For example, do not run one blended analysis for a year that started with one living arrangement and ended with another. The point is not to overcomplicate the return. It is to make sure your filing position follows dated facts rather than a rough year-end impression.

Separate temporary resident, foreign resident, and Australian resident outcomes#

Use filing behavior, not labels, as your anchor. The ATO says what you need to declare depends on both your residency status and whether you are also a temporary resident, so temporary resident and foreign resident are not interchangeable.

Filing comparison#

| Status | Reportable income base in the Australian tax return | Tax-free threshold | Medicare levy | Australian-sourced interest, dividends, royalties when withholding applies |

|---|---|---|---|---|

| Temporary resident | Not established in the provided ATO excerpt. Verify against current temporary resident guidance before lodging. | Not established in the provided ATO excerpt. | Not established in the provided ATO excerpt. | Not established in the provided ATO excerpt. |

| Foreign resident | Declare Australian-sourced income. You generally do not declare income from outside Australia. If you have a HELP, AASL, or VSL debt, you may still need to declare worldwide income. | You cannot claim the tax-free threshold, so tax applies to every dollar earned in Australia. | You can claim an exemption from the Medicare levy. | Generally not declared if the Australian payer already withheld tax. |

| Australian resident | Not established in the provided ATO excerpt. Verify resident return rules separately before filing. | Not established in the provided ATO excerpt. | Not established in the provided ATO excerpt. | Not established in the provided ATO excerpt. |

The support in this excerpt is uneven by design. The foreign resident row is explicit, while the temporary resident and Australian resident rows are not. Do not fill those gaps by assumption.

Do not assume equivalence#

Temporary resident status sits alongside residency analysis. It does not replace it. If you reduce this to "temporary resident = foreign resident," you can misapply threshold, levy, or withholding treatment even when the foreign-income instinct feels plausible.

One useful discipline is to write your filing row in one sentence before you complete the return, then test the return fields against that sentence. If the return settings imply a different row from the one in your notes, treat that mismatch as an error to resolve, not a harmless software quirk. If you cannot point to a current ATO rule that supports your row, stop and verify before you finalize the return.

Verification checkpoint#

Before lodging, confirm your row with this checklist:

| Checkpoint | What to confirm | Detail |

|---|---|---|

| Residency outcome | Reconfirm your residency outcome for the relevant period | Especially if facts changed during the year |

| Temporary resident status | Reconfirm whether you are also treated as a temporary resident under current ATO guidance | Temporary resident status is distinct from residency analysis |

| Interest, dividends, royalties | Verify whether the payer already withheld tax | This check applies to Australian-sourced interest, dividends, or royalties |

| Payer details | If using foreign resident withholding treatment, confirm you told the payer you are a foreign resident and gave a home address outside Australia | Foreign-resident withholding treatment depends on those payer details being provided |

| HELP, AASL, or VSL debt | Check whether you have a HELP, AASL, or VSL debt | Worldwide income may still need to be declared |

- Reconfirm your residency outcome for the relevant period, especially if facts changed during the year.

- Reconfirm whether you are also treated as a temporary resident under current ATO guidance.

- For Australian-sourced interest, dividends, or royalties, verify whether the payer already withheld tax.

- If using foreign resident withholding treatment, confirm you told the payer you are a foreign resident and gave a home address outside Australia.

- Check whether you have a HELP, AASL, or VSL debt, since worldwide income may still need to be declared.

The common failure mode here is omission by assumption. If payer withholding is missing or your residency details with the payer are stale, treat that as a review point before filing.

Related: A Guide to Tax Residency in Australia for Digital Nomads.

Classify every income stream before you file#

Classify each line item by source before you start the return, and treat any unclear source as review-required. Do not guess from bank location or invoice currency alone.

A simple working sheet usually makes the next steps cleaner. Start with two buckets, Australian-sourced income and foreign-source income. Then add two columns, what the ATO excerpt supports and evidence to keep.

In the provided ATO excerpt, for foreign residents working in Australia, the rules are clear on a few core points. You declare Australian-sourced income. You generally do not declare income from outside Australia. HELP, AASL, or VSL debt may still require worldwide income reporting. Specific temporary resident treatment line by line is not established in this excerpt, so keep that as a verification item rather than filling the gap by assumption.

A good operational habit is to break income out by payer and by period, not just by category. That matters when one payer has withholding evidence and another does not, or one item is supported by clear statements while another still needs review. If you lump everything together too early, you make later verification harder than it needs to be.

| Income line | First bucket to test | What the provided ATO excerpt supports | Evidence / checkpoint |

|---|---|---|---|

| Client service income from freelance work | Review-required if source is unclear | No source-classification rule for freelancer service income is established in the excerpt | Contracts, invoices, work-delivery timeline, work or travel location records, client correspondence |

| Rental income | Australian-sourced income | Rental income is listed as Australian-sourced income | Lease, property manager statements, annual rental summary |

| Australian pensions and annuities | Australian-sourced income | Listed as Australian-sourced income unless exempt under Australian tax law or a tax treaty | Annual statement, payer details, exemption or treaty review note |

| Interest, dividends, royalties | Australian-sourced income with conditional declaration treatment | Not declared only if the Australian payer has already withheld tax | Statements, withholding evidence, payer details on file, confirmation you advised the payer of foreign-resident status and a home address outside Australia |

| Capital gains on Australian assets | Australian-sourced income | Capital gains on Australian assets are listed as Australian-sourced income | Sale contract, asset records, acquisition records, gain calculation working papers |

Put a hard flag on loan obligations#

If you have a HELP, AASL, or VSL debt, put a prominent flag on your sheet before filing. The excerpt says you may need to declare worldwide income in that case, so collect foreign-income records you might otherwise leave out.

Make that flag visible early, not at final review. Once a worldwide-income question appears late in the process, the usual problem is not the rule itself. It is the scramble to locate statements and timelines that were left out because the first draft assumed only Australian income mattered.

Practical filing rule#

If a line is clearly covered in the excerpt, classify it and attach support. If it is not clearly covered, especially service income where source is fact-sensitive, keep it as review-required and resolve it before lodging.

Do not force uncertain items into a final bucket just to make the worksheet look complete. A marked unresolved line is safer than an unsupported classification that quietly flows into the return.

Handle capital gains and property exposure without guesswork#

Property gains deserve their own lane early. The ATO excerpt is clear that a foreign resident must declare capital gains on taxable Australian property, so do not fold property into broad assumptions about temporary resident treatment. Start with a clean split before you classify anything else:

| Asset or scenario | What the ATO excerpt supports | What to do now |

|---|---|---|

| Taxable Australian property | A foreign resident must declare capital gains on taxable Australian property | Treat as high-stakes and escalate early |

| Australian home sale | The gain may need to be included if you are a foreign resident when you sign the contract of sale | Check status at contract signing first |

| Other assets | No specific temporary resident capital gains exemption is established in this excerpt | Keep as review-required; do not assume exemption |

Use the contract-signing date as your checkpoint for property transactions. The excerpt points to status "at the time you sign the contract of sale," so test that date directly when you assess the gain.

Build a simple file before lodging: signed contract of sale, execution date, and residency-status evidence tied to that date. If your status changed during ownership, for example from temporary resident to Australian resident or from temporary resident to foreign resident, flag it for adviser review. The excerpt confirms that residency and temporary status affect obligations, but it does not provide outcome rules for mid-ownership status changes.

Where property is involved, keep the transaction documents together rather than spread across general tax folders. In practice, the cleanest file is one folder with the sale contract, timing records, ownership records, and your status note for the signing date. That makes it easier to test the point that actually matters in the excerpt and avoids re-creating the timeline later.

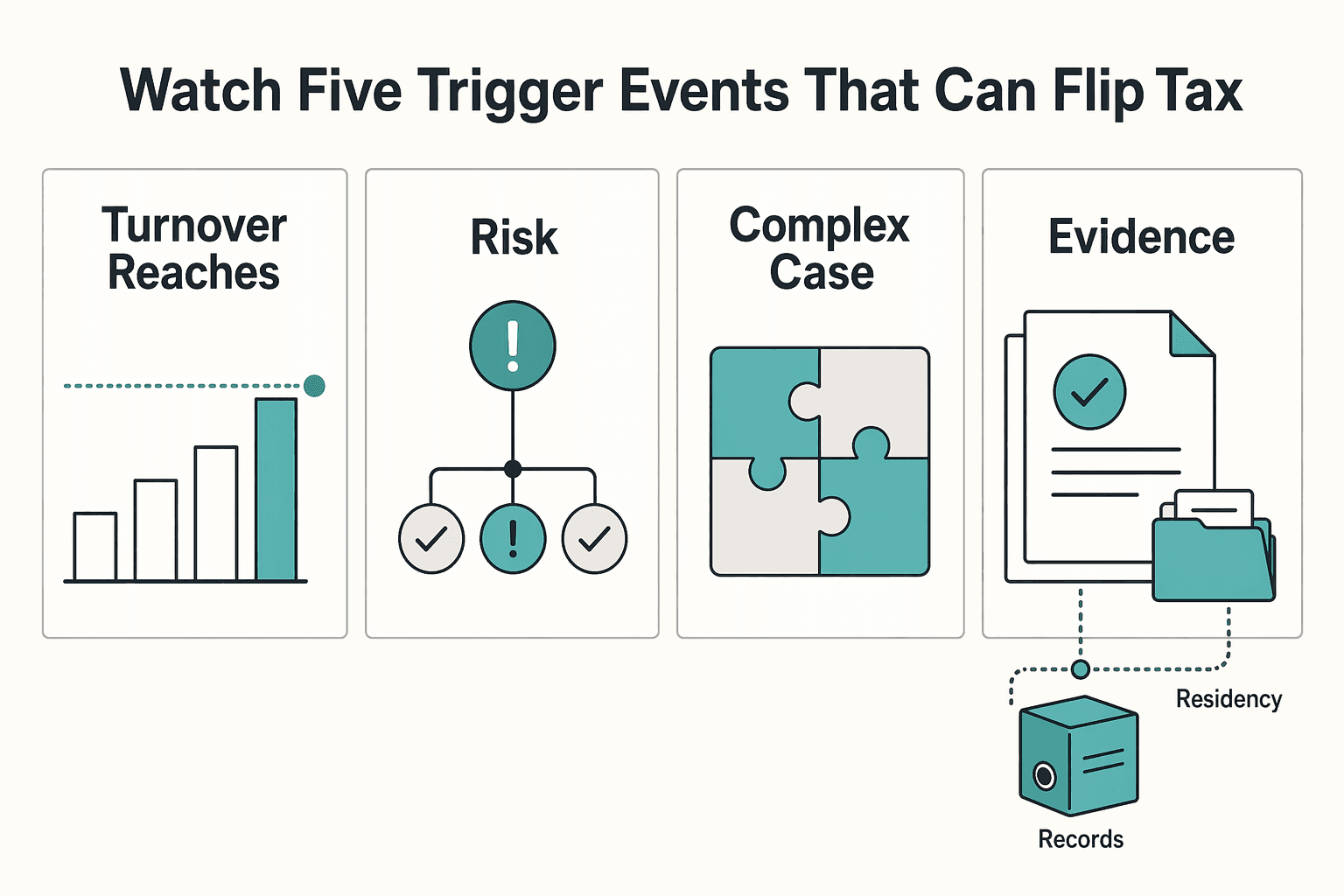

Watch the five trigger events that can flip your tax position#

These five items are compliance triggers, not automatic income-tax outcomes. The excerpts for this section support GST and registration process requirements for non-resident businesses, not temporary-resident income-tax treatment. The safer move is to pause, verify dates, and re-check your position before you reuse last year's assumptions.

| Trigger event to track | What to verify right away | Dated evidence to keep |

|---|---|---|

| Turnover reaches the GST threshold | Whether you now need to register based on the A$75,000 threshold (or A$150,000 for non-profit organisations) | Turnover reports, dated threshold calculation, internal review note |

| GST registration becomes required | Whether registration is completed within 21 days to reduce penalty risk | Registration submission receipt, internal deadline log, follow-up notes |

| Standard GST registration as a non-resident | Whether additional proof-of-identity requirements apply and may extend processing time | Identity documents submitted, ATO correspondence, processing timeline notes |

| Lodgment from outside Australia | Whether you need an Australian registered tax agent because electronic lodgment from outside Australia is unavailable | Tax agent engagement record (if used), lodgment method notes, submission receipts |

| ATO registration confirmation arrives | Whether the written notice and effective date match your internal records and reporting start date | ATO written GST registration notice, effective-date log, system update record |

Use a monthly checkpoint rule#

A monthly checkpoint is a practical house rule. Recheck whether GST registration is required, whether your turnover tracking is current, and whether any registration step is blocked before you lodge or report.

This does not need to be a long memo every month. A dated confirmation note is usually enough when nothing changed. The value is in catching the month where something did change and linking that event to your compliance actions while the facts are still fresh. If you operate as an individual carrying on an enterprise, confirm your ABN details are still accurate.

Know the difference between a quiet year and a changed year#

A quiet year is usually a confirmation exercise. A year where turnover crosses the threshold, registration becomes required, or non-resident processing steps change should be treated as a fresh compliance check, not a carry-forward assumption.

Make the file defensible#

Keep one dated note for each checkpoint: what changed, the effective date, what document supports it, and what action you took. If you conclude nothing changed, record that explicitly so the timeline is clear if reviewed.

Use treaty tie-breaker logic when two countries claim you#

If Australia and another country both treat you as resident, domestic rules alone may not be enough for a filing position. Your outcome may depend on the relevant double tax agreement, and generic summaries are not a safe substitute for checking the actual treaty text.

The ATO view in TR 2001/13 is that treaty interpretation is, in some respects, different from domestic tax law interpretation. You can look aligned under an Australia-only reading and still miss a treaty rule that affects how taxing rights are allocated between the two countries.

What to do before drawing a treaty conclusion#

Collect facts first, then verify the specific bilateral treaty language against those facts. At minimum, line up:

- Each country's residency position

- The dates each country treats you as resident

- The income in scope, including foreign-source income

Keep dated records that support that analysis.

Use the authorised consolidated PDF of TR 2001/13, and check its current status on the ATO Legal database before you rely on it.

A practical order helps here. First write down what each country is saying about your residency. Then match those positions to dates. Only after that should you test the treaty language. If you jump straight to a treaty summary without the dated fact pattern in front of you, it is easy to apply the wrong conclusion to the wrong period.

Where people get this wrong#

The common failure mode is copying a treaty answer from a generic summary and applying it unchanged. TR 2001/13 is clear that each DTA is separately negotiated, so treaty terms differ across countries.

If your facts include dual residency and cross-border income, consider getting treaty-specific advice before filing. For a step-by-step walkthrough, see A deep dive into the US-Australia 'tie-breaker' rules for a dual-resident software developer.

Build your evidence pack for an ATO-defensible position#

Your file should let a reviewer trace the path from records to return without relying on memory. For temporary resident income tax specifically, the material here does not provide a prescribed ATO evidence checklist, so treat the structure below as a practical way to organize the year, not a legal requirement list.

Keep a practical core file#

| File element | What to keep | Detail |

|---|---|---|

| Timeline | A dated timeline of key changes that affected your filing position | Keep dates tied to filing-position changes |

| Income map | A working income map by payer, period, amount, and provisional treatment | Map income by payer and period before final treatment |

| Working papers | Return working papers, including drafts, calculations, and judgment notes | Keep the materials used to prepare the return |

| Operational records | Supporting operational records such as invoice trails, payout records, and reconciliation exports | Use them where useful for timing and treatment |

- a dated timeline of key changes that affected your filing position

- a working income map by payer, period, amount, and provisional treatment

- return working papers, including drafts, calculations, and judgment notes

- supporting operational records, where useful for timing and treatment (for example, invoice trails, payout records, and reconciliation exports)

Keep a decision log for material items#

Use a simple log for each material line item: item, period, amount, treatment, evidence file, assumption, unresolved point, and final return outcome. If a point is uncertain, mark it clearly instead of forcing a definitive label.

This log does two jobs. It helps you prepare the return, and it preserves the reasoning behind the return after filing. That matters most when an item moved from uncertain to resolved during the process and you want a clear record of what changed and why.

Add a GST/ABN evidence layer when relevant#

Where your facts create Australian GST exposure, keep the records that support registration and ongoing lodgment:

| Artifact | Why it matters | Concrete checkpoint |

|---|---|---|

| ABN registration records and identity documents | ABN is required before GST registration; non-resident identity checks can increase processing time | Keep what was filed and when |

| ATO written GST registration notice | Confirms registration details and effective date | File the notice with the effective date |

| BAS lodgments and payment confirmations (plus any internal reconciliations you rely on) | Supports recurring GST reporting | Standard non-resident GST registration includes BAS and GST obligations, monthly or quarterly |

Also keep the threshold and timing logic used in your file where relevant: A$75,000 turnover, A$150,000 for non-profits, the 21-day registration window once required, and GST at 10% or 1/11th. If you are offshore, note the lodgment constraint separately. You cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

If you want this file to stay usable, keep a simple index at the front. List the timeline, the income map, the decision log, and the GST layer if applicable. The goal is not formality for its own sake. It is to let you or an adviser find the exact support for a treatment call without searching through unrelated records.

File with fewer surprises on threshold levy and withholding rules#

Before lodging, confirm that threshold, Medicare levy, and withholding treatment match the status you are actually filing under, not any carried-forward defaults.

Confirm the threshold and levy position from status, not habit#

Start with status, then set the return fields. For foreign residents, ATO wording says you cannot claim the tax-free threshold, so tax applies from every dollar of Australian income, and you do not pay the Medicare levy in the Australian return.

Do not assume a temporary resident outcome is automatically the same as a foreign resident outcome here; verify it separately. Treat that as a verification step, and keep a short file note on which status you applied and why.

Before lodging, reconcile these items:

- your residency conclusion in working papers

- threshold and Medicare levy settings in the return

- any prefill settings that may have rolled over from a prior year

If those do not match, stop and resolve the gap before filing.

A useful final check is to compare the summary screens in the return against your status note, not just the data-entry screens. Sometimes the mismatch only becomes obvious when you look at the completed calculation and see threshold or levy treatment that does not fit the filing row you intended to use.

Check withholding on interest, dividends, and royalties#

For Australian-sourced interest, dividends, and royalties, declaration treatment depends on whether tax was already withheld by the Australian payer.

Keep evidence that supports the withholding treatment, including proof that you told the payer you are a foreign resident and gave an overseas home address. If withholding is missing, inconsistent, or not traceable in payer records, mark the item unresolved and review it before lodging.

When you review these items, test the payer record and the statement together. If the statement shows withholding but your records do not show the status details given to the payer, keep both points in the file. If the statement does not show withholding when you expected it to, do not assume the omission is harmless.

Add one hard stop to your pre-lodgment checklist#

Use this final gate: Any unresolved status or source-classification issue that changes threshold, levy, or withholding treatment? If yes, do not lodge until it is resolved or escalated.

This matters most when your status label changes threshold or Medicare settings, or when withholding treatment on interest, dividends, or royalties is unclear.

Default to current ATO wording when summaries conflict#

If secondary summaries conflict, use current ATO wording and save what you relied on in your tax-year file. For this guidance set, keep a screenshot or PDF showing the ATO page date (last updated 16 June 2025).

Know when to escalate to a tax adviser immediately#

Escalate as soon as the issue moves beyond return drafting and into GST registration deadlines, BAS lodgment constraints, or an ATO information request.

Escalate now if GST registration may be required#

For non-resident businesses with sales connected with Australia, GST obligations are a key trigger. If turnover is at or above A$75,000 or A$150,000 for non-profit organisations, and registration is required, the ATO says you must register within 21 days. Penalties may apply if you fail to register when required.

If you cannot confidently confirm turnover, Australia-connected sales, or ABN status, escalate before the deadline. You need an ABN before GST registration.

Escalate if you cannot see a clean BAS lodgment path#

Under standard GST registration, non-resident businesses need to lodge BAS and pay GST monthly or quarterly. The ATO also states you cannot lodge electronically from outside Australia and may need an Australian registered tax agent.

If you are offshore, facing ABN identity-proofing delays, or cannot map registration through to ongoing BAS lodgment, escalate early rather than troubleshooting late.

Escalate early in any ATO information-gathering dispute#

If the ATO is requesting information, escalate quickly and organize your evidence pack. The ATO notes many disputes begin with misunderstandings and emphasizes relevant information and evidence.

Prepare one consistent file:

- turnover worksheet and ledger for Australia-connected sales

- ABN and GST registration records

- BAS lodgment and payment records

- ATO correspondence and submitted identity documents

If an adviser needs to step in, handing over one organized file can reduce avoidable follow-up questions. The facts may stay the same, but the response is usually stronger when the timeline, records, and unresolved points are laid out clearly.

For broader cross-border context, see A Deep Dive into the US-Australia Tax Treaty's 'Independent Personal Services' Article.

Conclusion#

The lowest-stress path is straightforward: verify your tax residency status first, then classify income, document your decisions, and escalate early when the facts are unclear.

For australia temporary resident tax, do not treat a visa label as your tax answer. The ATO uses its own residency tests, and it states those rules are different from Department of Home Affairs rules. It also states that having a visa does not automatically make you an Australian resident for tax purposes, and that temporary resident status can coexist with either Australian resident or foreign resident outcomes.

Treat residency as a recurring checkpoint, not a one-time setup. The ATO confirms residency status can change during the year, so re-check your position when your facts change before you file.

Keep an evidence trail as you go: the residency test outcome you relied on, the date you checked guidance, and the records behind your treatment decisions. Keep the page date from the version you relied on with your file.

Next steps:

- Re-run your current year through the ATO residency tests.

- Classify income only after that status call is recorded.

- Get expert review before filing for any edge case or unsupported assumption.

If your facts are complex or change during the year, use this checklist and then talk with Gruv to confirm your next operational step.

Frequently Asked Questions

Who qualifies as a temporary resident for Australian tax purposes?

The ATO excerpt used here confirms that residency and temporary status affect your tax and other obligations, but it does not provide the full qualification test. Verify your position using your documented residency facts and visa records.

Do temporary residents pay Australian tax on foreign-source income?

Do not assume foreign income is automatically exempt or automatically taxable. The confirmed point here is narrower: foreign residents must declare income earned in Australia.

What income must a temporary resident include in an Australian tax return?

From the provided excerpt, the confirmed rule is that foreign residents must declare income earned in Australia. It also says Australian-sourced interest, dividends, and royalties generally do not need to be declared if the payer already withheld tax. Before lodging, match each payment to payer statements and confirm withholding was actually deducted.

Do temporary residents get the tax-free threshold?

Foreign residents have no tax-free threshold. If your return depends on claiming one, verify your status first.

Do temporary residents pay the Medicare levy?

This excerpt does not establish a temporary resident Medicare levy rule. It does confirm that foreign residents do not pay the Medicare levy and claim exemption for the number of days in the income year they are foreign residents. Keep a dated residency timeline and travel records if your status changed during the year.

Are capital gains taxed differently for temporary residents, especially for taxable Australian property?

A confirmed risk point is that capital gains on an Australian home may still need to be included if you are a foreign resident when you sign the sale contract. Keep the contract-signing date, settlement papers, and your residency position at signing together in one file.

Can tax treaties and tie-breaker rules override normal Australian tax residency outcomes?

Possibly, but this excerpt does not establish treaty tie-breaker mechanics or outcomes. If two countries both treat you as a resident, do not self-apply treaty summaries without review. Treat that as an adviser case, especially when material foreign income or a property sale is involved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- abr.gov.au/business-super-funds-charities/applying-abn/...trusted

- ato.gov.au/individuals-and-families/income-deductions-o...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- ssa.gov/international/CoC_link.htmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints

The goal is a defensible, low-drama position the Australian Taxation Office (ATO) can follow from your records, not a clever workaround. For a digital nomad, that usually means keeping two tracks straight: residency and GST/ABN admin. Consistency is what holds up over time: use real facts, take steps in a clear order, and keep documents that still match months later.

The Best Tools for Creating Professional Presentations

Use a 2025-2026 validation sweep each quarter: confirm one monthly software baseline ($15/month), one collaboration baseline ($30/month), and one premium workflow baseline ($60/month) before changing client-facing tool commitments.